This comprehensive kt alpha Co., Ltd. earnings analysis offers a detailed look into the company’s preliminary financial results for the third quarter of 2025. For investors monitoring the 036030 stock, this report unpacks the key figures, explores the underlying growth drivers in its core markets, and outlines the potential risks and opportunities that lie ahead. We will delve into the numbers to provide clear, actionable insights for your investment strategy.

kt alpha Q3 2025 Earnings: The Official Numbers

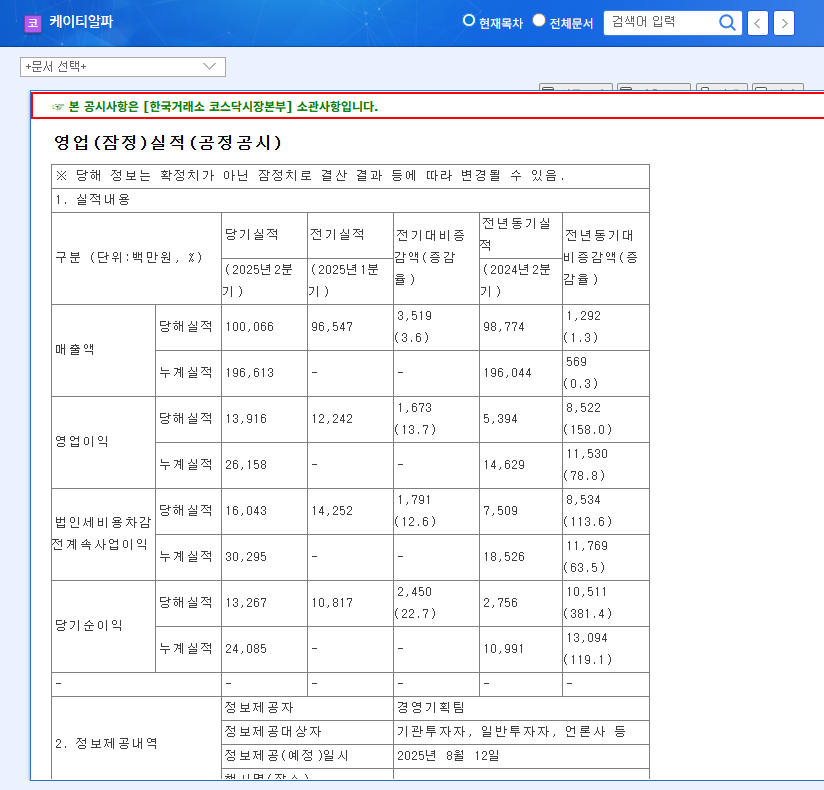

On November 12, 2025, kt alpha Co., Ltd. (036030) released its preliminary operating results for the third quarter. The report revealed a story of resilience and profitability, even amidst slight revenue fluctuations. These figures are based on the company’s filing, which can be reviewed in the Official Disclosure on DART.

Key Financial Highlights

- •Revenue: KRW 96.3 billion

- •Operating Profit: KRW 11.3 billion

- •Net Income: KRW 12.8 billion

While Q3 revenue experienced a minor decrease compared to the previous quarter, the true success story lies in profitability. Both operating profit and net income, despite a slight sequential dip, showcased a significant improvement year-on-year. This signals strong operational efficiency and a robust underlying business model, a key positive indicator for anyone conducting a kt alpha Co., Ltd. earnings analysis.

The year-on-year surge in operating profit and net income confirms that kt alpha’s strategic focus on core, high-margin businesses is yielding substantial returns for the company and its shareholders.

Core Business Strength: The Pillars of Growth

kt alpha’s impressive performance is built on two primary pillars: a mature T-commerce division and a rapidly expanding mobile gift certificate segment. The semi-annual report for 2025 already hinted at this stability, with H1 revenue hitting KRW 196.6 billion and operating profit at KRW 26.2 billion.

T-commerce Market: A Stable Foundation

The company’s T-commerce business continues to be a reliable revenue generator. By leveraging a large base of paid broadcasting subscribers, kt alpha maintains a defensible position in a competitive market. This segment provides the stable cash flow necessary to invest in higher-growth ventures. For more on the broader industry, see our analysis of the South Korean e-commerce market.

Mobile Gift Certificate Market: The High-Growth Engine

The mobile gift certificate market is where kt alpha is experiencing its most exciting growth. This segment is capitalizing on the massive consumer shift towards digital gifting and contactless payments. The sheer convenience and practicality of sending gifts via mobile have made it a dominant force in the consumer landscape, providing a powerful tailwind for the company’s expansion.

Financial Health and External Risk Factors

A Solid Balance Sheet

A key highlight for investors is kt alpha’s improving financial stability. As of the first half of 2025, the company’s debt-to-equity ratio had fallen to a healthy 58.9%. This reduction indicates prudent financial management and a lower risk profile, strengthening the investment case for the 036030 stock. This financial discipline is complemented by a clear business strategy: divesting non-core assets like the content business to double down on T-commerce and mobile certificates.

Navigating Macroeconomic Headwinds

No company operates in a vacuum. Investors must consider external risks:

- •Exchange Rate Volatility: With the continued depreciation of the Korean Won against the Euro and US Dollar, currency fluctuations could impact costs and profitability, a factor often discussed by outlets like Reuters.

- •Market Competition: The T-commerce and mobile gift certificate markets are increasingly crowded. Sustained growth will depend on kt alpha’s ability to innovate and maintain its market share against aggressive competitors.

- •Economic Uncertainty: A global or domestic economic slowdown could dampen consumer spending, which would directly affect both of kt alpha’s core business segments.

Investor Takeaway: What’s the Verdict on 036030 Stock?

The kt alpha Q3 2025 results paint a positive picture. The significant year-on-year improvement in profitability reaffirms the company’s strong fundamentals and successful strategic focus. Historically, the company’s stock price has reacted positively to strong earnings, and the increased trading volume earlier in the year suggests growing investor interest.

While external risks warrant careful monitoring, the combination of strong Q3 performance, a healthy balance sheet, and a strategic position in high-growth markets presents a compelling case. The current financial status is robust, and there is clear potential for stock price appreciation tied to continued earnings improvement.

In conclusion, this kt alpha Co., Ltd. earnings analysis suggests that the company is on a stable growth trajectory. Investors should continue to watch for execution on its growth strategies and monitor macroeconomic conditions, but the Q3 report provides a solid foundation for a positive outlook.