KOLMAR KOREA Co., Ltd. has released its much-anticipated Q3 2025 earnings report, revealing a narrative of impressive top-line growth set against a backdrop of tightening profitability. With consolidated revenue climbing robustly, the company continues to demonstrate its market strength. However, for discerning investors, the story lies deeper within the numbers. This detailed KOLMAR KOREA Q3 2025 earnings analysis will unpack the performance drivers, dissect the financial health, and outline the critical questions that need answers during the upcoming Investor Relations (IR) session.

While revenue growth signals strong market demand, the slight compression in operating margin is the central theme for investors heading into the company’s Q3 IR call. Understanding the strategy to navigate this is key.

Unpacking the Q3 2025 Financial Performance

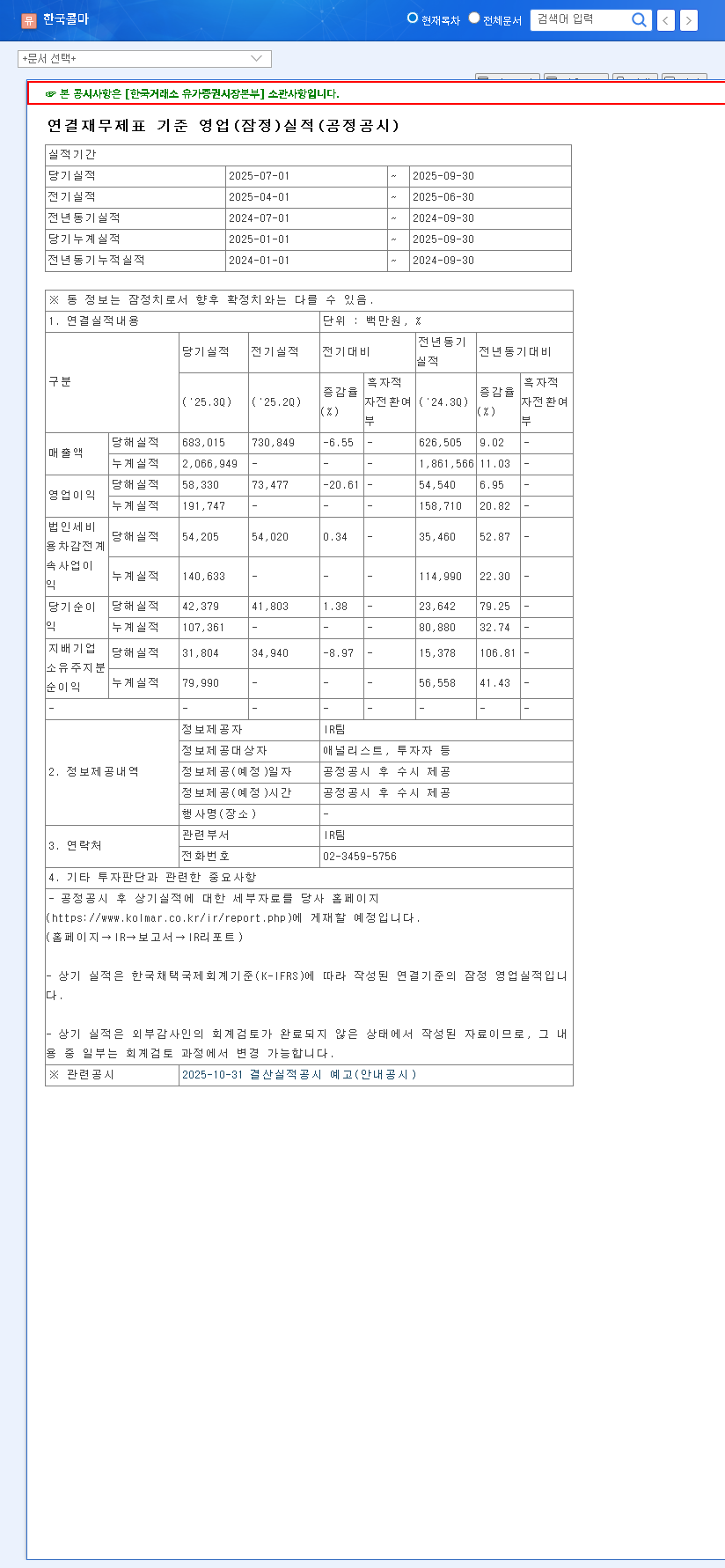

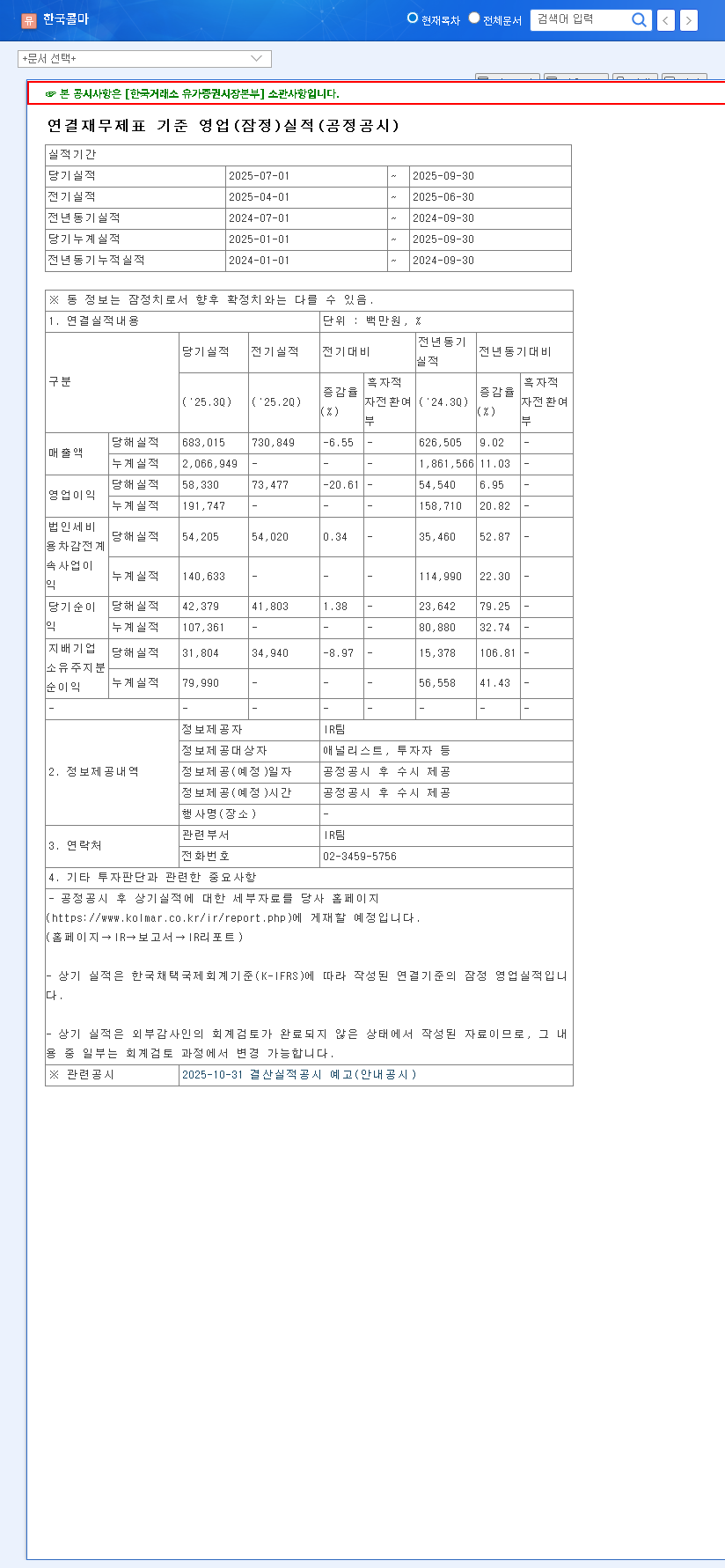

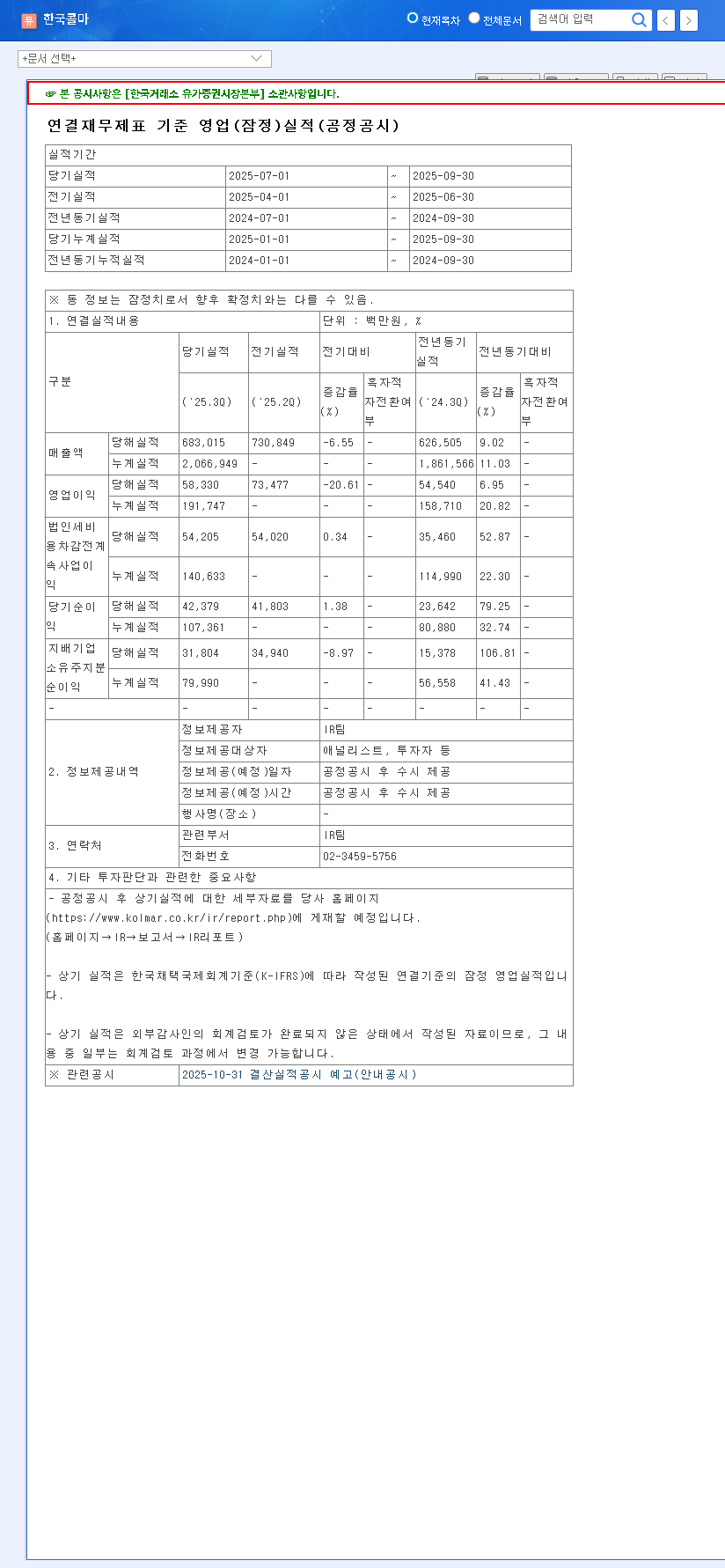

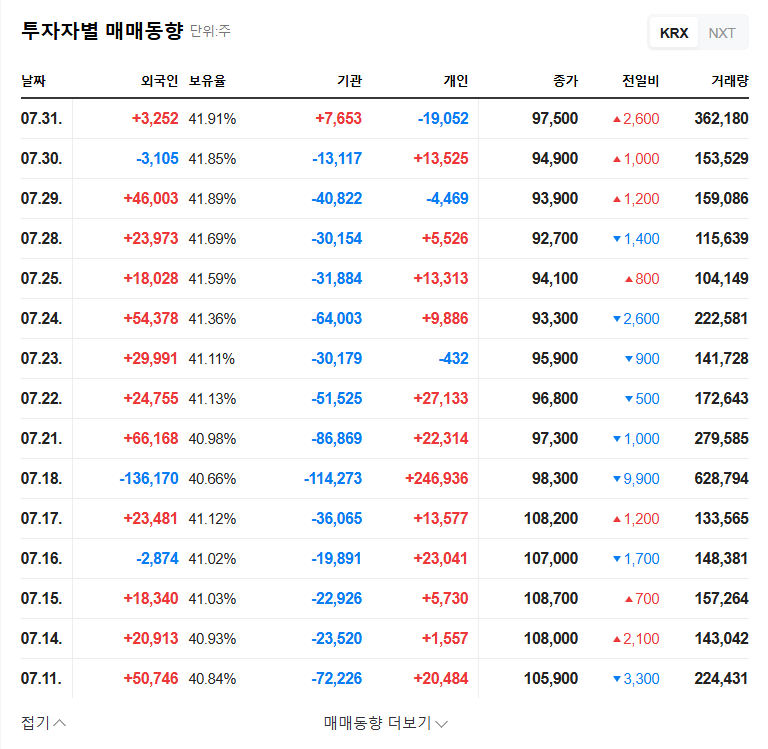

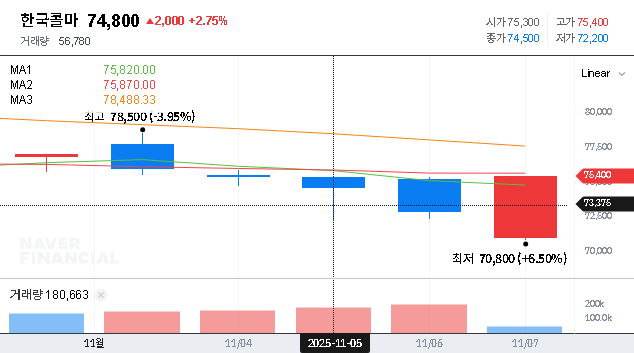

KOLMAR KOREA reported a strong quarter, with consolidated revenue reaching KRW 2.067 trillion, a significant 10.57% increase year-on-year. This growth showcases the company’s resilient position in its core markets. However, a closer look reveals a more nuanced picture.

Operating profit saw a marginal increase of 1.0% to KRW 191.7 billion, causing the operating profit margin to dip slightly to 9.28%. Net profit, on the other hand, jumped by 15.3% to KRW 107.4 billion, largely buoyed by non-recurring gains, including