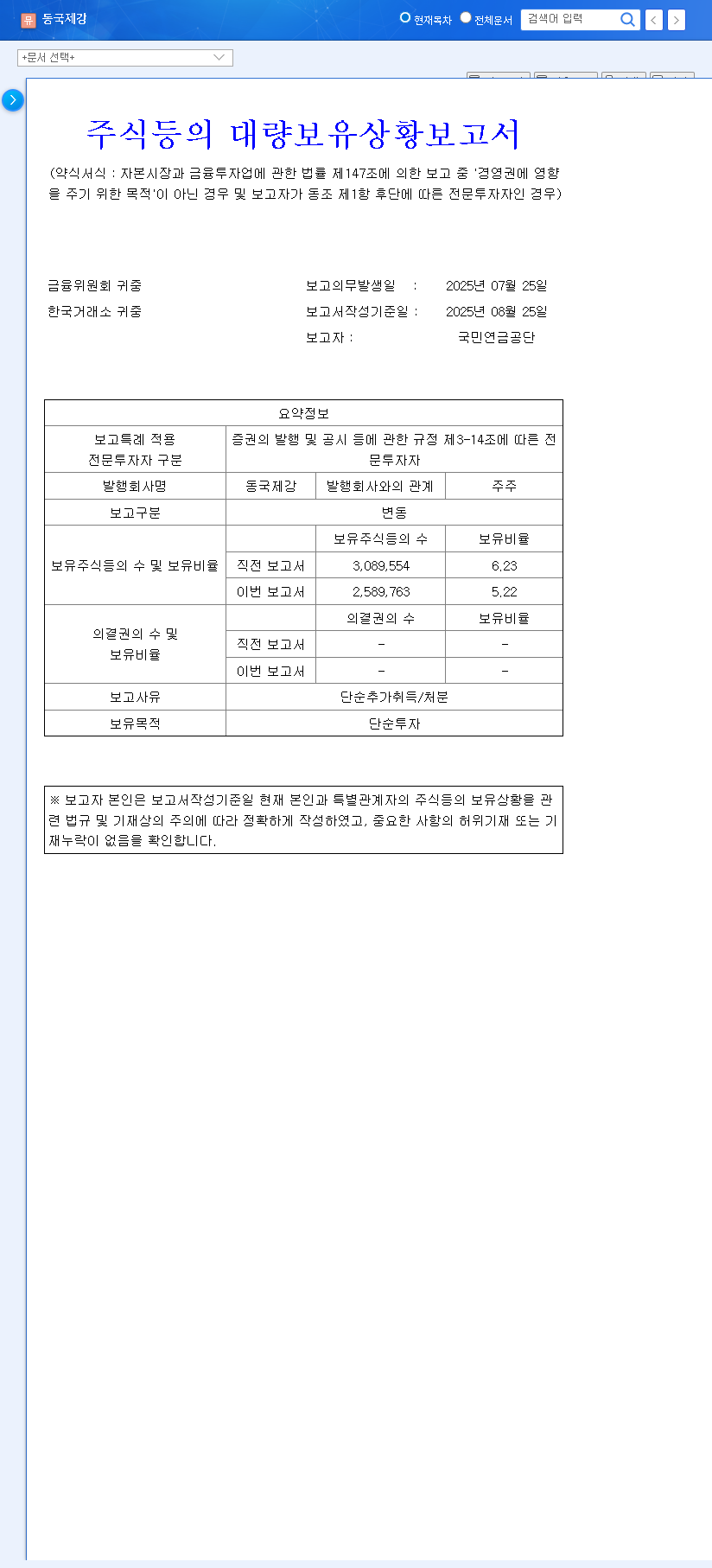

The recent disclosure from South Korea’s National Pension Service (NPS) announcing a reduction in its ownership of Dongkuk Steel stock has sent ripples through the investment community. When one of the country’s largest institutional investors adjusts its position, the market takes notice. The NPS reduced its stake from 6.23% to 5.22%, a move that raises critical questions for current and potential investors.

What does this stake reduction truly signify for the future of Dongkuk Steel? Is this a signal of underlying weakness, or merely a portfolio rebalancing? This in-depth analysis will explore the full implications of this event on the Dongkuk Steel stock price, its core fundamentals, and provide actionable strategies for your investment decisions.

The Disclosure: What Exactly Happened?

On October 1, 2025, the National Pension Service (NPS) filed an official ‘Report on Major Shareholdings’ concerning Dongkuk Steel (Market Cap: KRW 450.9 billion). The report, available on the public DART system (Official Disclosure), confirmed the key detail: the NPS’s stake in Dongkuk Steel decreased from 6.23% to 5.22%. This 1.01 percentage point reduction was categorized as a result of a ‘simple additional acquisition/disposal’, but the reasons behind such a move warrant a closer look.

