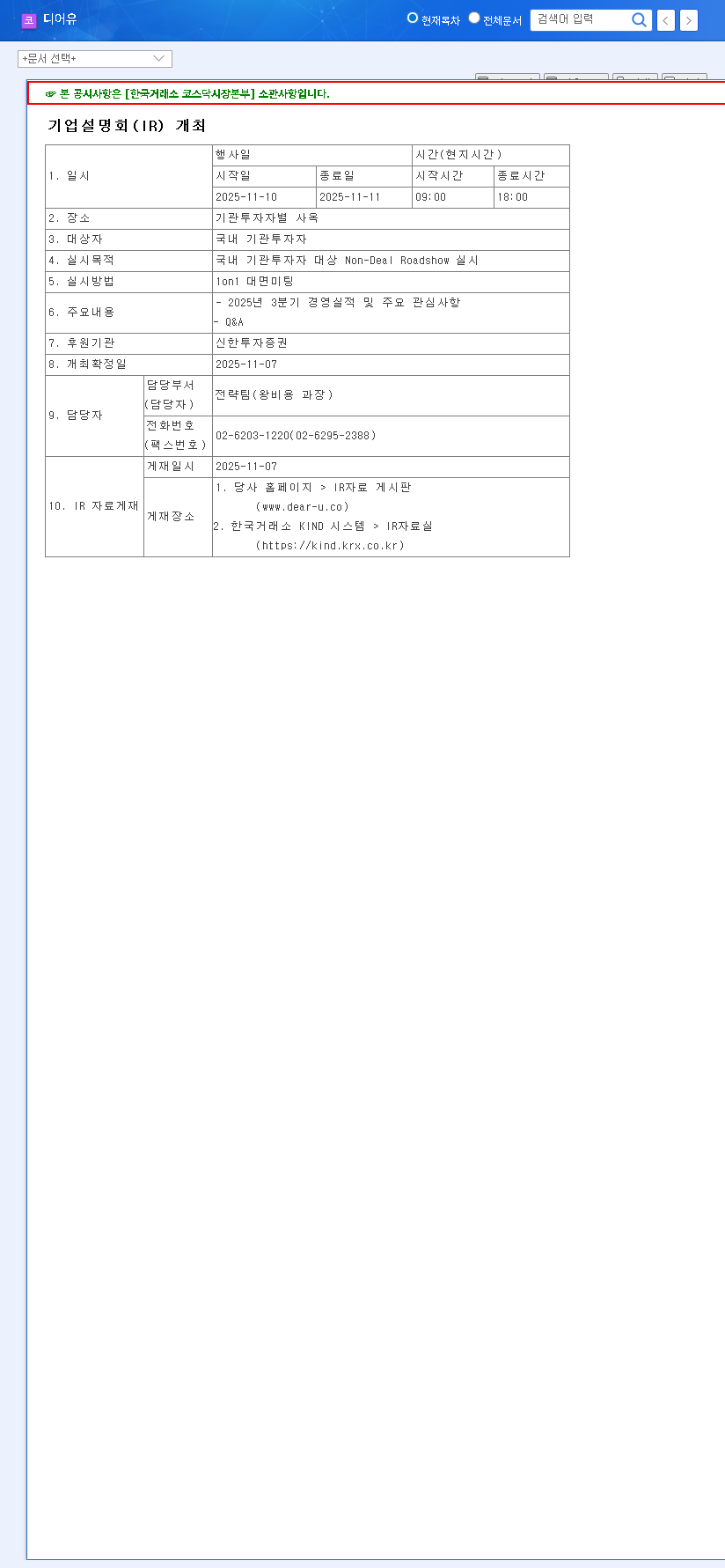

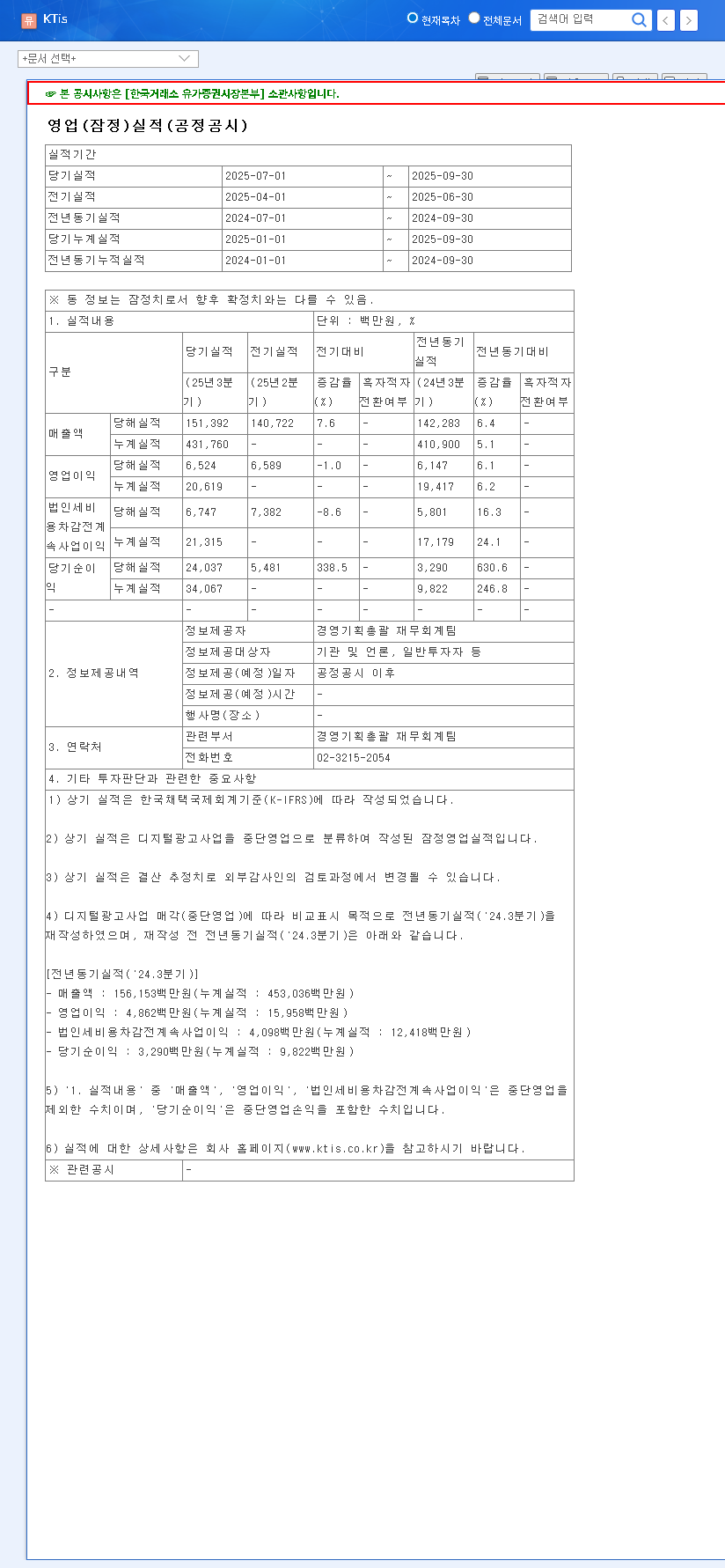

This comprehensive Messe eSang financial analysis delves into the company’s recently announced provisional Q3 2025 earnings. As Korea’s leading exhibition organizer, Messe eSang’s performance is often seen as a bellwether for the health of the events industry and broader consumer sentiment. Following a significant post-pandemic recovery, investors have been keenly watching to see if the company can maintain its impressive momentum. We will break down the numbers, evaluate the underlying fundamentals, and provide a clear investment perspective.

The exhibition sector is a dynamic space that thrives on economic activity. Messe eSang’s ability to not only recover but aggressively expand highlights its dominant market position and strategic foresight. This report offers the insights you need to understand the story behind the numbers.