the disposal of investment assets. For a complete breakdown of the financial data, investors can refer to the Official Disclosure filed with DART.

Deep Dive: Business Segment Drivers & Challenges

Cosmetics Division (41.73% of Revenue)

The engine of KOLMAR KOREA’s growth remains its Cosmetics business. Capitalizing on the enduring global K-beauty trend, the company’s advanced Original Design Manufacturing (ODM) technology and reputation for quality have fueled exceptional performance. The basic skincare segment, in particular, has shown remarkable growth, solidifying the company’s leadership in this high-demand area.

Pharmaceutical Division (34.58% of Revenue)

The Pharmaceutical business continues to be a powerful contributor, largely thanks to the blockbuster success of ‘K-CAB,’ a new drug for gastroesophageal reflux disease. The consistent and strong sales of this flagship product have significantly bolstered the division’s performance. Looking ahead, the company is making substantial R&D investments to identify and develop the next wave of growth drivers, dubbed the ‘Post K-CAB’ pipeline.

The Profitability Puzzle: Why Margins Are Under Pressure

Despite the healthy revenue figures from the KOLMAR KOREA Q3 2025 earnings, the slight decline in operating margin is a critical point of analysis. This compression is not due to a single issue but a convergence of several external and internal factors.

- •Rising Input Costs: Global macroeconomic trends, such as volatile international oil prices, have directly led to higher raw material costs, squeezing margins.

