The recent CJ CheilJedang Q3 2025 earnings announcement sent a significant shockwave through the market, with preliminary figures falling substantially short of consensus expectations. This underperformance has understandably raised questions for current and potential investors about the company’s trajectory and financial health. Is this a temporary setback or a sign of deeper issues? This comprehensive analysis will dissect the Q3 results, evaluate the core strengths of CJ CheilJedang’s business segments against pressing macroeconomic challenges, and outline a clear CJ CheilJedang investment strategy for both short-term and long-term horizons.

Decoding the Q3 2025 Earnings Shock

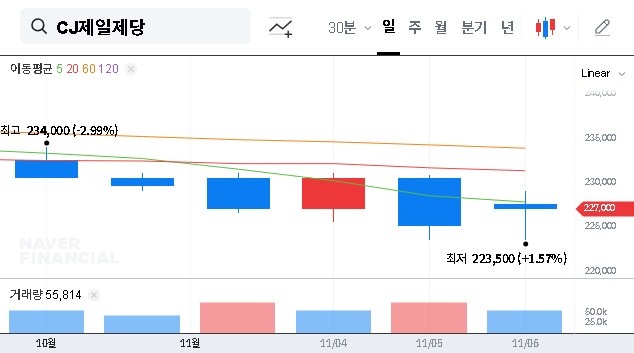

CJ CheilJedang reported its preliminary consolidated financial results for the third quarter of 2025, revealing a significant deviation from market forecasts. The numbers, as detailed in the Official Disclosure (DART), painted a challenging picture:

- •Revenue: KRW 7,439.5 billion, which was 2% below the market expectation of KRW 7,565.4 billion.

- •Operating Profit: KRW 346.5 billion, a more significant 7% miss compared to the forecast of KRW 372.6 billion.

- •Net Income: KRW 72.9 billion, a staggering 58% below the market expectation of KRW 173.8 billion.

While the revenue miss was modest, the sharp decline in operating profit and the collapse in net income are the primary drivers of investor concern. The significant gap in net income points towards non-operating factors, such as increased financial costs and adverse foreign exchange rate fluctuations, playing a major role in the quarter’s poor performance.

The Q3 results underscore the company’s vulnerability to external macroeconomic variables, temporarily overshadowing the fundamental strength of its diverse business portfolio. The key question for investors is how effectively management can navigate these headwinds moving forward.

Core Business Strength vs. External Pressures

A proper CJ CheilJedang stock analysis requires looking beyond a single quarter. Despite the recent slump, the company’s foundational business pillars remain robust.

A Diversified and Resilient Portfolio

- •Food Business: As a leader in the K-Food global expansion, anchored by domestic dominance and the growing Home Meal Replacement (HMR) trend, this segment has a strong consumer base. However, it faces persistent cost pressures from fluctuating international grain prices.

- •BIO Business: This division is a global powerhouse, leveraging world-class fermentation technology to lead in key amino acids. Future growth is pinned on the innovative White (bio-degradable plastics) and Red (specialty nutrients) BIO ventures. For more on this, see our deep dive into the BIO business segment.

- •Feed & Care (F&C): Focused on improving profitability through high-yield feed innovation and strategic expansion of its livestock operations.

The Weight of Macroeconomic Variables

The Q3 results clearly show that CJ CheilJedang is not immune to global economic shifts. Key variables that negatively impacted profitability include a volatile won/dollar exchange rate, rising interest rates that increase financial costs, and elevated international commodity prices. While the company employs risk management strategies, the scale of these external shocks proved overwhelming in this period. According to global market analysts, these pressures are expected to persist in the near term, making cost control and efficiency paramount.

A Practical CJ CheilJedang Investment Strategy

Given the disappointing CJ CheilJedang Q3 2025 earnings, investors must adapt their approach. A bifurcated strategy considering different time horizons is most prudent.

Short-Term Strategy: A Cautious ‘Wait-and-See’ Stance

In the immediate aftermath, market sentiment is likely to be negative. The stock may experience downward pressure as the market digests the full impact of the earnings miss. A tactical pause is recommended. Investors should wait for the company’s official conference call and detailed segment-by-segment analysis to understand the specific drivers of the slump and management’s concrete plans for remediation. Rushing into a position before these uncertainties are clarified carries unnecessary risk.

Mid-to-Long-Term Strategy: Focus on Enduring Growth Potential

The long-term growth thesis for CJ CheilJedang remains largely intact. The innovative potential of the BIO business, particularly in sustainable materials and high-value nutritional products, presents a significant upside that is not reflected in a single quarter’s results. For long-term investors, any significant price dip in the short term could present an attractive entry point. The key is to monitor for signs of stabilization, such as improved cost management, favorable shifts in raw material prices, and tangible progress in their new growth engines. Once these signals appear, re-entry can be considered for capturing the company’s enduring value.

In conclusion, while the Q3 earnings report is a clear negative, it should not derail the long-term investment case. Prudent investors should exercise short-term caution while keeping a close watch for a long-term buying opportunity once the dust settles. Continuous monitoring of macroeconomic trends and company-specific execution will be critical to navigating this period successfully.

Disclaimer: This analysis is based on preliminary data and is for informational purposes only. It is not intended as financial advice or an investment recommendation. All investment decisions should be made based on your own research and judgment.