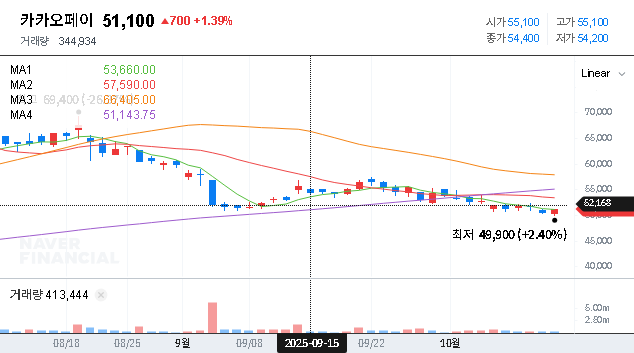

The latest kakaopay Corp. Q3 2025 earnings report has sent a shockwave through the fintech community, revealing a significant revenue shortfall that has investors asking critical questions. The South Korean digital finance giant announced provisional results that missed market expectations by a wide margin, particularly on the top line, raising immediate concerns about its growth trajectory and short-term stock performance.

Is this a temporary setback in a challenging macroeconomic environment, or does it point to deeper issues within kakaopay’s core business segments? This comprehensive analysis will dissect the official Q3 2025 figures, explore the underlying causes of the revenue miss, evaluate the company’s fundamental strengths, and provide a balanced outlook on the future of kakaopay stock for prospective investors.

Breaking Down the kakaopay Corp. Q3 2025 Earnings Results

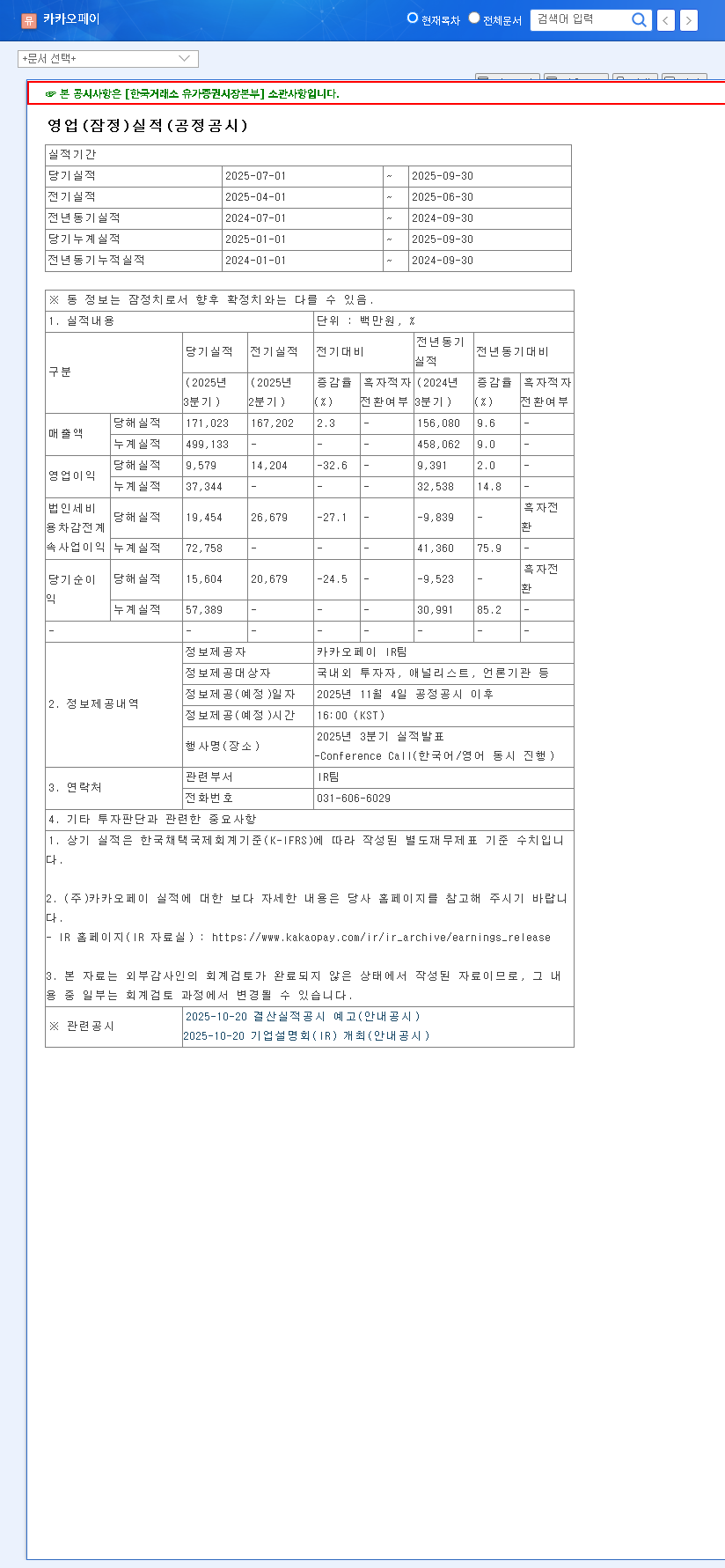

kakaopay Corp. released its provisional third-quarter earnings, which immediately caught the market’s attention due to a significant deviation from analyst consensus. The most alarming figure was the revenue, which fell short by over 30%. Here’s a detailed breakdown of the key metrics compared to market expectations (consensus), based on the Official Disclosure:

- •Revenue: KRW 171 billion (a 30.3% miss compared to the market expectation of KRW 245.3 billion).

