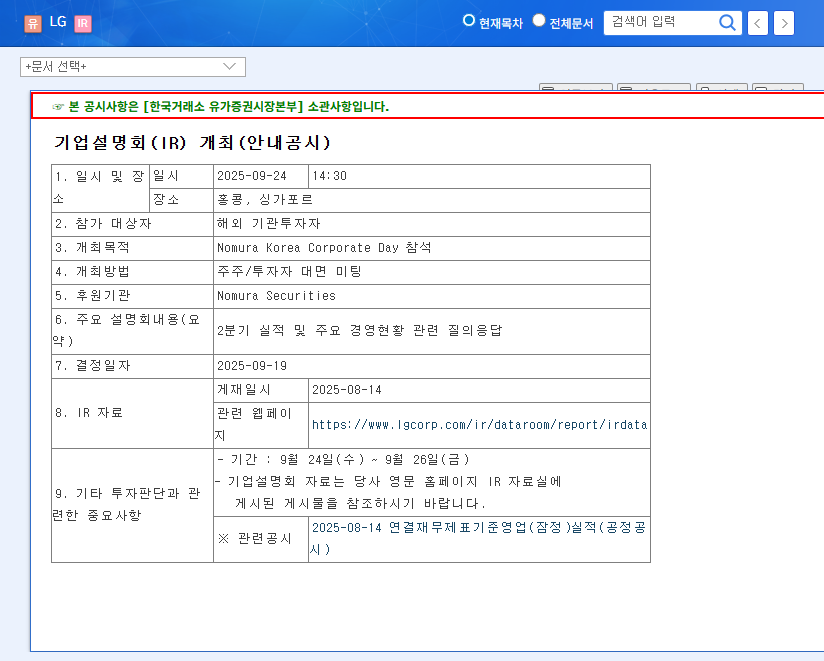

1. LG Investor Relations (IR) Overview

LG will hold its investor relations (IR) meeting on September 24th as part of Nomura Korea Corporate Day. The meeting will cover the company’s Q2 2025 earnings and key management updates, providing a crucial platform for communication with investors and showcasing growth strategies.

2. Fundamentals and Market Environment Analysis

2.1. Company Fundamentals

LG reported consolidated revenue of KRW 3.73 trillion (an 8.3% YoY increase) in the first half of 2025, driven by strong performance in LG CNS’s IT services and increased equity method gains. However, standalone operating revenue decreased by 13.5% to KRW 523.1 billion, primarily due to a decline in dividend income. The company repurchased shares in April, demonstrating its commitment to enhancing shareholder value. Key subsidiary updates include:

- LG CNS: Expanding cloud and AI investments

- LG Uplus: Focusing on IDC and EV charging infrastructure

- LG Chem: Prioritizing new drug development and battery materials

- LG Electronics: Investing in robotics for future growth

2.2. Market Environment

US interest rates remain stable, with the European Central Bank’s base rate at 2.15%. Oil prices are volatile, while the KRW/USD exchange rate shows an upward trend. Rising gold prices reflect a preference for safe-haven assets. The IT services market is expected to grow with cloud and AI adoption, positioning LG CNS for continued success. The consumer electronics and battery sectors face intensifying competition, and LG Chem is mitigating risks through portfolio diversification.

3. Key IR Takeaways and Investment Strategies

The IR meeting is expected to provide detailed insights into LG’s Q2 2025 performance and key business initiatives. Addressing the decline in standalone operating revenue and outlining future growth strategies will be crucial. A positive announcement meeting market expectations could boost investor sentiment and drive stock prices higher. Conversely, failure to meet these expectations could negatively impact stock performance. Careful analysis of the IR presentation and management Q&A is essential for informed investment decisions.

FAQ

When is the LG Investor Relations (IR) meeting?

The IR meeting is scheduled for September 24, 2025, at 2:30 PM KST.

What are the key topics to be discussed at the IR?

The meeting will cover Q2 2025 earnings results and key management updates. Analysts and investors will be particularly interested in the company’s plans to address the decline in standalone operating revenue and its future growth drivers.

How can I participate in the IR meeting?

The IR meeting is part of Nomura Korea Corporate Day, which may limit direct participation for individual investors. Information related to the IR can be found on LG’s official website or through brokerage firms.