RS AUTOMATION CO.,LTD. (140670) Investment Analysis

A recent major disclosure from RS AUTOMATION CO.,LTD. (140670) has caught the attention of the market: CEO Kang Deok-hyun has significantly increased his ownership stake. This move, officially intended to strengthen management control, sends a powerful signal to current and potential investors. But what does this insider confidence mean when weighed against the company’s recent performance and the challenging macroeconomic climate? This comprehensive analysis will break down the event, dissect the company’s fundamentals, and provide a clear investment perspective.

We will explore the implications of this shareholding change, the impact of the associated rights issue, and whether the long-term potential in the robot motion control market outweighs the short-term financial headwinds facing RS AUTOMATION CO.,LTD.

The Core Event: CEO Stake Increase Explained

1. What Happened?

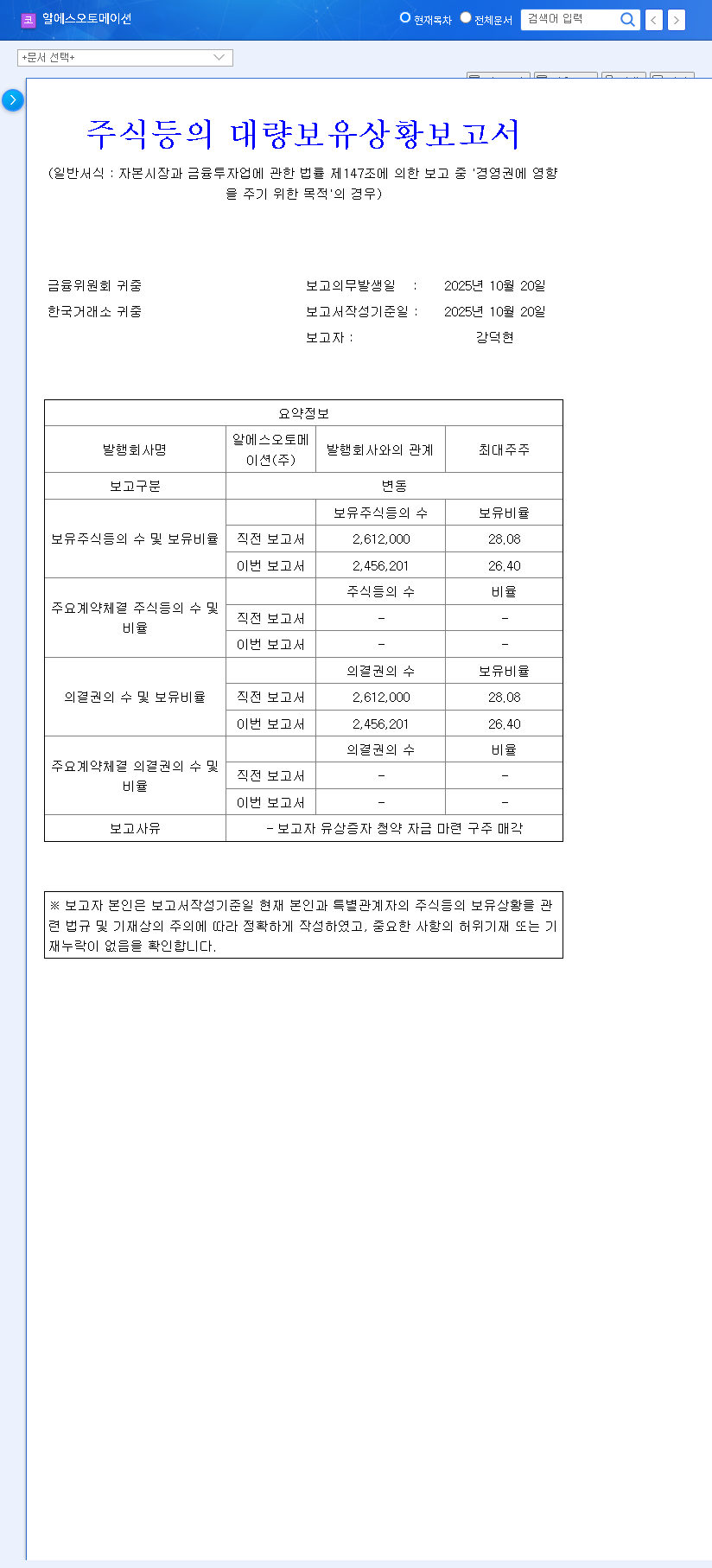

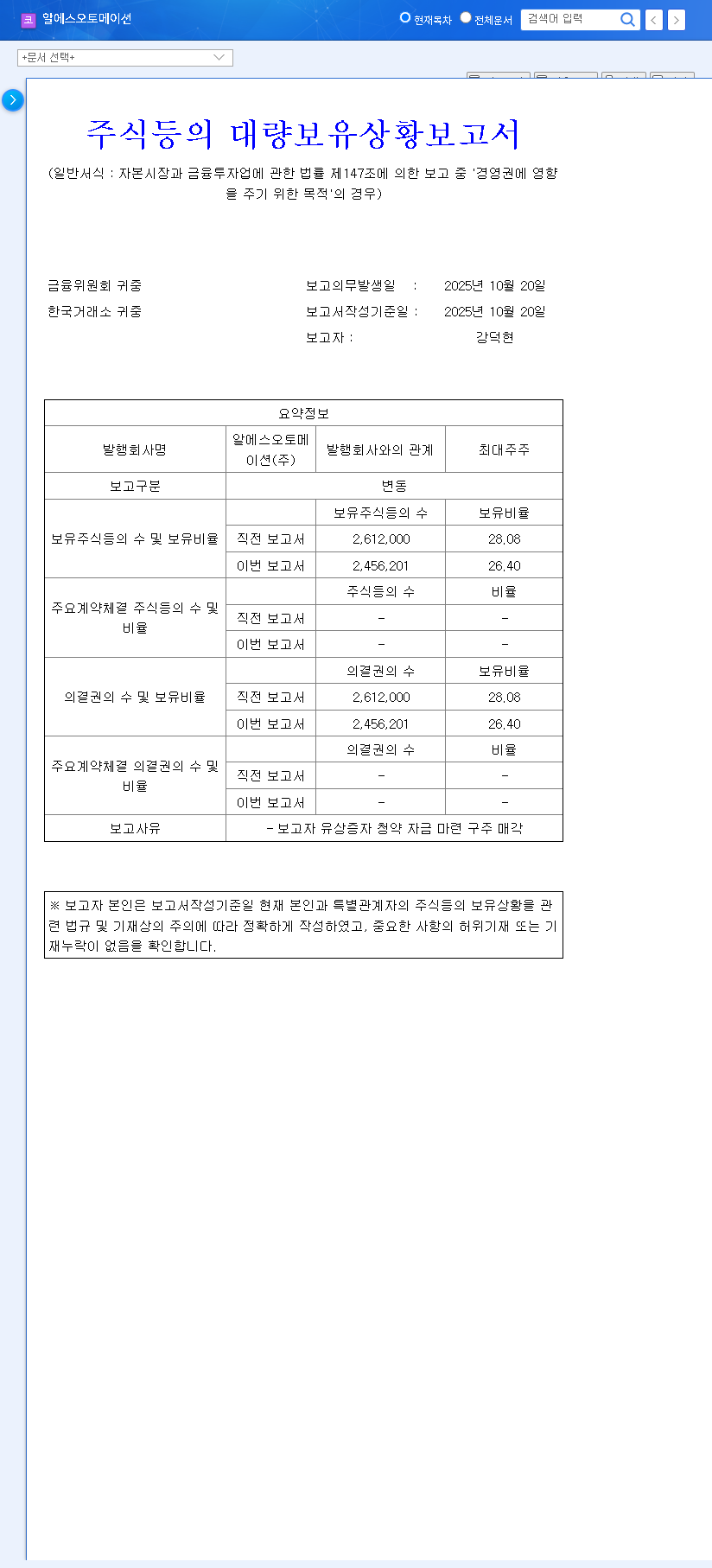

On October 27, 2025, a mandatory disclosure was filed detailing a significant change in the ownership structure of RS AUTOMATION CO.,LTD. The key takeaway is that CEO Kang Deok-hyun increased his personal shareholding by 2.15 percentage points, moving from 26.40% to 28.55%. This was achieved through a strategic allocation of new share warrants from a rights issue, followed by off-market sales. The officially stated purpose was to bolster ‘influence over management.’ You can view the Official Disclosure (Source) for complete details.

2. Why It Matters: Interpreting the CEO’s Actions