- •Strategic R&D Investment: To secure its future, KOLMAR KOREA is heavily investing in research and development. While the R&D expenditure ratio remains stable at 5.28% of revenue, this necessary spending impacts short-term profitability.

- •Global Expansion Costs: As the company expands its international footprint, increased operating expenses from overseas subsidiaries have also contributed to the pressure on profitability.

Navigating these macroeconomic headwinds is crucial. Factors like currency fluctuations and interest rate hikes, as reported by authoritative sources like Bloomberg, present ongoing risks that demand proactive management.

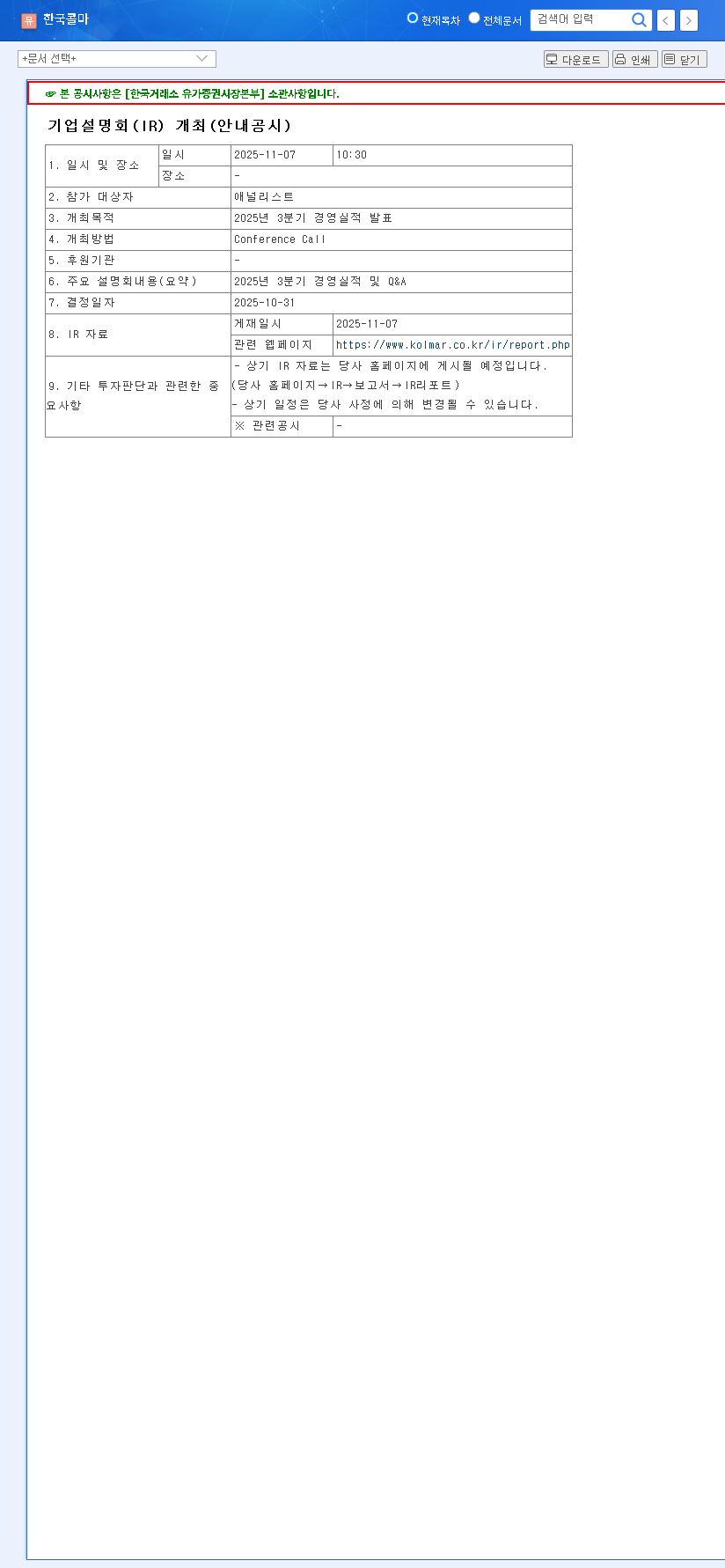

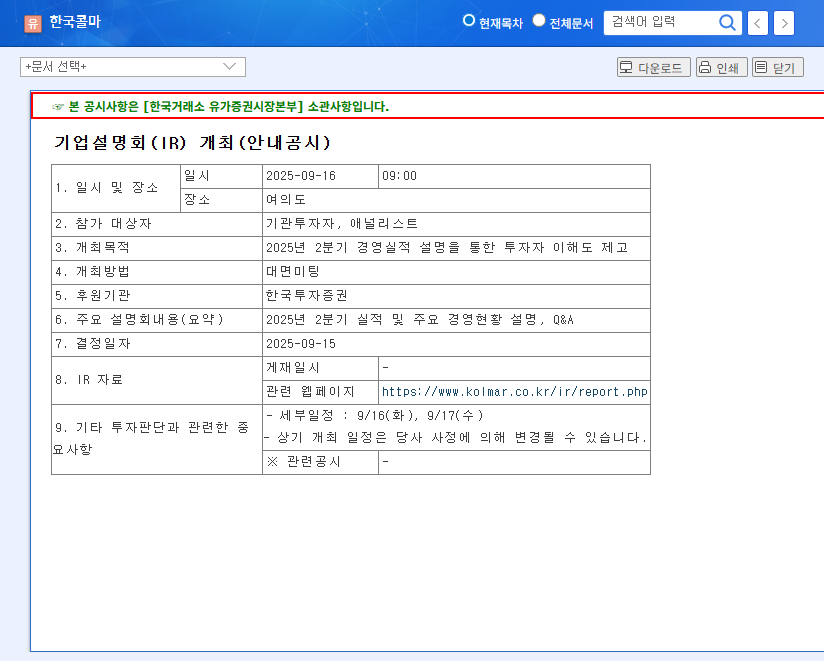

The Upcoming IR: Key Topics for Investors

The upcoming Investor Relations session is a pivotal moment for management to address these concerns and build confidence. Investors should pay close attention to the following areas:

Potential Positive Catalysts

- •A clear, data-backed strategy for improving profitability and managing costs.

- •A convincing roadmap for the ‘Post K-CAB’ pharmaceutical pipeline and other future growth engines.

- •Updates on ESG initiatives, such as eco-friendly packaging, which appeal to long-term institutional investors.

Potential Red Flags to Monitor

- •Vague or insufficient explanations for the decline in operating profit margin.

- •A lack of a concrete plan for mitigating macroeconomic risks like currency volatility.

- •Evasive answers during the investor Q&A session.

