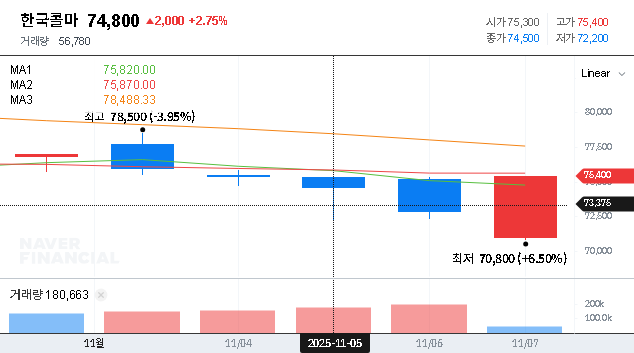

The recent preliminary earnings report for Q3 2025 has sent ripples through the investment community, directly impacting the outlook for KOLMAR KOREA stock. On November 7, 2025, the company announced figures that fell short of market consensus, sparking immediate concerns about short-term volatility and investor confidence. This comprehensive analysis will dissect the official report, explore the underlying causes of the underperformance, and provide a clear-eyed investment strategy for navigating the path forward.

Is this a temporary setback caused by macroeconomic headwinds, or does it signal a deeper issue with the company’s competitive edge? We will delve into KOLMAR KOREA’s fundamentals, long-term growth prospects, and the critical factors investors must monitor.

