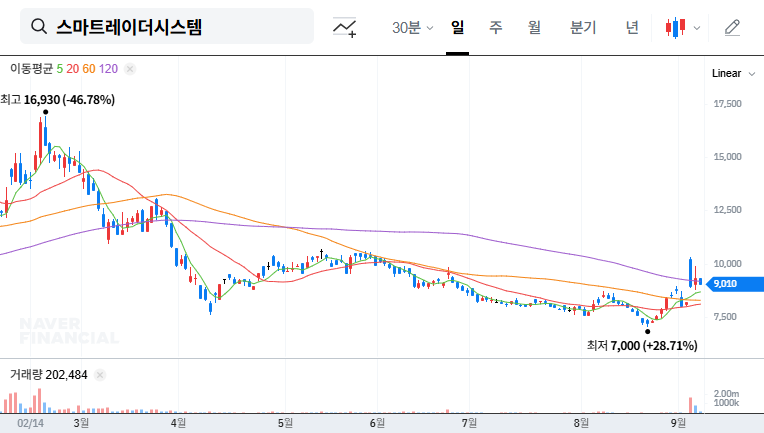

A significant Smart Radar System, Inc. shareholding change has been publicly disclosed, creating ripples within the investment community. This detailed report, officially titled ‘Report on the Status of Large Shareholding, etc. (General)’, outlines shifts in the stakes of major shareholders. Such changes can be a crucial indicator of a company’s internal dynamics, management stability, and future market confidence. For discerning investors, understanding the nuances behind this announcement is key to navigating potential impacts on Smart Radar System stock and its long-term corporate value.

This comprehensive investor analysis will dissect the disclosure, evaluate the company’s fundamentals based on H1 2025 performance, and consider the broader market and macroeconomic landscape. We will explore everything from its core 4D imaging radar technology to the implications for its KRW 122 billion market capitalization, providing deep insights for your next investment decision.

