The recent announcement of the UTI rights offering for its subsidiary has sent ripples through the investment community, forcing shareholders to question whether this move is a stepping stone to future growth or a harbinger of financial strain. With KRW 11.2 billion on the line, UTI (179900) is making a bold play to fund new ventures, but this comes at the immediate cost of potential share dilution. This comprehensive UTI stock analysis will dissect the offering, evaluate the company’s fundamentals, and provide a clear investment strategy to help you navigate the uncertainty and make an informed decision.

Decoding the UTI (179900) Rights Offering

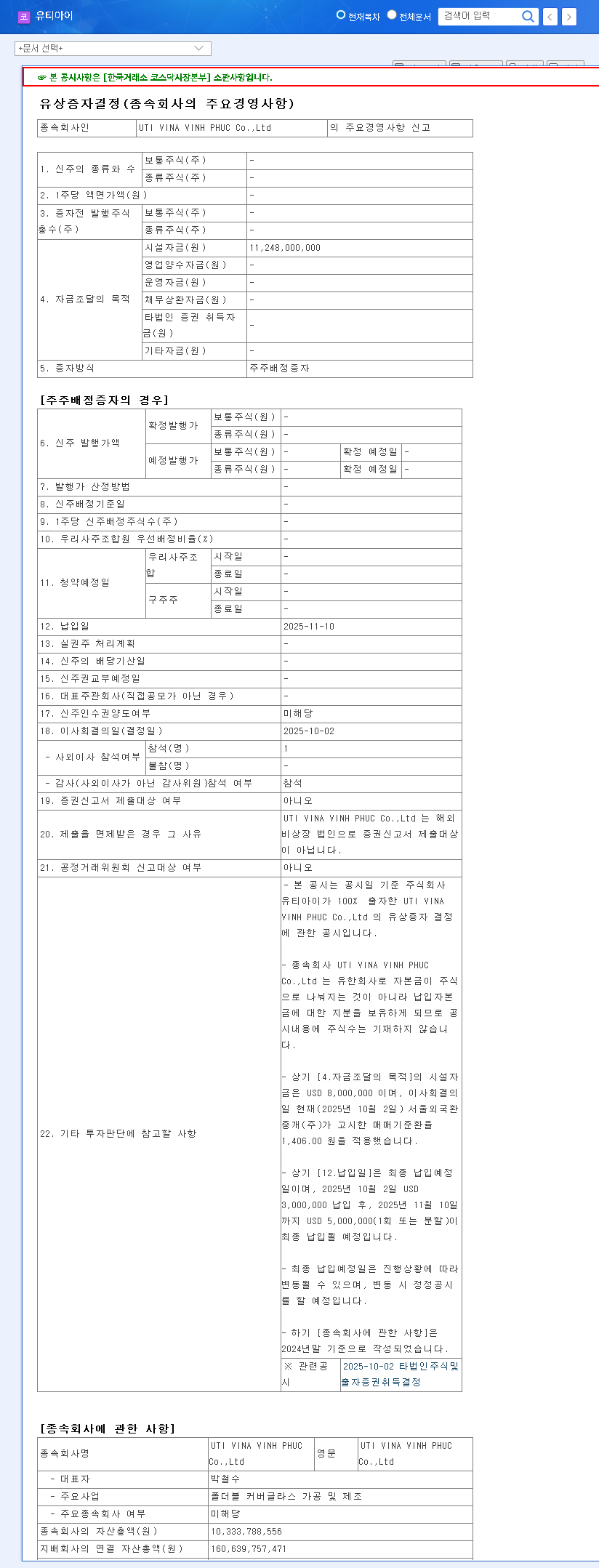

On October 2, 2025, UTI (179900) formally announced a shareholder-allocated rights offering to raise KRW 11.2 billion for its subsidiary, UTIVINAVINHPHUCCo.,Ltd. The primary stated purpose is to secure critical facility funds for expansion and technology development. This capital is earmarked for new, high-potential business lines, including Flexible Glass and TGV (Through-Glass Via) substrates, which the company sees as its future growth engines. You can review the Official Disclosure (Source) on DART for complete details. This move is a strategic pivot, but it’s one born out of necessity, considering the company’s current financial landscape.

The Driving Forces: Why Now?

A decision of this magnitude is rarely made in a vacuum. The UTI rights offering is a direct response to a confluence of internal and external pressures.

1. A Challenging Business Environment

UTI’s core business, the camera window segment, has faced significant headwinds. A general slowdown in the global smartphone market, coupled with fierce competition, led to a noticeable decline in sales during the first half of 2025. When a company’s primary revenue stream is under pressure, it must look for new avenues for growth, which requires capital that may not be readily available from operations.

2. Mounting Financial Pressures

The company’s balance sheet reveals a concerning trend. The issuance of convertible bonds and preferred shares has increased total liabilities while total capital has decreased, weakening the overall financial structure. Furthermore, the substantial R&D expenses necessary to stay competitive have widened operating losses. This combination of factors has contributed to a sustained downtrend in the stock price over the past year, making it difficult to raise capital through other means.

The rights offering is a classic corporate maneuver: raising capital from existing shareholders when debt markets are tight and the core business isn’t generating enough cash for ambitious expansion projects.

Impact Analysis: Opportunity vs. Share Dilution Risk

For investors, the central conflict is weighing the long-term potential against the short-term pain. The impact of this offering is decidedly two-sided.

The Bull Case: Fueling Future Growth

- •Secured Growth Capital: The KRW 11.2 billion provides the necessary runway to scale up new technologies like Flexible Glass, which could be a game-changer in the display industry.

- •Improved Liquidity: The immediate cash infusion will provide a much-needed boost to the company’s short-term liquidity, giving it more operational flexibility.

The Bear Case: Navigating the Downsides

- •Share Dilution: This is the most significant and immediate negative. Issuing new shares means each existing share represents a smaller piece of the company, which typically puts downward pressure on the stock price. To learn more about this effect, you can read this guide on understanding share dilution from a trusted financial source.

- •Weakened Investor Sentiment: In a volatile macroeconomic environment, a rights offering can be perceived as a sign of weakness, potentially scaring off new investors and causing existing ones to sell.

- •Execution Risk: The entire bull case hinges on UTI successfully bringing its new products to market. If these ventures fail or are delayed, the company will be left with a diluted share base and little to show for it.

Your Investment Strategy: Navigating UTI Stock Post-Offering

A one-size-fits-all approach is unwise. Your investment strategy should align with your risk tolerance and time horizon. Explore our other stock analysis articles for more insights.

For the Short-Term Investor/Trader:

The period surrounding the offering and the listing of new shares will likely be highly volatile. A cautious, if not bearish, stance is prudent. The downward pressure from share dilution is a powerful short-term force. Monitor price action closely and be prepared for sharp movements. This is a high-risk environment best suited for experienced traders.

For the Mid-to-Long-Term Investor:

The long-term outlook depends entirely on execution. Your focus should be on fundamental milestones:

- •Track New Business Performance: Look for concrete updates on mass production timelines, customer contracts, and revenue contributions from the Flexible Glass and TGV divisions.

- •Monitor Financial Health: Beyond this offering, watch for signs of improving profitability, debt reduction, and better cost controls.

- •Assess Core Business Recovery: Any signs of stabilization or recovery in the camera window business would be a major positive catalyst.

Ultimately, investing in UTI today is a bet on management’s ability to turn fresh capital into sustainable, profitable growth. While the short-term path is fraught with risk from the UTI rights offering, patient investors who see tangible progress in the company’s strategic pivot could be rewarded in the long run.