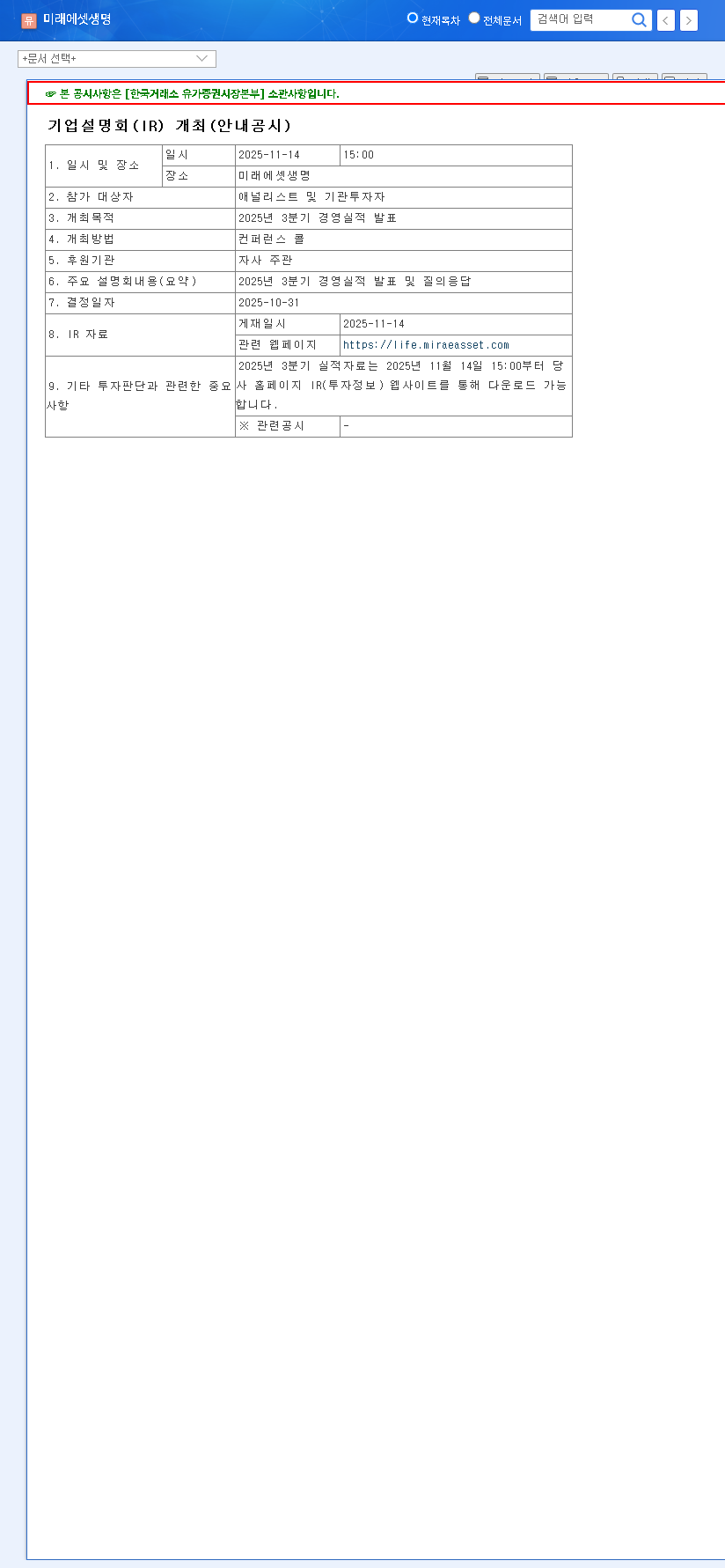

The upcoming Q3 2025 earnings call for MIRAE ASSET Life Insurance CO., Ltd. on November 14, 2025, is more than just a financial report; it’s a pivotal moment for investors evaluating the company’s trajectory amidst a volatile global economy. As one of South Korea’s premier life insurance providers, this investor relations (IR) event will offer critical insights into the company’s performance, strategic direction, and resilience. This comprehensive analysis will explore the key metrics, growth drivers, and potential risks that every investor should be watching.

