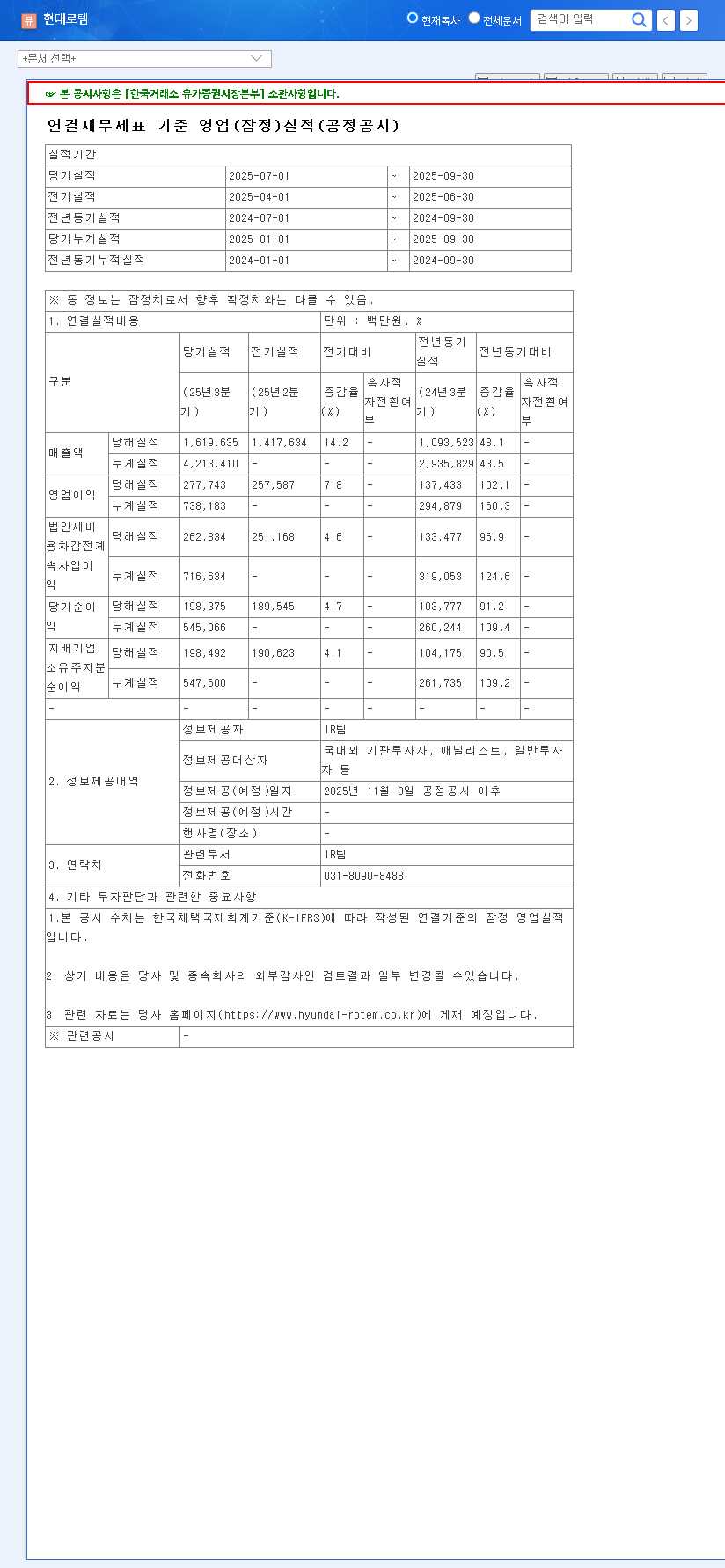

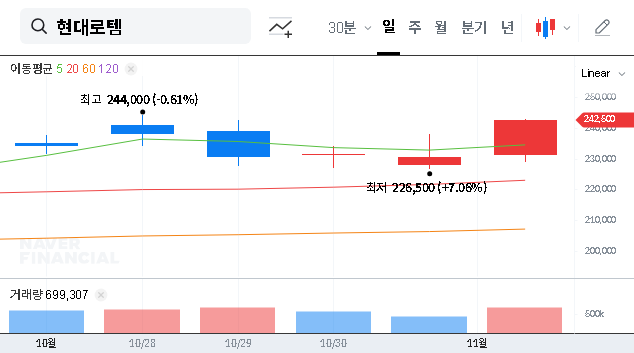

On November 11, 2025, Hyundai-Rotem Co. (ticker: 064350) will hold a pivotal Investor Relations session for domestic institutional investors. This Hyundai-Rotem IR is far more than a routine update; it’s a strategic platform to showcase the company’s Q3 2025 performance, validate its robust fundamentals, and outline its vision for future growth. For investors monitoring the Hyundai-Rotem stock, this event offers critical insights into its trajectory, from soaring overseas defense orders to pioneering eco-friendly rail solutions. This analysis will delve into the key discussion points and their potential market impact.