Investment Strategy & Outlook

The KOLMAR KOREA Q3 2025 earnings demonstrate a company with strong fundamentals and core competitiveness. The key to unlocking further value lies in management’s ability to articulate and execute a clear strategy for profitability enhancement. For investors, a long-term perspective is advisable, focusing on the company’s powerful market position in cosmetics and pharmaceuticals. Analyzing the upcoming IR content will be crucial for making informed decisions. For more context on the sector, you can read our Guide to Investing in K-Beauty Stocks.

Frequently Asked Questions (FAQ)

What were KOLMAR KOREA’s key Q3 2025 results?

KOLMAR KOREA reported Q3 2025 revenue of KRW 2.067 trillion, a 10.57% year-on-year increase. However, the operating profit margin saw a slight decline to 9.28% due to rising costs.

Which business segments drove revenue growth?

Growth was primarily driven by the Cosmetics business, leveraging the global K-beauty trend, and the Pharmaceutical business, powered by strong sales of its ‘K-CAB’ drug.

Why did KOLMAR KOREA’s profitability decline slightly?

The margin compression was due to a combination of factors, including higher raw material prices, increased strategic R&D spending for future growth, and higher operational costs from overseas expansion.

What are the main risks for KOLMAR KOREA investors?

Key risks include macroeconomic volatility (exchange rates, interest rates), sustained high raw material costs, and intensifying competition in both the cosmetics and pharmaceutical markets.