The latest review of MIRAE ASSET Life Insurance financial performance for Q3 2025 reveals a fascinating and complex picture for investors. On one hand, the company has demonstrated remarkable strength in its financial stability, boasting an impressive solvency ratio. On the other, its provisional operating performance shows a concerning dip in profitability. This duality presents a critical question: is MIRAE ASSET Life Insurance a stable ship navigating rough waters, or are there underlying currents that investors should be wary of? This deep-dive analysis will dissect these contrasting signals, explore the external market forces at play, and provide a comprehensive outlook on the company’s future.

While short-term profitability has faced headwinds, MIRAE ASSET Life Insurance’s fortified solvency ratio provides a powerful buffer against market volatility, signaling robust long-term risk management.

The Pillar of Strength: A Soaring Solvency Ratio

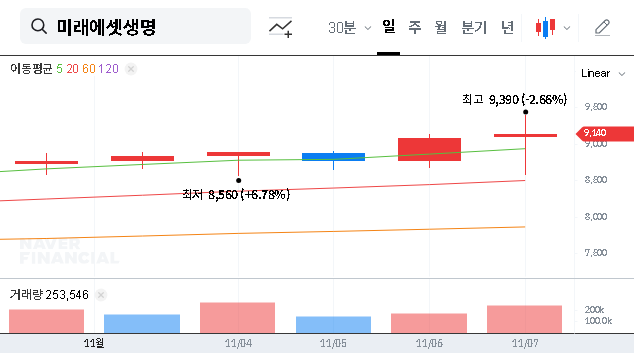

One of the most positive takeaways from the recent data is the significant improvement in MIRAE ASSET’s financial health. As of the end of June 2025, the company’s solvency ratio, measured by the stringent K-ICS (Korean Insurance Capital Standard), climbed from 183.5% to an impressive 192.4%. This isn’t just a number; it’s a critical indicator of an insurer’s ability to meet all its long-term obligations to policyholders. The increase was driven by a dual achievement: the total solvency amount grew while the required capital actually decreased, showcasing highly efficient capital and risk management. You can view the official numbers in the Official Disclosure.

Why the K-ICS Ratio Matters More Than Ever

The introduction of K-ICS has been a game-changer for the Korean insurance industry, demanding a more rigorous, market-value-based assessment of assets and liabilities. For MIRAE ASSET Life Insurance to not only adapt but to thrive under this new standard speaks volumes about its strategic foresight. For more information on how these standards work, you can review guidelines from a regulatory body like the Financial Supervisory Service.

- •Enhanced Policyholder Trust: A high solvency ratio directly translates to a greater capacity to pay claims, even in adverse economic scenarios, building confidence among customers.

- •Regulatory Compliance: It demonstrates proactive alignment with a tightened regulatory environment, reducing the risk of regulatory intervention.

- •Competitive Advantage: In a mature market, superior financial stability is a key differentiator that can attract more discerning customers and business partners.

