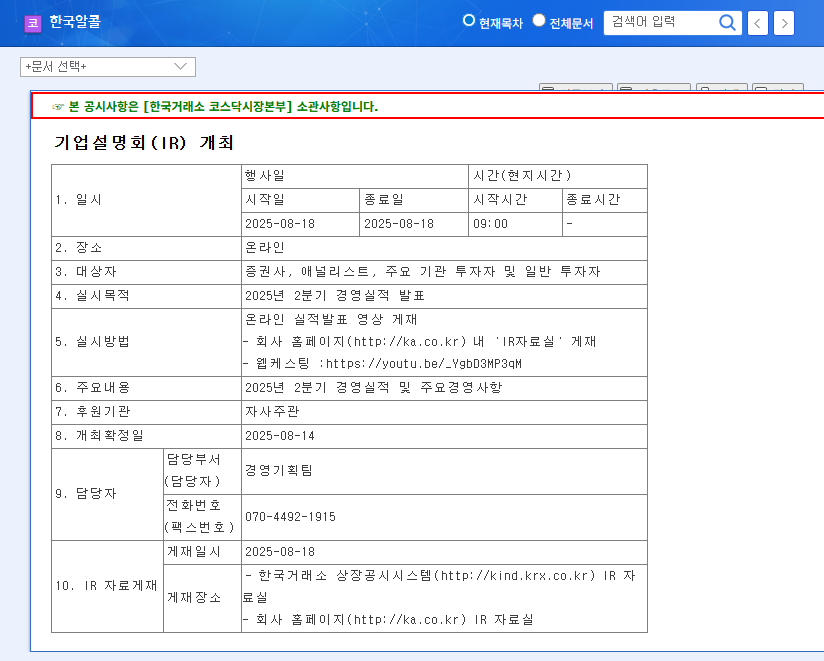

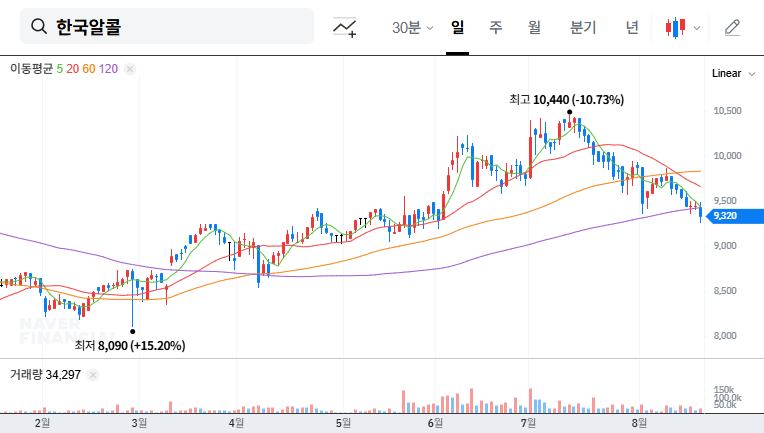

As the upcoming KoreaAlcoholIndustrial Q3 2025 earnings investor relations (IR) call on November 17, 2025, approaches, investors are keenly watching. KoreaAlcoholIndustrial (KAI), a pivotal player in the specialty chemical sector, is set to reveal its performance and strategic direction. This analysis provides a deep dive into the company’s financial standing, operational strengths, and the market risks that could shape its future. We will dissect the key factors to watch during the IR call, offering a data-driven investment outlook to help you make informed decisions about this unique ethyl acetate producer.

This report synthesizes information from the company’s latest quarterly filing, which can be viewed in the Official Disclosure, to provide a comprehensive KAI stock analysis.

Understanding KoreaAlcoholIndustrial’s Core Business

KoreaAlcoholIndustrial operates a dual-engine business model focused on chemical manufacturing and real estate. The chemical division is the company’s cornerstone, primarily involved in producing ethyl alcohol (ethanol) and various chemical products. A key competitive advantage is its status as the sole domestic producer of ethyl acetate, a crucial solvent used in paints, coatings, and adhesives. This market dominance provides a stable foundation.

Furthermore, KAI is strategically expanding into the high-purity organic solvent market, a move aimed at capturing higher-margin opportunities within the electronics and pharmaceutical industries. Complementing its industrial operations, the company’s real estate leasing arm, particularly its assets in the United States, generates consistent, stable rental income, adding a layer of financial diversification and resilience.

KAI’s unique position as the only domestic ethyl acetate producer, combined with its rock-solid financial health, makes it a compelling, albeit complex, investment case in the current macroeconomic climate.

