When a company’s top executive personally invests more of their own money into the business, the market takes notice. This is precisely the situation following the recent INSAN Inc. stake increase by CEO Kim Yoon-se. Such a move, often called ‘insider buying,’ can be a powerful signal of confidence in a company’s future prospects. However, for savvy investors, it also prompts a critical question: Is this a genuine vote of confidence in growth, or an attempt to shore up stability amidst hidden risks? This comprehensive INSAN Inc. investment analysis will dissect the transaction, evaluate the company’s financial health, and explore the market environment to provide a clear, actionable perspective.

We’ll go beyond the headlines to empower you with the insights needed to determine if INSAN Inc. stock aligns with your investment strategy in light of this significant development.

The Official Filing: Deconstructing the CEO’s Share Purchase

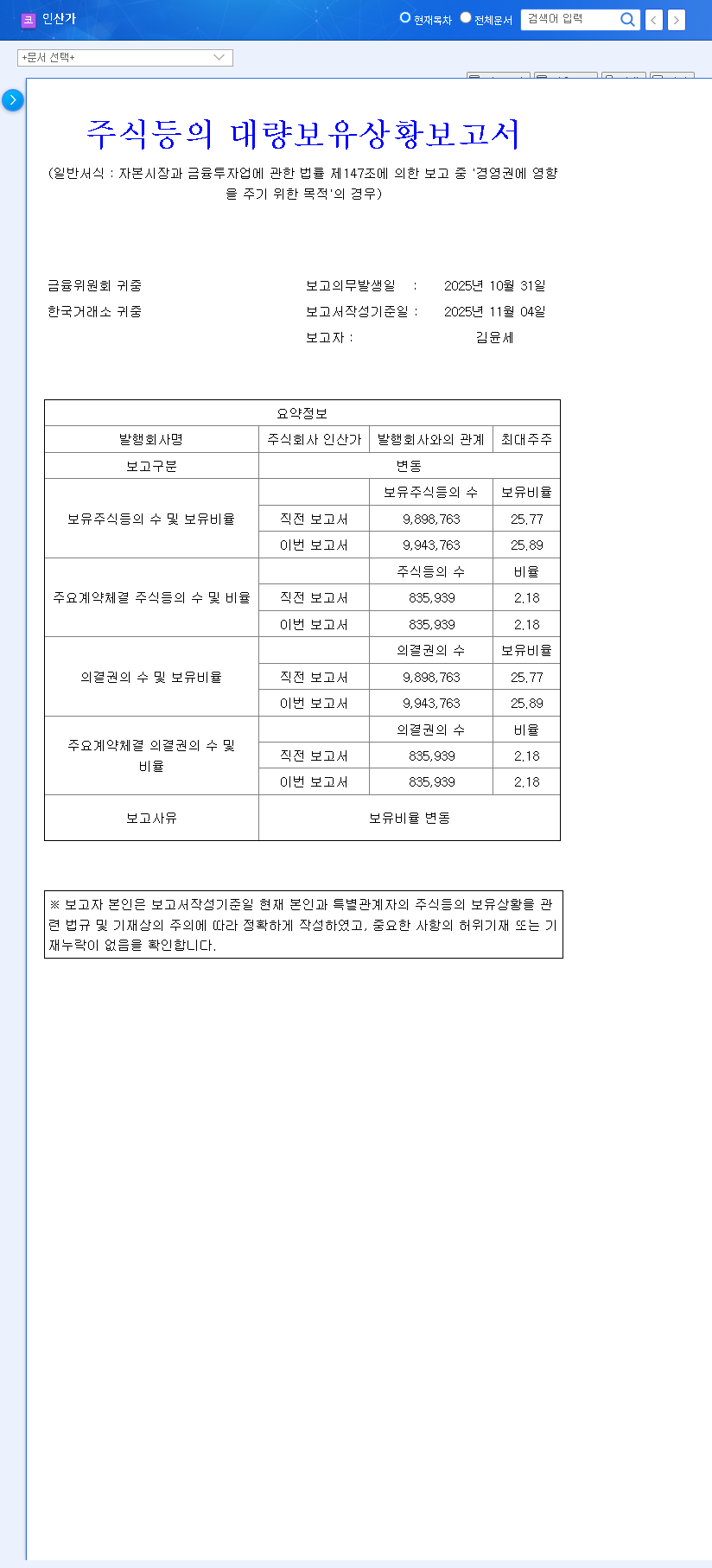

On November 4, 2025, a mandatory disclosure provided the concrete details of the CEO’s increased investment. The official report, filed with regulatory authorities, outlines the specifics of the transaction and is a crucial piece of evidence for any analysis.

