The latest DN AUTOMOTIVE CORPORATION earnings report for Q3 2025 presents a complex picture for investors. The company (007340), a significant player with a diverse portfolio in automotive parts and machine tools, has revealed preliminary figures showing healthy revenue growth juxtaposed with a concerning dip in operating profit. This mixed signal has left the market pondering its next move.

How should investors interpret these numbers? Is the revenue growth a sign of fundamental strength, or does the profitability decline foreshadow deeper issues? This comprehensive analysis will break down the DN AUTOMOTIVE stock outlook, examining corporate fundamentals, macroeconomic headwinds, and providing a clear investment strategy to help you make informed decisions.

DN AUTOMOTIVE’s Q3 2025 Preliminary Earnings at a Glance

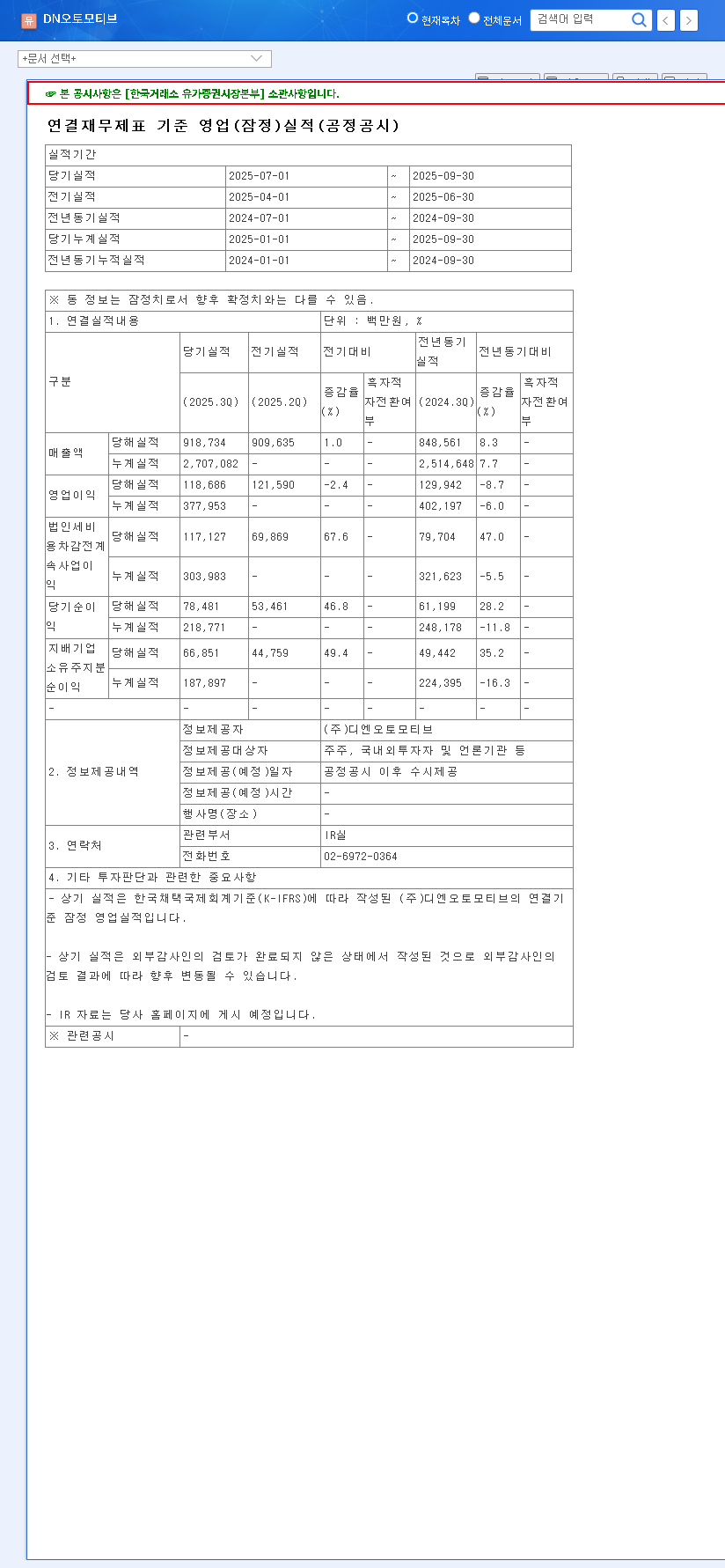

On November 5, 2025, DN AUTOMOTIVE CORPORATION released its preliminary consolidated financial results, which can be verified in the company’s Official Disclosure. The key performance indicators paint a nuanced story:

- •Revenue: KRW 918.7 billion. This figure represents a slight but steady year-over-year increase, signaling sustained demand and market presence.