- •Operating Income: KRW 9.6 billion (largely in line with expectations, only 1.0% below the consensus of KRW 9.7 billion).

- •Net Income: KRW 15.6 billion (an 8.8% miss compared to the market expectation of KRW 17.1 billion).

While the company managed to keep its operating income stable, the dramatic revenue shortfall is the primary concern. This suggests that while cost controls may be effective, the core engine of growth—its payment and financial services—may be sputtering, a worrying sign for a company valued on its expansion potential.

Why the Disappointing Results? A Deeper Analysis

1. Financial Health and Recent Performance

Despite the Q3 stumble, kakaopay’s recent financial journey has shown resilience. The company successfully transitioned from an operating loss in late 2024 to profitability in early 2025, a significant milestone. Furthermore, its capital adequacy remains strong, providing a buffer for future investments. However, the Q3 revenue figure marks a sharp reversal from the previous quarter’s growth, demanding scrutiny. While net income has trended upwards, revenue is the lifeblood of a growth-focused tech company, and this slowdown cannot be ignored.

2. Core Business Competitiveness and Market Pressures

kakaopay’s strength lies in its ecosystem, deeply integrated with the Kakao Group. Its core segments have distinct advantages but also face headwinds:

- •Payment Services: While still a market leader, this segment is facing intense competition from rivals like Naver Pay and Toss, potentially leading to fee compression and a fight for merchant exclusivity.

- •Financial Services: This has been a key growth driver, with loan comparison, investment, and insurance products boosting average revenue per user (ARPU). However, this segment is highly sensitive to macroeconomic factors like interest rates, which can dampen loan demand.

- •Platform Services: Advertising and money transfers are vital for user engagement but may have experienced a slowdown in line with broader consumer spending trends.

The core challenge for kakaopay is clear: Can it reignite top-line growth amidst fierce competition and economic uncertainty, or will this quarter mark the beginning of a new, slower-growth era?

Future Outlook: The Bull vs. Bear Case for kakaopay Stock

The Bull Case (The Optimist’s View)

Investors with a long-term horizon might see this as a buying opportunity. The bullish argument rests on kakaopay’s solid fundamentals, its powerful brand recognition, and immense cross-selling potential within the Kakao ecosystem. The company’s financial health is robust, and its ability to maintain operating profit despite the revenue drop shows disciplined management. As a leader in the ongoing digital transformation of South Korea’s financial sector, the long-term structural growth story remains intact. This quarter could be a temporary blip caused by short-term market conditions, as detailed in reports from financial experts like Bloomberg.

The Bear Case (The Skeptic’s View)

The bearish perspective is that the Q3 2025 earnings report reveals a crack in the growth narrative. The revenue miss could signal that the domestic market is reaching saturation and that competition is eroding kakaopay’s market share more than anticipated. Bears will argue that the stock’s valuation is predicated on high growth, and if that growth falters, a significant price correction is justified. Potential regulatory hurdles and the ongoing investigation by the Personal Information Protection Commission add layers of risk that cannot be dismissed.

Conclusion: A Strategic Approach for Investors

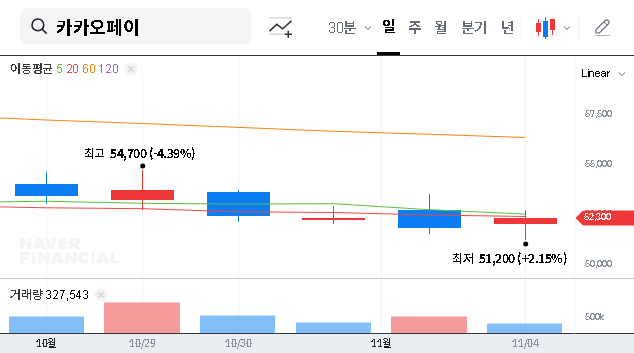

The kakaopay Corp. Q3 2025 earnings report is undeniably a negative short-term catalyst. The market will likely punish the stock for the revenue miss, leading to increased volatility. However, savvy investors should look beyond the immediate reaction.

A cautious but strategic approach is warranted. Rather than making a rash decision, investors should closely monitor management’s explanation for the revenue slowdown and their articulated strategy for re-accelerating growth in the upcoming quarters. Key metrics to watch will be user growth, transaction volume, and, most importantly, the ARPU from financial services. The company’s ability to innovate and successfully launch new products will be crucial. For those interested in the broader market, see our analysis of the wider fintech industry.

Ultimately, the investment decision depends on one’s belief in kakaopay’s ability to navigate current headwinds and capitalize on its long-term potential as a dominant financial platform. This quarter’s results serve as a critical test of that thesis.