Financial Health & Q3 Performance Highlights

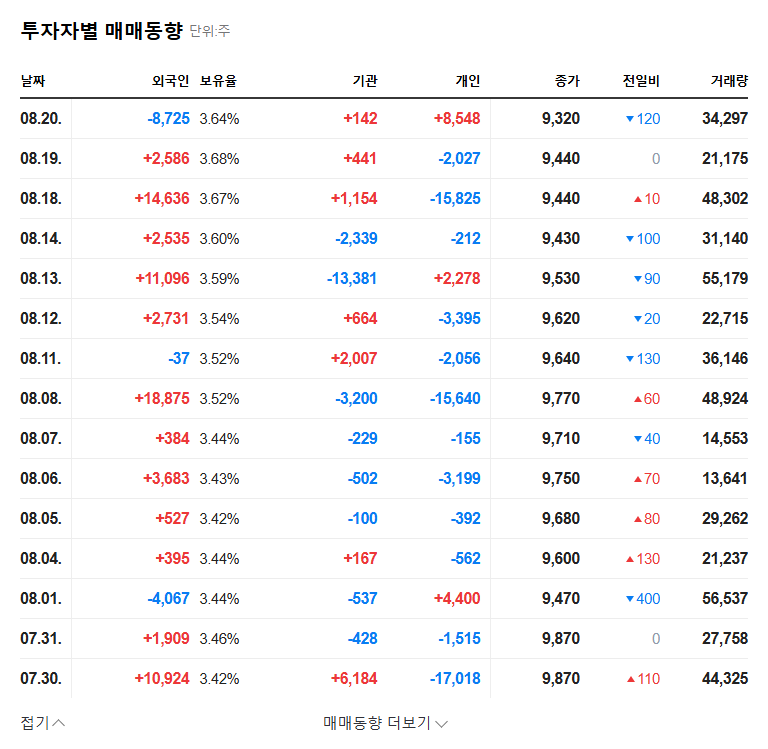

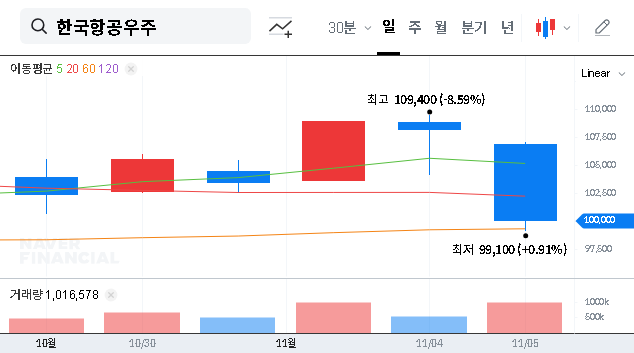

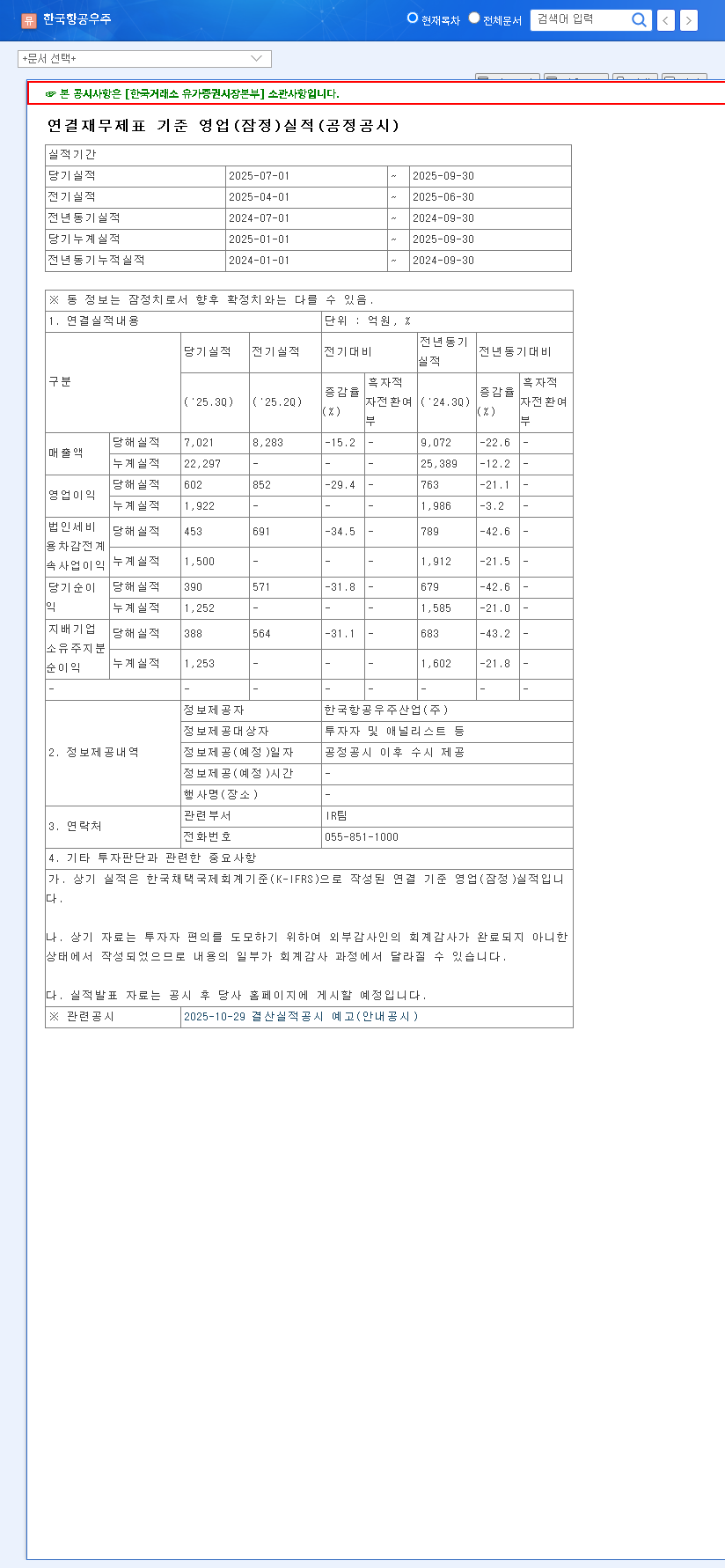

The upcoming KoreaAlcoholIndustrial Q3 2025 earnings report is expected to reaffirm the company’s robust financial position. Despite a minor dip in cumulative sales, the initial data points to a positive trajectory in profitability.

Key Strengths to Consider

- •Profitability Growth: Despite market headwinds, operating profit has seen a year-over-year increase. More impressively, net income has surged, largely due to strong performance from its equity-method investees.

- •Impeccable Financial Stability: With a remarkably low debt-to-equity ratio of just 18% and a negative net borrowing ratio, KAI boasts a fortress-like balance sheet. This minimizes its vulnerability to interest rate hikes and provides substantial capacity for future investment.

- •Future-Focused R&D: The company is actively investing in research and development for eco-friendly products and next-generation petrochemical materials, signaling a commitment to securing long-term growth engines.

- •Diversified Revenue Streams: The steady income from the US-based real estate portfolio provides a reliable buffer against the inherent volatility of the chemical industry. For a deeper understanding of market dynamics, you can read our analysis of global chemical industry trends.

Potential Risks and Market Headwinds

No investment is without risk. Prudent investors conducting a thorough KAI stock analysis must consider several external and internal challenges that could impact profitability.

- •Manufacturing Profitability Squeeze: The global chemical market is facing oversupply issues and intense price competition, particularly from low-cost producers in China and the Middle East. This has already led to a year-over-year decline in average chemical segment prices and could continue to pressure margins.

