The latest KCC GLASS Corporation Q3 2025 earnings report, released on November 5, 2025, has sent mixed signals to the market. While the company grapples with persistent losses and a challenging macroeconomic environment, a slight outperformance in operating profit against bleak forecasts offers a sliver of hope. For investors evaluating KCC GLASS Corporation stock, this report demands a nuanced interpretation. This in-depth analysis unpacks the critical figures, explores the underlying causes, and provides a clear investment outlook for the road ahead.

Facing a downturn in the domestic construction market and escalating raw material costs, the company’s path to profitability is fraught with challenges. We will examine the performance of its core segments, assess its financial health, and identify the key catalysts and risks that investors must monitor closely.

KCC GLASS Corporation Q3 2025 Earnings: The Headline Figures

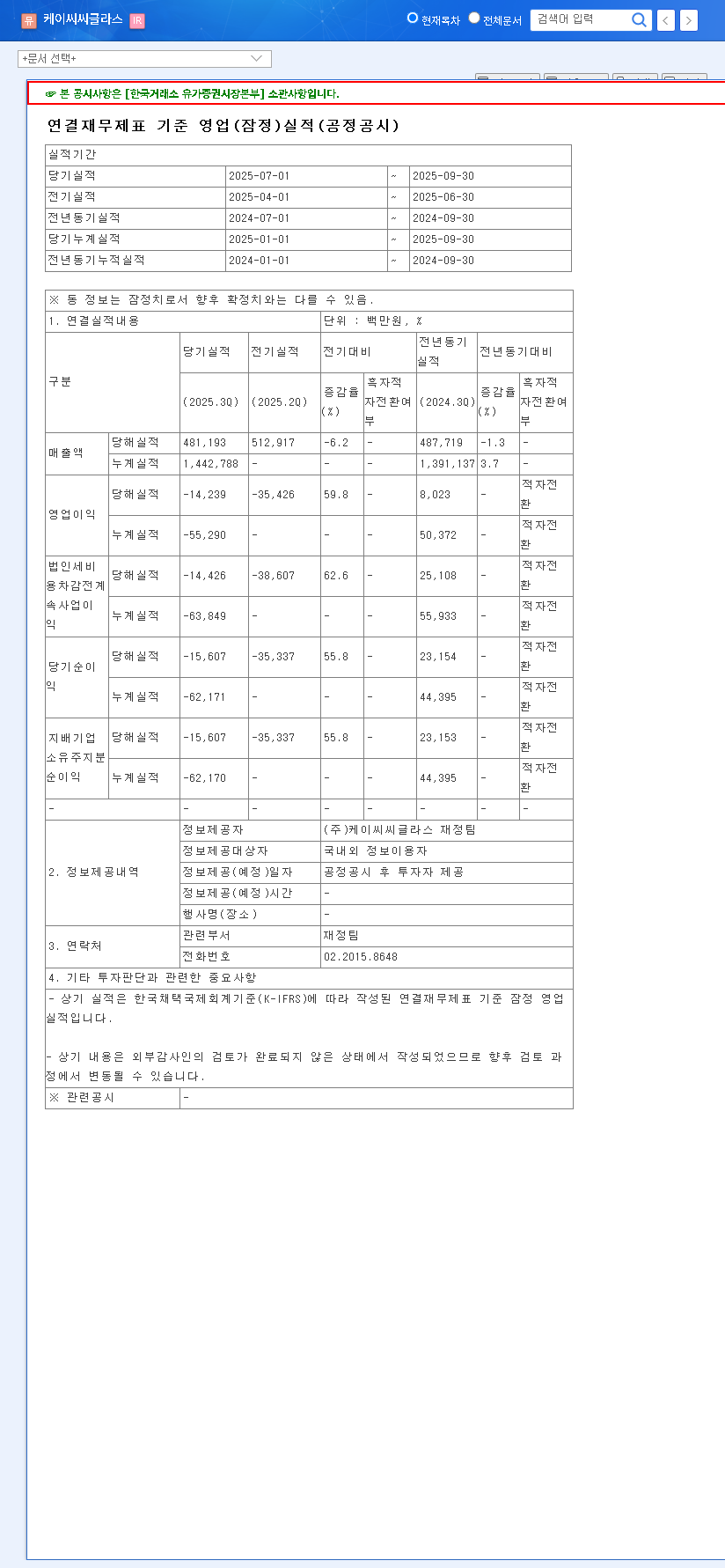

The provisional third-quarter KCC financial report presented a complex picture. Here’s a breakdown of the key performance indicators compared to market consensus, based on the Official Disclosure:

- •Revenue: KRW 481.2 billion, falling 3% short of the market expectation of KRW 497.7 billion.

- •Operating Profit: A loss of KRW -14.2 billion, which, while negative, was 10% better than the forecasted loss of KRW -15.8 billion.

- •Net Profit: A significant loss of KRW -15.6 billion, confirming a shift into the red for the bottom line.

The revenue miss highlights the ongoing demand weakness, particularly from the construction sector. However, the better-than-feared operating loss suggests that some internal cost control measures may be starting to take effect, or that the market’s pessimism was slightly overblown. Nevertheless, the overarching theme remains one of financial pressure.

Fundamental Analysis: Why is Profitability Worsening?

The Q3 results are not an anomaly but a continuation of a trend seen in the first half of 2025, where the company recorded a company-wide operating loss of KRW 41.1 billion. The core issues are multifaceted, stemming from both internal segment dynamics and external market forces.

The Glass Segment: Hit by Construction Slump

The primary drag on performance is the glass division. A slowdown in domestic construction and real estate development has directly reduced demand for architectural glass. This has been compounded by increased price competition from low-cost imports, squeezing margins and leading to an expanded operating loss for the segment. This is a critical area for any KCC investment analysis.

Interior & Distribution: A Story of Unprofitable Growth

Conversely, the interior and distribution segments saw impressive revenue growth of nearly 22%. However, this growth came at a steep price, with operating profit in this division falling by over 45%. This indicates that the company is spending heavily to capture market share in a fiercely competitive environment, with increased marketing costs and investments eroding profitability.

The core dilemma for KCC GLASS Corporation is balancing top-line growth in its interior segment with the urgent need to stabilize its core glass business and restore overall profitability in a high-cost, low-demand environment.

Macroeconomic and Financial Headwinds

The company’s performance is intrinsically linked to broader economic trends. High interest rates, set by the Bank of Korea at 2.50%, increase the financing costs for KCC’s substantial liabilities (KRW 948.8 billion as of H1 2025) and dampen construction activity. Furthermore, as noted by leading financial analysts at Reuters, global supply chain pressures and volatile energy prices directly impact raw material costs for glass manufacturing. The high KRW/USD exchange rate (1,444.00) is a double-edged sword: it helps export competitiveness but inflates the cost of imported raw materials.

A crucial variable for future growth is the performance of its overseas operations, particularly the new plant in Indonesia. Stabilizing this facility and expanding export sales could provide a much-needed buffer against domestic market weakness. For more on this, you can read our analysis on the global manufacturing outlook.

Investment Strategy and Key Considerations

Given the KCC GLASS Corporation Q3 2025 earnings, our investment opinion remains ‘Neutral.’ The persistent losses and revenue miss are likely to weigh on the stock price in the short term. However, long-term investors should watch for signs of a turnaround. Positive catalysts could emerge from a recovery in the construction market or clear evidence that the company’s cost-cutting and efficiency strategies are yielding tangible results.

Investor Action Plan: What to Monitor

- •Construction Market Indicators: Closely track housing starts, construction permits, and real estate market sentiment in South Korea.

- •Profit Margin Trends: Look for sequential improvement in operating and net profit margins in subsequent quarterly reports.

- •Overseas Performance: Monitor news related to the Indonesian plant’s production levels, efficiency, and export sales figures.

- •Management Commentary: Pay attention to the company’s forward-looking statements on cost management, debt reduction, and strategic priorities.