Key Details from the Large-Scale Stock Holdings Report:

Reporting Officer: Kim Yoon-se (CEO & Largest Shareholder)

Purpose of Holding: Influence over management

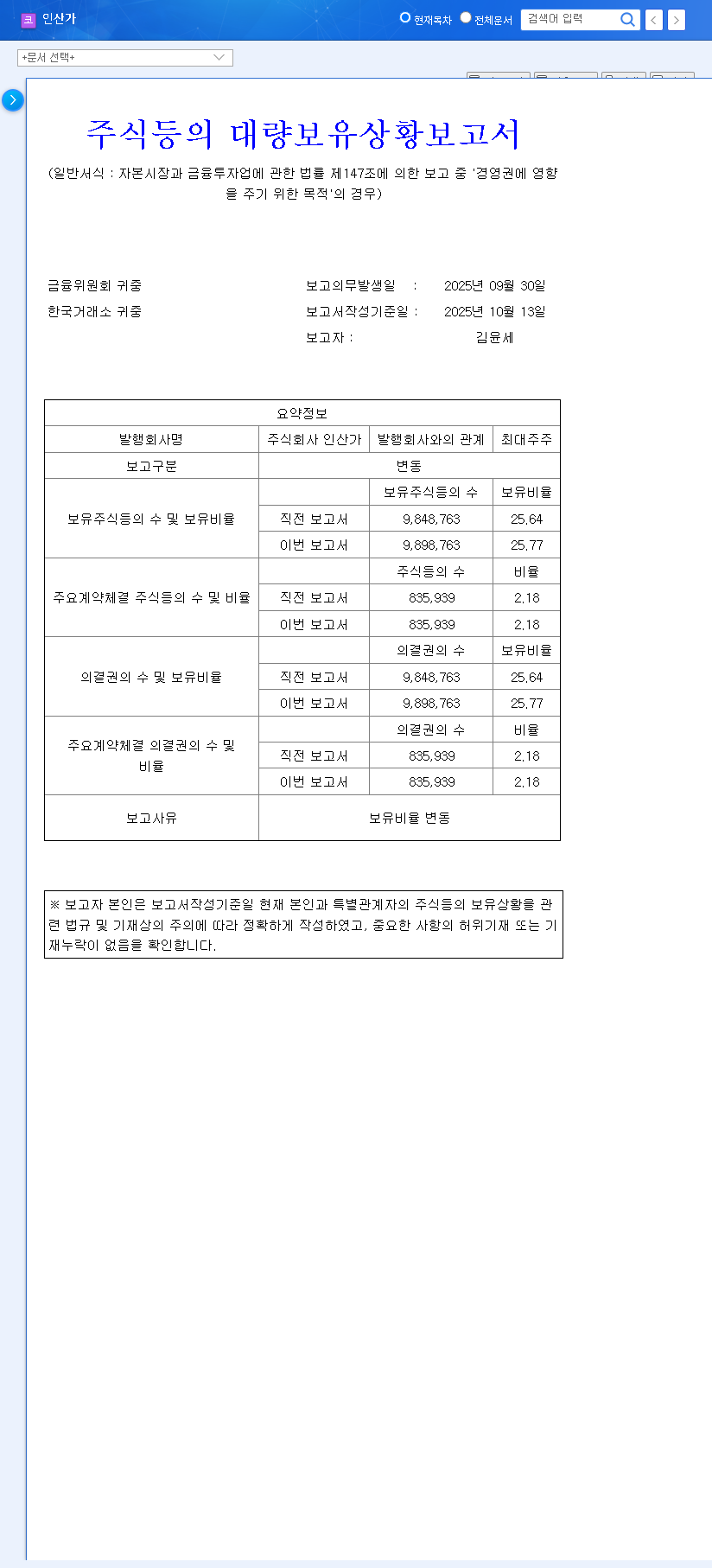

Ownership Before: 25.77%

Ownership After: 25.89%

Net Change: +0.12% (an acquisition of 45,000 common shares)