An insider increasing their stake is often viewed as one of the strongest bullish signals. It suggests that the person with the most intimate knowledge of the company’s operations, challenges, and future prospects believes the stock is undervalued. This act of strengthening management control can also reassure investors that leadership is stable and committed to a long-term vision, reducing concerns about potential hostile takeovers or rudderless strategy.

While the CEO’s increased ownership is a vote of confidence, investors must balance this against the dilutive effect of the rights issue and the company’s recent profitability challenges to form a complete picture.

Deep Dive: Corporate & Macroeconomic Analysis

Corporate Fundamentals of RS AUTOMATION CO.,LTD.

An analysis of the company’s 2024 financials reveals a period of difficulty. Revenue saw a 5.5% year-over-year decrease to 76.8 billion won, accompanied by a double-digit slide in operating profit. This points to a significant deterioration in profitability, likely driven by sluggishness in the key semiconductor and display industries. For more information on this sector, you can read our guide to the semiconductor industry outlook.

- •Financial Structure: The debt-to-equity ratio has climbed to a concerning 135.2%, indicating increased financial risk.

- •Inventory Management: On a positive note, inventory turnover has improved to 5.0 rotations. However, the overall inventory level remains high, which could tie up capital.

- •Future Investment: The company is not standing still. R&D expenses have risen to 6.39% of revenue, signaling a firm commitment to innovation and securing future growth drivers in the promising robot motion control and energy sectors.

Macroeconomic & Industry Headwinds