Messe eSang Announces Impressive Q3 2025 Provisional Earnings

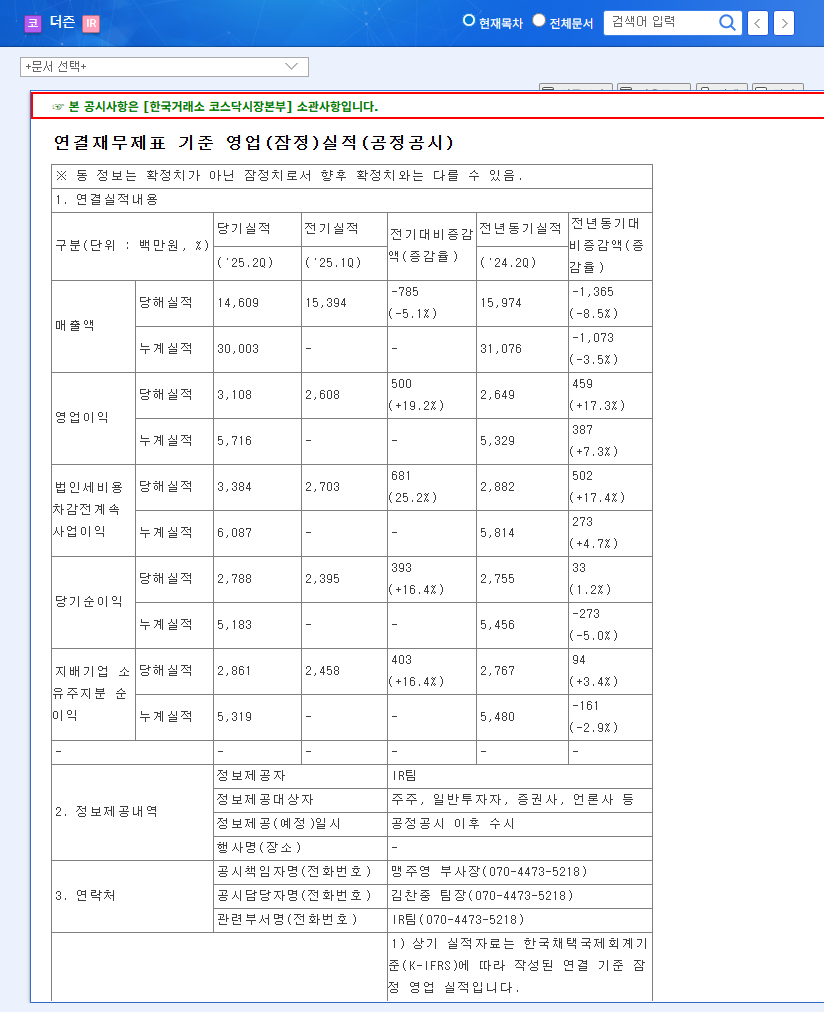

On November 10, 2025, Messe eSang Co., Ltd. released its provisional earnings for the third quarter of 2025, signaling another period of substantial year-over-year growth. The key figures reported are:

- •Revenue: KRW 21.9 billion

- •Operating Profit: KRW 6.3 billion

- •Net Profit: KRW 4.9 billion

These results provide a critical snapshot of the company’s operational success and financial health. For those seeking primary source verification, the company’s full report is available via the Official Disclosure on DART.

Why It Matters: Analyzing Messe eSang’s Robust Fundamentals

The appeal for those investing in Messe eSang goes far beyond a single quarter’s results. The company is built on a foundation of strong, sustainable fundamentals that promise long-term value.

Dominant Market Leadership

As Korea’s largest exhibition organizer, Messe eSang hosts over 90 events annually, cementing its leadership in the Korean exhibition industry. Flagship events like ‘Korea Build’, ‘MegaZoo’, and the ‘KOBE Baby Fair’ are not just exhibitions; they are industry-defining platforms that attract massive audiences and generate stable revenue streams.

Strategic Growth Initiatives

Messe eSang is actively pursuing future growth through two key avenues: digital transformation and global expansion. By investing in IT R&D, the company is enhancing the exhibitor and attendee experience with data analytics and digital platforms. Furthermore, its strategic entry into high-growth markets like India represents a significant step towards becoming a global player in the industry, a move detailed in our previous analysis of their expansion strategy.

Messe eSang’s consistent YoY growth is a testament to its strong business model and its leadership position within the rebounding global events market. The Q3 results reinforce a positive long-term outlook.

In-Depth Look: The Q3 2025 Earnings Data

To fully grasp the Messe eSang Q3 2025 earnings, we must compare them against previous periods to identify trends and anomalies. The following table provides a clear overview:

| Category | Q3 2025 (Prov.) | Q2 2025 | Q3 2024 |

|---|---|---|---|

| Revenue (KRW bn) | 21.9 | 17.4 | 13.8 |

| Operating Profit (KRW bn) | 6.3 | 6.5 | 3.2 |

| Net Profit (KRW bn) | 4.9 | 5.3 | 2.3 |

Year-over-Year (YoY) Analysis: Explosive Growth Continues

The YoY comparison is outstanding. Revenue surged by a massive 58.7%, while operating profit and net profit skyrocketed by 96.9% and 113.0%, respectively. This dominant growth trajectory confirms that the industry’s recovery is robust and that Messe eSang is effectively capturing increased demand and expanding its market share.

Quarter-over-Quarter (QoQ) Analysis: A Point of Consideration

While revenue grew a healthy 25.8% compared to Q2 2025, operating profit saw a slight dip of 3.1%. This suggests a potential short-term margin compression. The cause could be seasonal, related to the mix of exhibitions held in the quarter, or due to increased investment in marketing and technology for future events. While not a red flag, it is a key area for investors to monitor in the upcoming Q4 report.

Investor Action Plan & Final Outlook

Based on this detailed financial analysis, here is our overall assessment for current and potential investors.

Positive Factors

- •Sustained YoY Growth: The powerful year-over-year performance confirms the company’s growth thesis is intact.

- •Strong Financial Health: With a low debt-to-equity ratio and strong cash flow, the company is well-capitalized for future investments.

- •Strategic Vision: Clear focus on digital innovation and global expansion provides a roadmap for future revenue streams. For context on industry trends, see this analysis from a leading global consulting firm.

Points for Consideration

- •QoQ Profitability: The slight dip in quarterly profit margins requires monitoring to ensure it’s a temporary fluctuation and not a new trend.

- •Macroeconomic Risks: While resilient, the business is not immune to a potential global economic downturn, which could impact exhibitor budgets and attendance.

Investment Opinion: From a long-term perspective, Messe eSang remains a highly attractive investment. Its market leadership, sound financials, and clear growth strategy position it for continued success. While short-term volatility is possible, the core business is exceptionally strong. Investors with a long-term growth-oriented portfolio should find the Messe eSang stock a compelling opportunity.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. All investment decisions should be made at the investor’s own discretion and responsibility after conducting thorough research.