Decoding the Official Shareholding Report

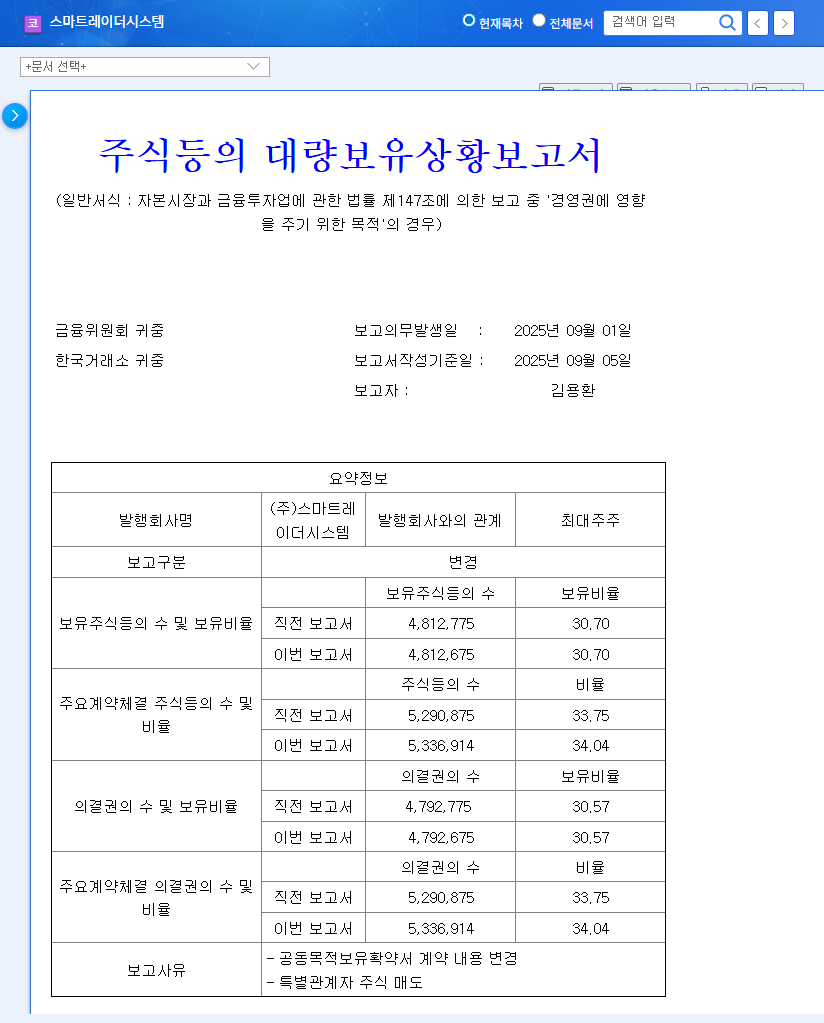

On November 12, 2025, Smart Radar System, Inc. filed a disclosure detailing changes in share ownership by CEO Yong-Hwan Kim and his specially related persons. The report, available via the official DART system, shows a marginal decrease in their collective holdings. You can view the full details in the Official Disclosure.

The key figures are a change from a 30.70% pre-report stake to a 29.99% post-report stake. While seemingly minor, any shift in a majority shareholder’s position warrants careful examination. The stated reasons for this fluctuation provide critical context:

- •Loan Agreement Adjustments: The agreement period for stock collateral loans involving the reporting parties was modified. This is often a standard financial maneuver and not necessarily a red flag.

- •Share Sale by Related Person: A specially related person, Jong-Il Kim, sold a total of 8,883 shares in the open market. This is the most direct cause for the decreased percentage.

- •Termination of Special Relationship: The formal ‘special relationship’ with certain executives was terminated following their resignation, removing them from the consolidated shareholding count.

Fundamental Health Check: H1 2025 Performance Review

To understand if the shareholding change is a symptom of deeper issues, we must analyze the company’s core financial health. Smart Radar System, Inc.’s performance in the first half of 2025 paints a picture of a company in transition, investing heavily in its future.

Key Financial Highlights

- •Revenue Stability: A minor year-over-year decrease of 1.18%, suggesting a stable top line.

- •Profitability Improvement: A significant jump in the gross profit margin from 17.86% to 25.90%, indicating better cost control and operational efficiency.

- •Narrowed Losses: Both operating and net losses were reduced, aided by efficient cost management and financial income gains.

- •Aggressive R&D: Research and development spending remains high at 47.54% of revenue. This is a powerful investment in future growth but puts pressure on short-term profitability. For more on this, you can read our Guide to Tech Company Valuations.

While securing future growth through its core 4D imaging radar technology, the primary challenges for Smart Radar System, Inc. remain achieving a full turnaround to profitability and strengthening its financial foundation.

Investor Impact of the Shareholding Change

How should investors interpret this news? It’s best to consider the short-term market noise versus the long-term fundamentals.

Short-Term Volatility

In the short term, any change in major shareholder stakes can increase stock volatility. The sale of shares by Jong-Il Kim, though small, could be perceived negatively by the market, potentially creating downward pressure. This is a common reaction that seasoned investors anticipate, as noted in market analysis by sources like Bloomberg. However, the other reasons for the change are procedural and do not signal a lack of confidence from the core leadership.

Medium to Long-Term Stability

From a long-term perspective, the situation appears stable. The collective stake held by CEO Yong-Hwan Kim and related parties remains a commanding 29.99%. Crucially, the filing’s purpose is explicitly stated as ‘management influence,’ indicating a continued commitment to controlling the company’s direction. Therefore, the immediate threat to management control is extremely low. The core focus for long-term value creation remains unchanged: leveraging the company’s powerful 4D imaging radar technology in the growing autonomous mobility market.

Investment Thesis: Neutral Outlook

Our overall investment opinion for Smart Radar System, Inc. is Neutral. The company’s technological edge and market position are undeniable positives. The improvements in gross profit margin are encouraging signs of maturing operations. However, the path to sustained profitability is a challenge that must be navigated, alongside managing financial burdens from borrowings and convertible bonds.

This Smart Radar System, Inc. shareholding change is more of a minor event than a structural shift. While it may cause temporary market fluctuations, it does not alter the company’s medium-to-long-term investment value, which is tied to its fundamental business performance and technological innovation.

Key Monitoring Points for Investors:

- •Future Shareholder Activity: Any further sales by specially related persons should be watched closely.

- •Profitability Metrics: Look for continued improvement in margins and a clear path to net profit in H2 2025 and 2026 reports.

- •Product Commercialization: Track news on new radar product launches and their market adoption rates.

- •Financial Management: Monitor how the company manages its debt and convertible bonds.