The company operates in a complex global environment. A rising KRW/USD exchange rate could increase import costs for raw materials, while volatile oil prices add uncertainty to operational expenses. Furthermore, while central bank interest rates are on hold, persistent concerns about a global economic slowdown could continue to dampen investment and demand in the industrial automation sector. However, the long-term outlook for automation and robotics remains strong, as detailed in reports by authorities like the International Federation of Robotics.

Investment Thesis & Action Plan

Overall Assessment: A Tale of Two Stories

The investment analysis for RS AUTOMATION CO.,LTD. presents a classic conflict between short-term pain and potential long-term gain. On one hand, CEO Kang Deok-hyun’s stake increase is a powerful endorsement from the inside. The company’s focus on high-growth sectors like robotics and its dedication to R&D are commendable. On the other hand, the deteriorating 2024 financials, high debt ratio, and potential for share dilution from the rights issue present clear and immediate risks.

Recommended Investment Strategy

Given the mixed signals, a patient and watchful strategy is advised.

- •Short-Term (3-6 Months): Adopt a Conservative Observation approach. Monitor the 140670 stock price closely for volatility caused by the off-market sales and rights issue absorption. Wait for the next quarterly earnings report to see if profitability trends are beginning to reverse.

- •Long-Term (1-3 Years): Base decisions on tangible results. Look for evidence that R&D investments are leading to new products or market share gains. A significant improvement in the debt-to-equity ratio and a sustained turnaround in the semiconductor sector would be strong buy signals.

Disclaimer: The contents of this report are for informational purposes only and are not intended as investment advice or recommendations.