- •Operating Profit: KRW 118.7 billion. The most notable point of concern, this marks a slight decrease quarter-over-quarter, raising questions about margin compression.

- •Net Profit: KRW 66.9 billion. A modest rebound from the previous quarter, but its sustainability is yet to be confirmed.

While top-line growth is a positive sign of the company’s operational resilience, the decline in operating profit suggests that rising costs or pricing pressures are beginning to eat into profitability.

The core challenge for DN AUTOMOTIVE is clear: converting strong sales into stronger profits. The divergence between revenue and operating profit is the central theme of this quarter’s results.

Analysis: The Forces Shaping Performance

To understand the DN AUTOMOTIVE CORPORATION earnings, we must look beyond the headline numbers and analyze the interplay between internal strategies and external market forces.

Internal Strategy and Business Structure

DN AUTOMOTIVE’s strength lies in its diversified business, spanning automotive parts, machine tools, and its emerging battery business. The recent merger with Dong-A Tire & Rubber and the shift to a holding company structure are strategic moves designed to unlock synergies and improve efficiency. However, this diversification also exposes the company to varied segment-specific challenges.

- •Revenue Drivers: Continued investment in new factory expansions and cross-segment sales likely bolstered the top line.

- •Profitability Headwinds: The profit dip could stem from rising raw material costs, increased logistics expenses, or intensified competition in the machine tool market forcing price concessions. For a deeper understanding of how such factors are reported, investors can review guides on reading corporate financial statements.

The Macroeconomic Gauntlet

No company operates in a vacuum. Broader economic trends, as reported by outlets like Reuters, are exerting significant pressure:

- •Currency Volatility: A strong USD relative to the KRW increases the cost of imported raw materials and components, directly impacting profit margins.

- •High Interest Rates: Elevated benchmark rates in both Korea and the U.S. increase the cost of capital, making debt servicing more expensive, a notable risk given the company’s high debt-to-asset ratio.

- •Raw Material Costs: While a decline in oil prices provides some relief on transportation costs, the price volatility of specialized materials like rubber remains a key variable.

Investment Strategy for DN AUTOMOTIVE Stock

Given this complex environment, a carefully considered investment strategy for DN AUTOMOTIVE is crucial. We recommend a bifurcated approach based on investment horizon.

Short-Term Outlook: Caution and Patience

In the immediate term, the market is likely to focus on the negative signal of declining operating profit. This could create downward pressure on the DN AUTOMOTIVE stock price until the company provides clarity. A prudent short-term strategy is a “wait-and-see” approach. Investors should wait for the final, confirmed earnings report and pay close attention to management’s commentary on margin improvement plans.

Mid- to Long-Term Potential: A Balancing Act

The long-term picture is more balanced, with clear growth drivers and significant risks.

- •The Bull Case: Growth can be fueled by synergies from the Dong-A merger, the ramp-up of new production facilities, and the company’s diversified revenue streams. Proactive shareholder-friendly policies like dividends and stock buybacks also build investor confidence.

- •The Bear Case: The high debt-to-asset ratio remains a significant vulnerability, especially in a high-interest-rate environment. Continued margin erosion and macroeconomic volatility are the primary risks to monitor.

Frequently Asked Questions (FAQ)

What were DN AUTOMOTIVE’s key Q3 2025 results?

The company reported preliminary revenue of KRW 918.7 billion (an increase), operating profit of KRW 118.7 billion (a decrease), and net profit of KRW 66.9 billion (a slight rebound).

Why did operating profit fall if revenue grew?

The decline is likely due to a combination of factors, including rising costs for raw materials and logistics, pricing pressures from competitors, or temporary underperformance in one of its key business segments. The final report will provide more specific details.

What is the recommended investment approach for 007340 now?

A conservative, patient approach is advised. Investors should wait for the confirmed earnings release and management’s strategic plans for improving profitability before making significant investment decisions. Continuous monitoring of the company’s debt levels and macroeconomic conditions is essential.

Disclaimer: This analysis is based on publicly available preliminary information and is intended for informational purposes only. It does not constitute investment advice. All investment decisions are the sole responsibility of the investor.