The Other Side of the Coin: Analyzing the Dip in Operating Performance

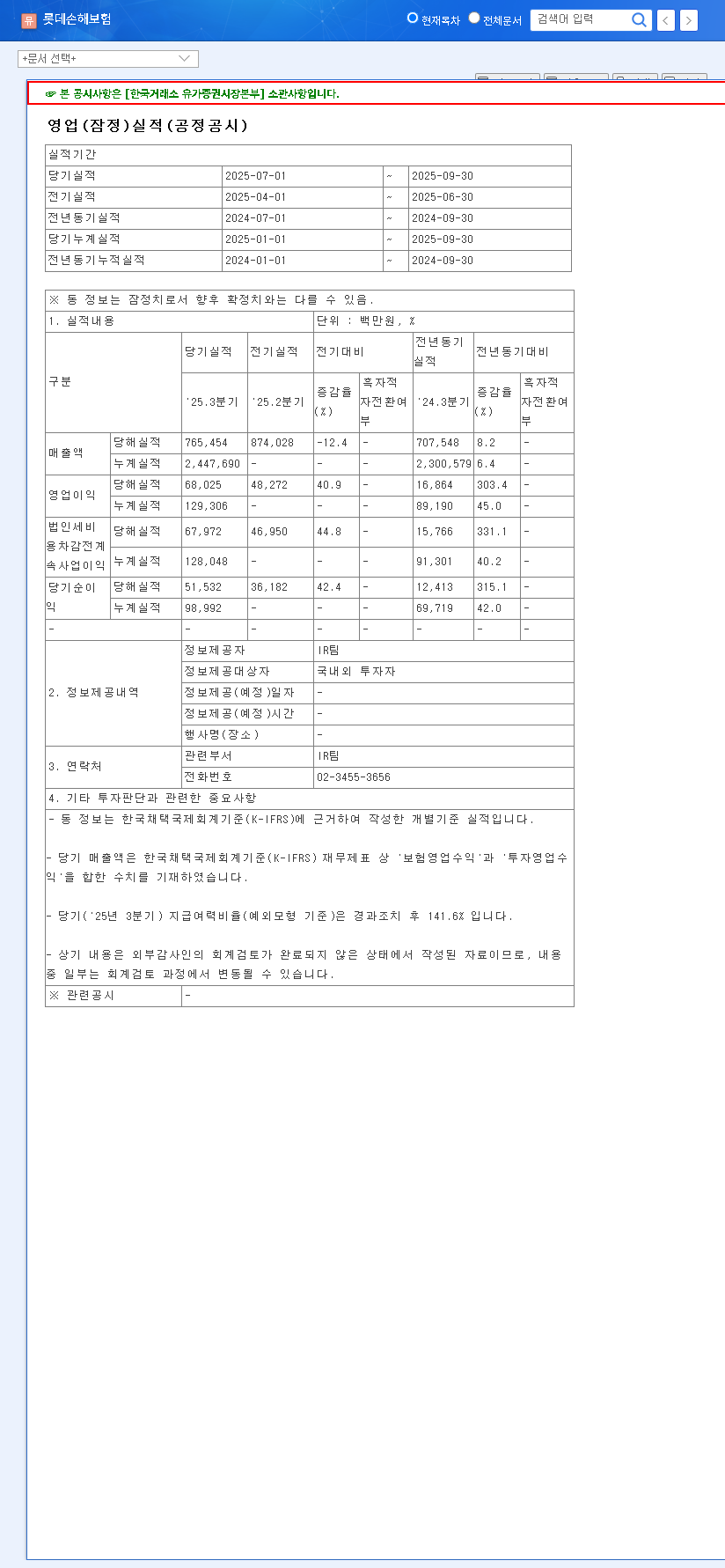

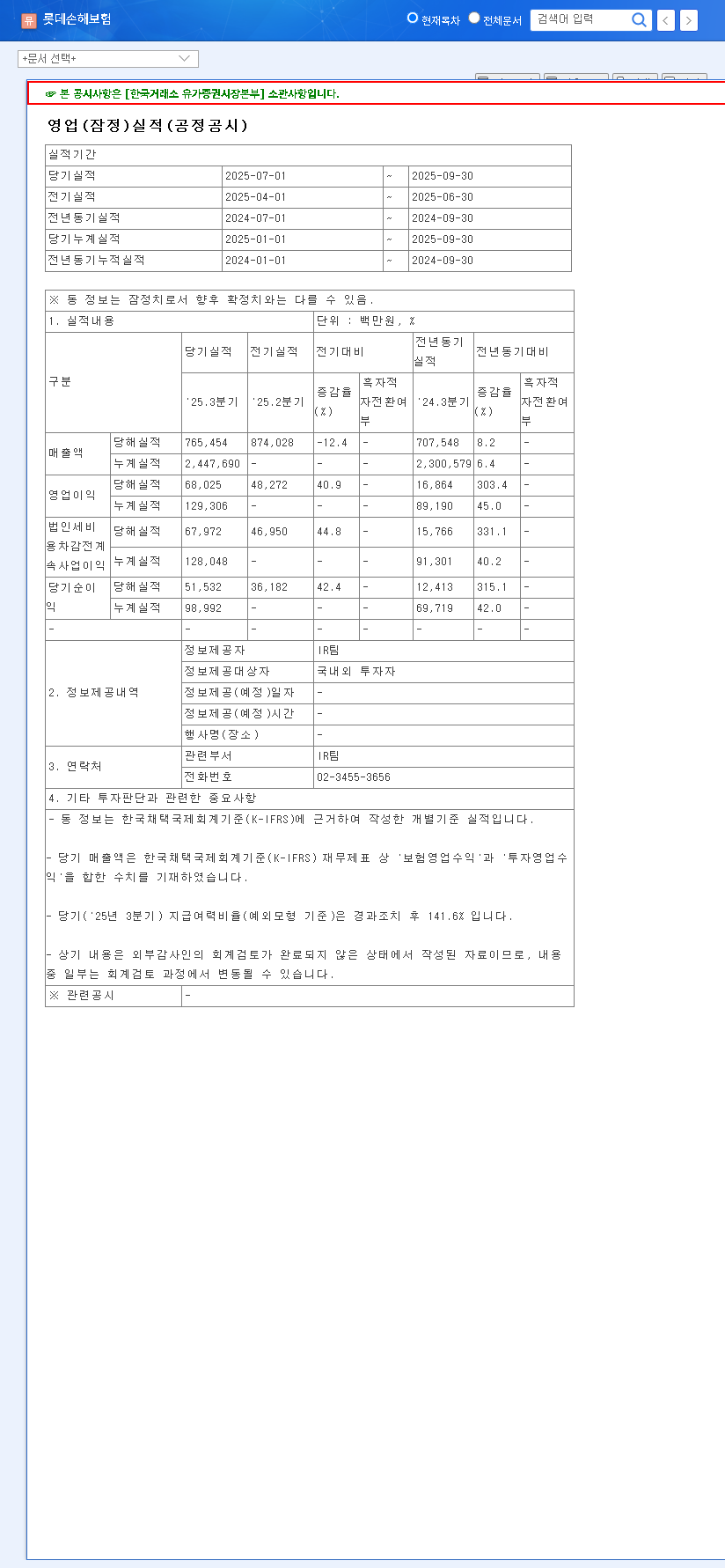

While the solvency figures are reassuring, the provisional operating results for Q3 2025 paint a less rosy picture. The company reported a decline in key profitability metrics, with revenue at KRW 1.254 trillion, operating profit at KRW 61.8 billion, and net profit at KRW 49.8 billion—all showing a decrease from the previous quarter. This downturn isn’t unique to MIRAE ASSET but reflects a complex mix of industry-wide challenges and short-term market turbulence.

Key Factors Behind the Profitability Squeeze

- •Macroeconomic Pressures: Volatility in global financial markets, including fluctuations in interest rates and the USD/KRW exchange rate, directly impacts investment returns, which are a core part of an insurer’s income.

- •Industry Saturation: The Korean insurance market is mature, leading to intensified competition and pressure on profit margins as companies vie for a limited pool of new customers.

- •Shifting Business Mix: While the strategic focus on protection-type insurance and fee-based business (Fee-Biz) is sound for long-term stability, it may lead to different revenue recognition patterns compared to traditional savings-type products. For those interested, our guide on analyzing insurance company financials provides more context.

Strategic Outlook and Investor Takeaways

In summary, the MIRAE ASSET Life Insurance financial performance presents a classic case of stability versus short-term profitability. The robust solvency ratio is a testament to the company’s strong risk management foundation. However, the dip in operating profit highlights the urgent need for strategic adaptation in a challenging environment.