KOLMAR KOREA Q3 2025 Earnings: The Official Numbers

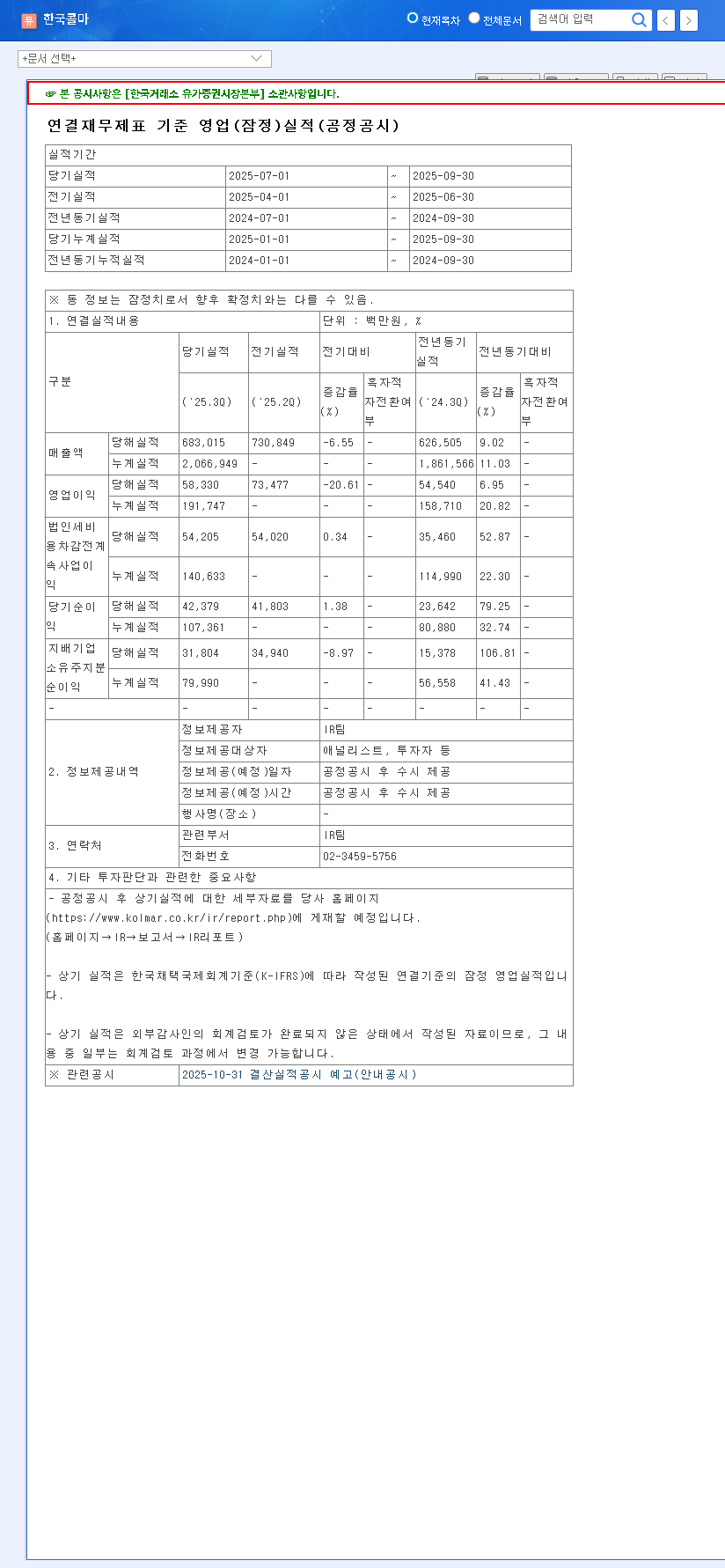

KOLMAR KOREA’s preliminary announcement revealed a noticeable gap between its performance and market expectations. The results, as detailed in the Official Disclosure, have raised important questions. Here is a breakdown of the key financial figures:

- •Revenue: KRW 683 billion, which was 2% below the market’s estimate of KRW 698.7 billion.

- •Operating Profit: KRW 58.3 billion, a significant 14% miss compared to the projected KRW 67.8 billion.

- •Net Income: KRW 31.8 billion, falling 19% short of the consensus estimate of KRW 39.5 billion.

This across-the-board underperformance suggests that multiple pressures are affecting the company’s profitability, prompting a deeper investigation into the contributing factors.

Why the Miss? Unpacking the Performance Headwinds

While the preliminary report lacks a detailed management discussion, we can infer the likely causes based on prevailing market conditions and the company’s previous financial statements. This KOLMAR KOREA earnings analysis points to a confluence of challenges.

Primary Factors Affecting Profitability

- •Cost Pressures: Volatility in global markets, particularly in crude oil prices, likely inflated the cost of raw materials and logistics. This directly squeezes profit margins if costs cannot be fully passed on to consumers.

- •Intense Competition: The cosmetics and pharmaceutical markets are highly competitive. Increased marketing and promotional spending to maintain market share can erode operating profit, even if revenue remains stable.

- •Subsidiary Performance: The ongoing profitability challenges at its subsidiary, Yeonwoo Co., Ltd., which were highlighted in previous reports, likely continued to drag on consolidated earnings.

- •Currency and Derivative Effects: A weaker Korean Won can be a double-edged sword. While it boosts the value of exports, it also increases the cost of imported raw materials. Furthermore, fluctuations in exchange rates and interest rates can lead to non-operating losses on derivative valuations. For more on this, see this guide on how currency affects international stocks.

In the short term, the market’s reaction to an earnings miss is often emotional. The key for a long-term investor is to separate temporary operational headwinds from a fundamental deterioration of the business model.

Navigating the Future: An Investment Strategy for KOLMAR KOREA

Given the increased uncertainty, a measured and strategic approach is vital. The immediate downward pressure on KOLMAR KOREA stock may present opportunities for investors with a long-term horizon, but careful consideration is required.

Actionable Steps for Investors

Before making any decisions, it’s crucial to adopt a disciplined investment strategy. Here are key areas to focus on:

- •Await Full Disclosure: Wait for the complete Q3 report and the subsequent earnings call. Management’s commentary will provide critical context on the causes of the miss and their plans for remediation.

- •Re-evaluate Core Fundamentals: Assess whether KOLMAR KOREA’s core strengths—its leading position in cosmetics ODM and the growth of HK inno.N’s pharmaceutical business—remain intact. For guidance, you can review our internal guide on how to analyze corporate fundamentals.

- •Monitor Macro-Indicators: Keep a close watch on interest rates, KRW/USD exchange rates, and commodity prices. These external factors will continue to influence profitability.

- •Analyze Future Guidance: The company’s guidance for Q4 2025 and the full year 2026 will be the most telling indicator of their confidence in a recovery.

In conclusion, while the Q3 2025 earnings are a clear setback, they do not necessarily invalidate the long-term investment case for KOLMAR KOREA. The company’s robust market position provides a strong foundation. However, prudent investors should demand clarity on the underlying issues and monitor the company’s execution of its strategy before committing new capital. This report is for informational purposes only and does not constitute investment advice.