- •Currency Exchange Volatility: As a Korean company with international dealings, KAI is exposed to fluctuations in the USD and JPY. The company estimates that a 10% change in foreign exchange rates could impact its bottom line by approximately KRW 1.9 billion.

- •Macroeconomic Uncertainty: A slowdown in the global economy or specific sectors like the IT industry could dampen demand for KAI’s high-purity solvents, affecting its growth ambitions. For context on economic indicators, see the latest reports from sources like The World Bank.

- •Input Cost Fluctuations: The prices of crude oil and other raw materials, along with global freight costs, are notoriously volatile and can directly impact KAI’s cost structure and profitability.

Investment Strategy: A Prudent ‘Hold’ Recommendation

Given the balance of strong fundamentals against significant market headwinds, the recommended investment strategy is a cautious “Wait and See (Hold)”. The upcoming IR is a critical event that will provide clarity on management’s strategy to navigate the identified risks.

Investors should meticulously scrutinize the details of the Q3 report and listen closely to the management’s commentary during the call. Pay specific attention to the profitability metrics within the chemical division, any forward-looking guidance on demand, and concrete plans for managing currency and raw material price risks. The progress and outlook for the high-purity organic solvent business will be a key indicator of the company’s future growth trajectory. A clear, convincing strategy from leadership could turn a ‘Hold’ into a ‘Buy’, while ambiguity or a downbeat forecast would warrant continued caution.