Core Business Segments: Analyzing the Growth Drivers

Hyundai-Rotem’s diversified portfolio is its greatest strength. The upcoming IR will provide color on the performance and outlook for its three primary divisions, which are the core Hyundai-Rotem growth drivers.

1. Defense Solution (55% Revenue Share)

The Defense Solution segment remains the company’s primary revenue engine, fueled by strong international demand. The export success of the K2 main battle tank, particularly to Poland, has solidified Hyundai-Rotem’s position as a global defense powerhouse. Ongoing geopolitical tensions in Eastern Europe and other regions continue to drive defense budget increases, creating a sustained demand pipeline. Investors at the Hyundai-Rotem IR will be keen to hear about progress on subsequent K2 export batches and expansion plans for its wheeled armored vehicle projects, which offer diversification within the land systems market.

2. Rail Solution (36% Revenue Share)

The Rail Solution division is capitalizing on the global shift towards sustainable transportation. Steady performance is anchored by domestic projects like the Great Train eXpress (GTX), but the real excitement lies in future-facing technologies. The commercialization of hydrogen-powered electric trams represents a significant leap into next-generation mobility. As governments worldwide commit to reducing carbon emissions, the demand for green public transit solutions is expected to surge, positioning this segment for significant long-term growth. We expect the Hyundai-Rotem Q3 performance report to detail new order prospects in this high-potential area.

3. Eco-Plant (9% Revenue Share)

Though the smallest segment, Eco-Plant holds immense potential. This division focuses on crucial future industries, including hydrogen infrastructure (production, storage, charging stations) and smart logistics automation. As the hydrogen economy develops, a trend supported by organizations like the International Energy Agency (IEA), Hyundai-Rotem’s early investments could yield substantial returns. The IR should provide updates on tangible project milestones and the strategy for scaling these nascent but critical operations.

Investors should focus on the synergy between the Rail Solution and Eco-Plant divisions. Success in hydrogen trams is directly linked to the development of a robust hydrogen infrastructure, creating a powerful internal growth loop.

Financial Stability and Strategic Outlook

A strong balance sheet underpins Hyundai-Rotem’s ambitious growth plans. The company has demonstrated impressive financial discipline, significantly improving its debt-to-equity ratio to 134% from 163% at the end of the previous year. This deleveraging enhances financial stability and provides greater flexibility for future investments. Furthermore, a robust operating cash flow and a stable A+ credit rating signal strong operational health and facilitate favorable access to capital. For a deeper look at industry financials, you can explore our comprehensive industrial sector analysis.

The company is also investing heavily in its future. The 109.9 billion KRW commitment to R&D for technologies like wearable robotics and advanced hydrogen systems is a clear indicator of its long-term vision. These investments are crucial for maintaining a competitive edge and unlocking new markets.

Key Questions for the Hyundai-Rotem IR

As the event unfolds, investors should seek answers to several critical questions that will influence the Hyundai-Rotem stock valuation:

- •Order Pipeline: Beyond the current Polish contract, what is the status of other K2 tank and armored vehicle export negotiations?

- •Profitability Margins: How are fluctuating raw material costs and exchange rates impacting margins, and what hedging strategies are in place?

- •Hydrogen Roadmap: What is the concrete commercialization timeline for hydrogen trams and the expected ramp-up in the Eco-Plant’s infrastructure business?

- •Capital Allocation: How does the company plan to allocate capital between R&D, shareholder returns, and further debt reduction?

The answers provided during the Hyundai-Rotem IR will be critical. Positive surprises in Q3 earnings, the announcement of a major new order, or a clear, confident roadmap for new technologies could serve as powerful catalysts for the stock. Conversely, any guidance that falls short of expectations or highlights significant macroeconomic headwinds could lead to downward pressure.

For complete transparency and to review the primary data, investors should consult the company’s official filing with the Financial Supervisory Service. Official Disclosure: Click to view DART report.