Source: Official Disclosure (DART)

The purchase was executed in two tranches: 30,000 shares on October 31 and 15,000 shares on November 3, 2025. While the percentage increase of 0.12% is modest, the declared purpose—’influence over management’—confirms the strategic intent behind the move. It signals a desire by CEO Kim Yoon-se to tighten his control and steer the company’s direction, a move that requires a deeper look into the company’s current operational state.

INSAN Inc.’s Financial Health: A Mixed Picture

To understand the context of the INSAN Inc. stake increase, we must analyze its underlying financial performance as of the first half of 2025. The numbers reveal a story of growing sales but also increasing financial strain.

Revenue and Profitability Analysis

On the surface, there’s good news. Revenue grew to 16,117 million KRW, a respectable 5.7% increase year-over-year. More impressively, the company swung from an operating loss of -551 million KRW to an operating profit of 306 million KRW. This turnaround suggests that core business operations, likely related to its signature Jukyeom (bamboo salt) products, are becoming more efficient, possibly through better sales and cost management. However, the picture darkens when we look at the bottom line. Net income loss widened significantly, from -365 million KRW to -774 million KRW. This discrepancy is due to rising non-operating expenses, such as higher financing costs and losses on derivative products, which are red flags for investors.

Balance Sheet and Debt Concerns

The company’s debt ratio is another area demanding caution. It climbed from 55.09% to 64.88%, driven by new corporate bonds and borrowings. While not yet at a critical level, this trend indicates increasing financial leverage and risk, especially in a high-interest-rate environment. For a deeper understanding of these metrics, investors can review resources on Understanding Financial Ratios for Stock Analysis.

Business Strategy & Market Headwinds

INSAN Inc. is not standing still. The company is actively working to diversify beyond its core Jukyeom products by expanding into Home Meal Replacement (HMR) and health foods. Furthermore, it is targeting global markets with its ‘K-LAVA SALT’ brand, a crucial initiative for long-term growth. However, it operates in a challenging macroeconomic climate. As noted by leading financial sources like Reuters, persistent high interest rates globally increase borrowing costs, while currency fluctuations and volatile oil prices can impact everything from raw material costs to international shipping expenses. These external pressures add a layer of uncertainty to the company’s growth plans.

Investment Thesis: Bull Case vs. Bear Case

The Bull Case (Positive Signals)

- •Executive Confidence: The CEO’s purchase is a tangible sign of belief in the company’s long-term strategy and a commitment to shareholder value.

- •Management Stability: A strengthened leadership position can lead to more decisive and stable long-term planning, reducing governance risk.

- •Market Sentiment: Insider buying often creates positive short-term momentum for a stock as it attracts the attention of retail and institutional investors.

The Bear Case (Points of Caution)

- •Fundamental Weakness: The CEO’s buy doesn’t erase the widening net loss or the rising debt ratio. These fundamental issues must be resolved for sustainable growth.

- •Symbolic vs. Substantive: A 0.12% increase is not a game-changer in terms of control. Its impact is more psychological than structural.

- •Historical Volatility: INSAN Inc. stock has a history of sharp price swings. This news could potentially trigger another bout of volatility rather than a steady climb.

Final Verdict: A ‘Neutral’ Stance with Vigilant Monitoring

After a thorough INSAN Inc. investment analysis, our position is currently ‘Neutral.’ The CEO’s stake increase is a notable positive signal of commitment and could provide short-term support for the stock price. However, it is not enough to outweigh the underlying financial concerns, namely the widening net losses and increasing debt.

The prudent strategy for investors is to remain on the sidelines while closely monitoring key performance indicators in the upcoming quarters. Watch for signs of improvement in the company’s financial structure, tangible results from its new business ventures, and how it navigates the macroeconomic environment. An upgrade to our investment opinion would be contingent on seeing concrete proof that the company is addressing its fundamental financial challenges.