A ₩157.6 Billion Bet: Inside the LS Cable & System Rights Offering

The recent announcement of the LS Cable & System rights offering, a massive capital injection totaling 157.6 billion KRW, represents a pivotal moment for its parent company, LS Corp. This strategic maneuver is not merely a financial transaction; it’s a clear signal of the company’s ambitious plans for future growth, technological advancement, and a reinforced commitment to LS Corp shareholder value. For investors, this move presents both opportunities and critical questions. How will these funds be utilized, and what does this capital increase signal about the broader LS Corp investment strategy? This comprehensive analysis will break down every facet of the offering, providing investors with the clarity needed to navigate this development.

Deconstructing the Rights Offering: The Core Details

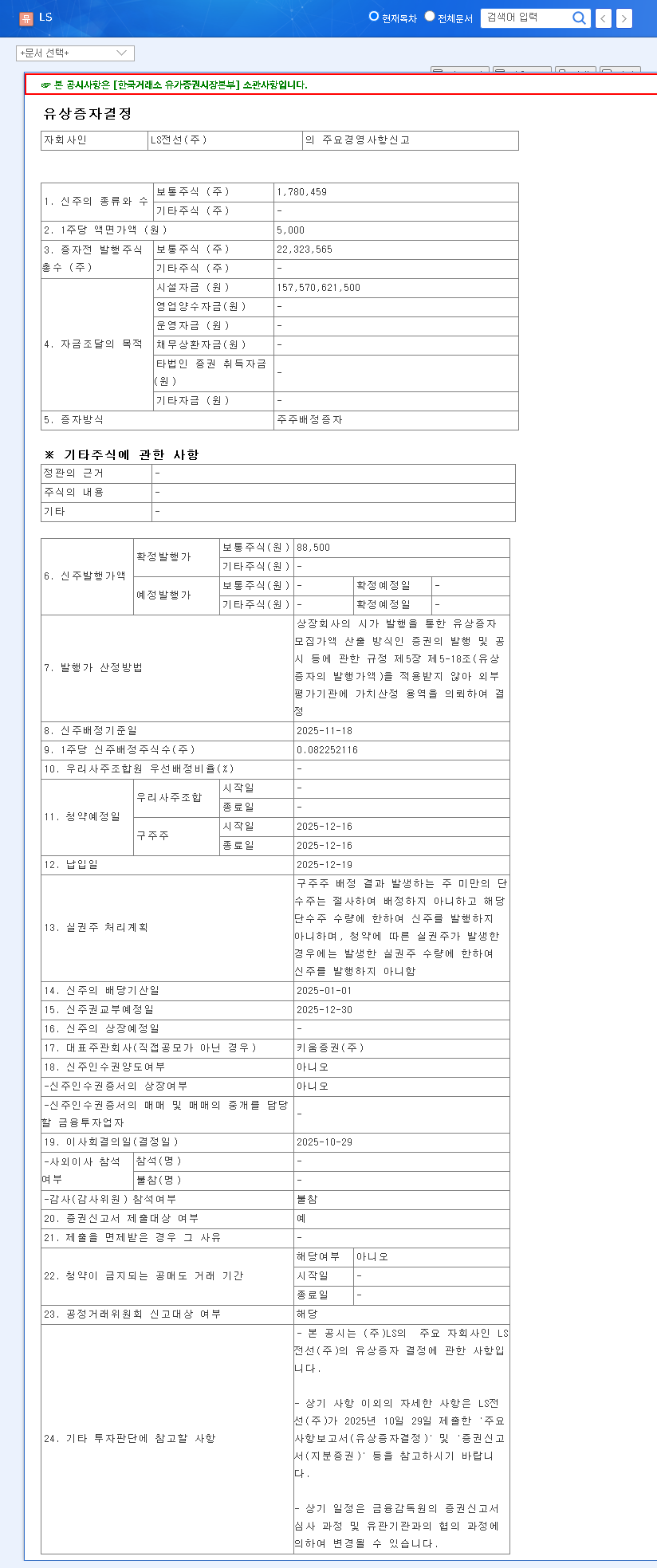

Announced on October 30, 2025, this shareholder rights offering grants existing shareholders the right to subscribe to new shares, directly funding the company’s expansion. Understanding these corporate actions is key for any investor; you can learn more about the fundamentals of corporate finance on our related resources page. Here are the essential details of the plan:

- •Total Amount: 157.6 billion KRW

- •Issuance Method: Shareholder Rights Offering

- •Offering Ratio: 0.08 new shares per existing share

- •Primary Purpose: Exclusively for facility investments

- •Subscription Period: December 16 – December 19, 2025

The Grand Strategy: Fueling LS Group Growth

This rights offering is a cornerstone of LS Corp.’s dual-pronged strategy: securing future growth engines while simultaneously enhancing shareholder value. It’s a calculated move to fortify the company’s market position and financial health for the long term, directly contributing to the overall LS Group growth trajectory.

A Clear Commitment to Shareholder Returns

LS Corp. has recently clarified its shareholder return policy, stating its intent to use financial resources for “dividend expansion” and other methods to boost LS Corp shareholder value. This offering should be viewed through that lens. By strengthening a key subsidiary, the parent company increases its capacity for future returns, creating a synergistic relationship between growth investment and shareholder rewards.

Fortifying Financials for Future Expansion

The influx of capital will significantly bolster LS Cable & System’s balance sheet. This financial fortification extends to the entire LS Group, enhancing its investment capacity and overall stability. The primary allocation of these funds is earmarked for critical facility investments, aimed at expanding production capacity and upgrading technology. This is confirmed by the company’s Official Disclosure (Source: DART), which outlines the use of proceeds. This strategic investment is designed to secure a competitive edge in a rapidly evolving global market.

This isn’t just about raising money; it’s about investing in dominance. The funds from the LS Cable & System rights offering are a direct injection into the company’s technological and production backbone, positioning it for long-term market leadership.

The Investor’s Playbook: Critical Monitoring Points

While the long-term outlook appears promising, savvy investors must remain vigilant. Success hinges on execution and market conditions. Here are the key factors to monitor as part of your LS Corp investment strategy:

- •Subscription Success & Market Sentiment: The subscription rate among existing shareholders will be the first major indicator of market confidence. A high rate signifies strong investor belief in the company’s vision.

- •Investment Execution & Transparency: Monitor company reports for specific details on how the ₩157.6B is being deployed. Is it on schedule? Are the projected efficiencies being realized? Transparency is paramount.

- •Macroeconomic Headwinds: The global economic climate is volatile. Keep an eye on interest rates, raw material costs (especially copper), and global shipping indices, as these directly impact profitability. Authoritative sources like Bloomberg’s market analysis can provide valuable context.

- •Competitive Landscape: The cable industry is fiercely competitive. Track the R&D, capital expenditures, and market share of key rivals to ensure LS Cable & System maintains its competitive advantage.

Conclusion: A Strategic Pivot for LS Group

The LS Cable & System rights offering is far more than a line item on a balance sheet. It is a strategic, forward-looking investment in the future of the entire LS Group. While short-term concerns about share dilution are valid, the long-term potential for increased corporate value, enhanced competitiveness, and greater shareholder returns is significant. For investors, the path forward requires diligent monitoring and a clear understanding of the company’s long-term vision. This move could very well be the catalyst that powers the next decade of LS Group growth.

Frequently Asked Questions (FAQ)

Why did LS Cable & System decide on a rights offering?

LS Cable & System plans to secure 157.6 billion KRW for facility investments through this rights offering. The primary purpose is to fund investments aimed at future growth, such as expanding production capacity and strengthening technological competitiveness.

What is the impact of this rights offering on LS Corp. as a whole?

As a major subsidiary, LS Cable & System’s enhanced financial health through these facility investments is expected to positively influence LS Group’s overall investment capacity, financial stability, and long-term growth potential.

What does the rights offering mean for existing LS Corp. shareholders?

While a rights offering can raise short-term dilution concerns, this action is aimed at long-term corporate value appreciation. If aligned with LS Group’s shareholder return initiatives, it enhances long-term LS Corp shareholder value. Existing shareholders receive the right to subscribe for new shares.

What should investors monitor regarding the LS Corp investment strategy?

Investors should comprehensively monitor the rights offering subscription rate, the specificity and execution of the facility investment plan, macroeconomic changes, and competitor trends to assess LS Group’s mid-to-long-term growth potential.