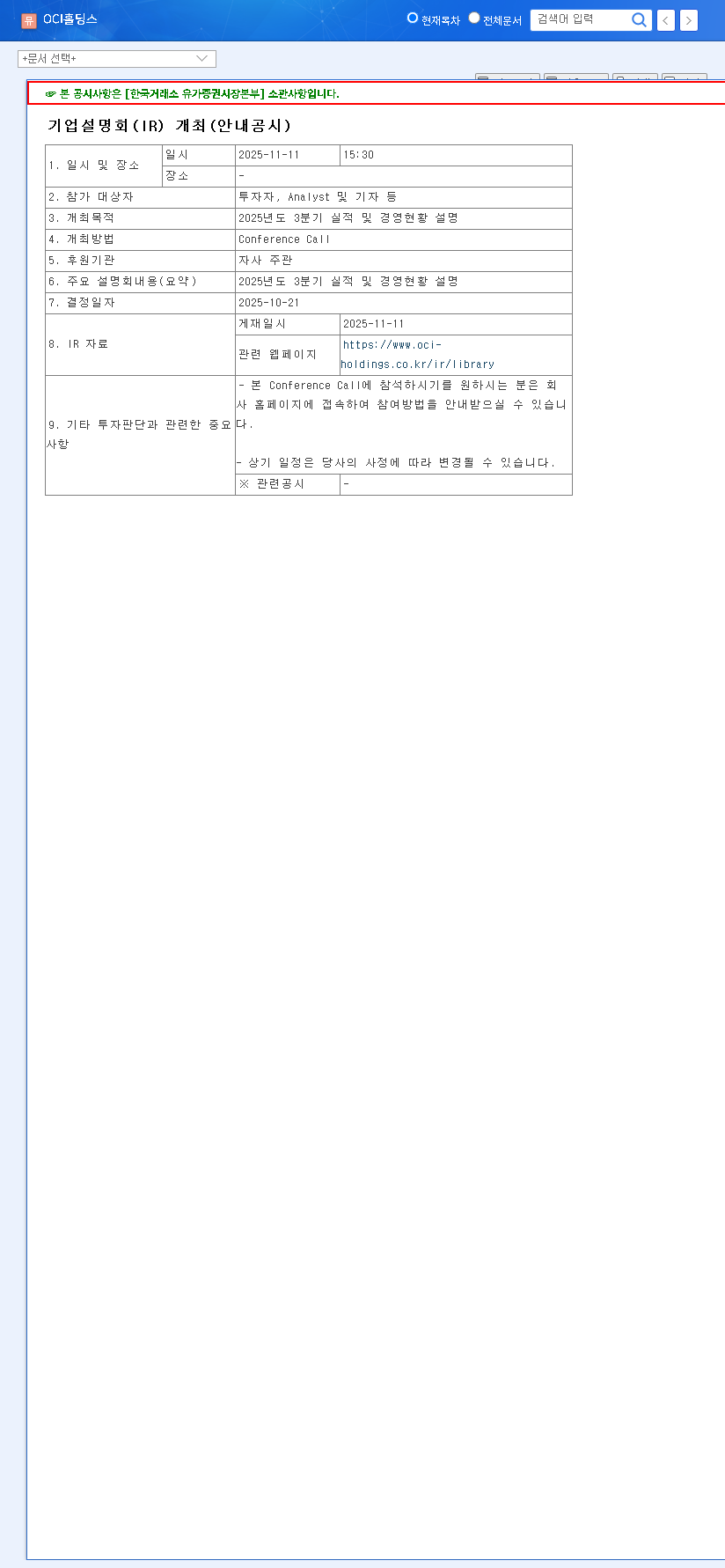

Attention investors: The upcoming OCI Holdings Q3 2025 Earnings announcement is a pivotal event that demands close scrutiny. On November 11, 2025, at 3:30 PM KST, OCI Holdings Company Ltd. will host its investor relations (IR) conference to present its third-quarter performance and management outlook. This is more than a routine update; it’s a critical opportunity for investors to assess the company’s financial health, strategic direction, and future growth potential in the competitive global market.

This comprehensive analysis will break down what to expect from the OCI Holdings IR, explore key financial metrics to watch, outline potential market scenarios, and provide an actionable plan to help you make informed investment decisions. The official announcement was registered on October 21, 2025. You can view the Official Disclosure (Source: DART) for more details.

Why the OCI Holdings IR is a Must-Watch Event

An investor relations conference is a direct line of communication between a company’s leadership and its shareholders. For a major player like OCI Holdings (Market Cap: KRW 1.8702 trillion), this event is crucial for several reasons. It resolves information asymmetry by providing transparent, firsthand data on the company’s performance, cutting through market noise and speculation. Furthermore, the discussion on management status offers invaluable insights into long-term strategy, upcoming projects, and responses to industry challenges.

Key Financial Metrics to Scrutinize

During the OCI Holdings Q3 2025 Earnings call, savvy investors should look beyond the headline figures. Pay close attention to these critical metrics:

- •Revenue Growth: Is the company’s top-line growing, and how does it compare to the previous quarter and the same quarter last year? This indicates market demand and pricing power.

- •Operating & Net Profit Margins: Are margins expanding or contracting? This reveals the company’s operational efficiency and ability to control costs.

- •Forward-Looking Guidance: What are the management’s projections for Q4 and the full fiscal year? Any change in guidance is a powerful signal to the market.

- •Segment Performance: How are OCI’s different business units (e.g., chemicals, renewable energy) performing? Strength or weakness in a key segment can significantly impact the overall outlook.

The key for investors will be to listen beyond the headline numbers. Management’s tone, confidence in their strategic plan, and transparency during the Q&A session often reveal more than the financial statements alone.

Potential Stock Price Scenarios Post-IR

The market’s reaction to the OCI Holdings IR will hinge on how the results compare to analyst expectations. While specific consensus data is pending, we can analyze three potential scenarios.

1. Positive Scenario (Stock Price Increase)

- •Earnings Beat: Announcing revenue and profit figures that surpass market expectations would signal strong operational health.

- •Optimistic Guidance: A confident outlook on future quarters or major new projects could significantly boost investor sentiment.

- •Shareholder-Friendly Policies: News of increased dividends or stock buyback programs would be highly attractive to investors.

2. Negative Scenario (Stock Price Decrease)

- •Earnings Miss: Failing to meet expectations could trigger a sell-off from disappointed investors.

- •Cautious Outlook: Citing macroeconomic headwinds, increased competition, or project delays could create uncertainty.

- •Unforeseen Challenges: Disclosure of unexpected operational issues or regulatory hurdles could negatively impact the stock.

Strategic Action Plan for Investors

To navigate the aftermath of the OCI Holdings Q3 2025 Earnings release, a proactive approach is essential. Consider the following steps:

- •Review Professional Analysis: Immediately after the call, review reports from major financial news outlets like Bloomberg and brokerage firms to understand the market’s initial reaction.

- •Analyze the Presentation Materials: Download the IR presentation and transcript. Meticulously read through them to find nuances and details missed in the initial summaries.

- •Deepen Your Fundamental Knowledge: Use this event as a catalyst to further your own research. A solid foundation in understanding key financial metrics will empower you to form independent conclusions.

- •Compare with Competitors: Benchmark OCI’s results against its main industry competitors. This contextualizes their performance and helps assess their market position.

By combining the company’s disclosures with external analysis and your own due diligence, you can develop a robust investment strategy for OCI Holdings. This upcoming IR is a critical data point in that ongoing process.