What should investors monitor moving forward?

1. Profitability Improvement Initiatives: Watch for clear strategies aimed at boosting profitability. This includes the successful expansion of their Fee-Biz model, innovations in digital customer engagement, and the development of new, high-margin revenue streams. The company’s ability to execute these plans will be key to its future valuation.

2. Macroeconomic Response: Pay close attention to how the company’s investment portfolio performs amidst changing interest rate and currency environments. A proactive and flexible asset management strategy will be crucial to navigating this volatility and protecting investment gains.

3. Sustained Financial Soundness: While the solvency ratio is currently strong, it’s important to ensure this trend continues. Continued stability provides the foundation from which the company can pursue growth without taking on excessive risk.

Ultimately, MIRAE ASSET Life Insurance has a solid base of financial health but faces the undeniable challenge of improving its operating performance. For long-term investors, the focus should be on the company’s strategic responses to these market pressures and its ability to turn its foundational stability into sustainable growth.

![(000370) Hanwha General Insurance: K-ICS Stability Analysis & Carrot Subsidiary Risk [2025 Investor Deep Dive]](https://note12345-images.s3.ap-southeast-2.amazonaws.com/wp-content/uploads/2025/11/12202007/000370.png)

![(000370) Hanwha General Insurance: K-ICS Stability Analysis & Carrot Subsidiary Risk [2025 Investor Deep Dive] 관련 이미지](http://note12345-images.s3.ap-southeast-2.amazonaws.com/wp-content/uploads/2025/11/12202010/000370_%EA%B3%B5%EC%8B%9C.png)