We will delve into the core strengths of MIRAE ASSET Life Insurance, from its robust financial health to its forward-thinking business strategies, and provide a clear outlook on what the Q3 results could mean for the MIRAE ASSET stock.

Robust Fundamentals: The Bedrock of Stability

Understanding the K-ICS Ratio: A Pillar of Financial Health

A key indicator of an insurer’s stability is its capital adequacy. For MIRAE ASSET Life Insurance, the K-ICS (Korean Insurance Capital Standard) ratio is a critical metric. As of June 30, 2025, the company reported a K-ICS ratio of 192.4%. This figure is significantly above the 100% regulatory minimum, signaling a powerful capacity to absorb financial shocks and fulfill its obligations to policyholders. This high solvency level provides a strong foundation for investor confidence. The company’s commitment to transparency was further reinforced by a recent semi-annual report amendment to enhance the accuracy of this calculation, a move detailed in their Official Disclosure (DART).

Strategic Agility: The ‘Two-Track’ and ESG Focus

MIRAE ASSET Life Insurance employs a sophisticated ‘Two-Track’ strategy to balance growth with stability. By strategically combining protection-type insurance (providing stable, long-term revenue streams) with variable insurance products (offering growth potential linked to market performance), the company navigates different economic cycles effectively. This balanced approach is complemented by a strong commitment to future-oriented initiatives, including ESG (Environmental, Social, and Governance) management through the issuance of ESG bonds and a dedicated push towards digital transformation. These efforts are not just about corporate responsibility; they are designed to build long-term value and secure a competitive edge in a rapidly evolving market.

The Great Turnaround: Projecting Profitability and Growth

After navigating a challenging period, financial projections indicate a dramatic and promising turnaround for MIRAE ASSET Life Insurance. The company is poised to shift from losses to substantial profitability, marking a new chapter of growth.

Analysts project operating profit to surge from a loss of KRW -68.5 billion in 2023 to a robust profit of KRW 215.6 billion in 2024, with forecasts reaching an impressive KRW 333.9 billion in 2025. This signifies a powerful recovery and a positive outlook for future earnings.

This recovery extends across the board. Net profit is expected to follow a similar trajectory, turning positive in 2024 and climbing to KRW 333.1 billion in 2025. Consequently, Return on Equity (ROE) is projected to improve from -4.90% in 2023 to a healthy 5.84% in 2025. This strengthening profitability is supported by an improving balance sheet, with a decreasing debt-to-equity ratio and a rising current ratio pointing to enhanced financial stability and liquidity.

IR Outlook: Potential Impacts on MIRAE ASSET Stock

The Q3 2025 IR event will be a key determinant of near-term stock performance. Investors will be scrutinizing the results against market consensus and listening intently to management’s narrative. For more on market volatility, you can refer to analysis from authoritative sources like Reuters.

Bullish Signals to Watch For

- •Earnings Beat: If Q3 profits, particularly in operating and net income, surpass expectations, it could serve as a powerful catalyst for the stock price.

- •Confident Guidance: A clear and confident outlook from management on future growth, new product pipelines, and digital initiatives can significantly boost investor confidence.

- •Stable K-ICS Ratio: Reinforcement of the company’s high K-ICS ratio will underscore its defensive qualities in an uncertain macroeconomic environment.

Potential Bearish Risks

- •Earnings Miss: Any failure to meet consensus earnings could trigger a negative market reaction and a potential stock price decline.

- •Macroeconomic Concerns: If management expresses significant concern over interest rate or exchange rate volatility impacting investment returns, it may dampen investor sentiment.

- •Competitive Pressures: A lack of clarity on how MIRAE ASSET Life Insurance will differentiate itself in a fiercely competitive market could limit the IR’s positive impact.

Conclusion: An Action Plan for Investors

The evidence points towards a positive trajectory for MIRAE ASSET Life Insurance, built on strong fundamentals and a clear strategy for a profitable turnaround. This Q3 2025 IR is a crucial checkpoint. Investors should focus on the hard numbers—especially the growth in operating profit—and listen carefully to management’s qualitative explanations. Pay close attention to the Q&A session for insights into their strategies for navigating market risks. For those new to this sector, understanding the basics of insurance company valuation is a great next step. While the overall outlook is promising, prudent investors should remain cautious and prepared for short-term volatility following the announcement.