A Deep Dive into Dongkuk Steel Stock Fundamentals

To understand the NPS’s decision, we must analyze the fundamental health of Dongkuk Steel. The company faces a mix of significant headwinds and promising strategic initiatives.

1. Challenging Market and Underperforming Earnings

The first half of 2025 was tough for Dongkuk Steel, primarily due to a broad downturn in the global steel market and a slowdown in the domestic construction sector. Financial results reflected this pressure:

- •Revenue: KRW 1.6192 trillion, showing a notable decline year-over-year.

- •Operating Profit: KRW 34.2 billion, also significantly lower than the same period last year.

- •Key Detractor: Falling export prices for the company’s long and heavy steel products severely impacted profitability.

2. Future-Oriented Growth Strategies

Despite the challenging environment, Dongkuk Steel is not standing still. The company is actively pursuing several initiatives aimed at sustainable growth and shareholder value:

- •‘Steel for Green’ Strategy: A commitment to investing in eco-friendly processes to ensure long-term sustainability and meet ESG demands.

- •GFRP Business Diversification: The company is entering the Glass Fiber Reinforced Plastic (GFRP) market, a high-growth sector. This move diversifies its portfolio away from traditional steel, with sales expected to commence in late 2025.

- •Enhanced Shareholder Returns: Management has raised the minimum dividend to KRW 400 per share for three years and already declared an interim dividend of KRW 200, signaling confidence to the market.

3. Complex Macroeconomic Factors

No Dongkuk Steel investment can be evaluated in a vacuum. Broader economic trends play a crucial role. For an in-depth look at market trends, investors often consult resources like the World Steel Association. Key factors include:

- •Exchange Rate: A rising KRW/USD exchange rate (KRW 1,400.50) can be a double-edged sword. While it benefits exporters, it increases the cost burden for companies like Dongkuk Steel that rely heavily on imported raw materials.

- •Interest Rates: Sustained high interest rates increase borrowing costs and can dampen construction activity, a key demand driver for steel.

Impact of the NPS Sale on Dongkuk Steel Stock

The sale by a major institutional investor like the NPS sends a powerful short-term negative signal. However, long-term value will ultimately be dictated by the company’s ability to execute its growth strategy and navigate the market recovery.

Short-Term: Negative Sentiment and Volatility

The immediate impact is likely negative. The NPS is a market bellwether, and its selling can trigger a decline in investor confidence, putting downward pressure on the Dongkuk Steel stock price. Investors should anticipate increased trading volume and heightened price volatility as the market digests this news. Learning to interpret moves by institutional investors is a key skill.

Mid- to Long-Term: Fundamentals are Key

The long-term outlook depends heavily on why the NPS sold. If it was a simple portfolio rebalancing, the impact may be fleeting. If it was based on deep concerns about Dongkuk Steel’s fundamentals, it could signal a prolonged period of weakness. The market will now watch to see if other investors absorb this selling pressure and if the company’s strategic initiatives, like the GFRP business, begin to bear fruit.

Investor Action Plan: Should You Buy Dongkuk Steel Stock Now?

Given the disappointing first-half earnings and a high PER of around 40x (as of June 30, 2025), the stock carries a valuation burden. The NPS Dongkuk Steel sale adds another layer of uncertainty.

- •Short-Term (1-3 Months): Caution. It is prudent to wait and observe the market’s reaction. A premature purchase could lead to catching a falling knife. Monitor support levels and wait for signs of stabilization.

- •Mid- to Long-Term (6-12+ Months): Observe and Approach. A successful Dongkuk Steel investment from here hinges on tangible improvements in fundamentals. If the GFRP business shows strong performance and the steel market begins a cyclical recovery, the current price could represent an attractive entry point, especially if the NPS sale proves to be purely strategic.

Frequently Asked Questions (FAQ)

What does the NPS’s reduction in Dongkuk Steel stake mean?

It means the National Pension Service sold a portion of its shares, decreasing its holding from 6.23% to 5.22%. As a major institutional investor, this action is seen as a negative short-term signal that can pressure the stock price.

What is Dongkuk Steel’s recent financial performance?

For the first half of 2025, both revenue and operating profit declined compared to the previous year. This was caused by a slowdown in the construction and steel markets and falling export prices.

What is Dongkuk Steel’s GFRP business?

GFRP (Glass Fiber Reinforced Plastic) is a new business venture for Dongkuk Steel. It represents a key part of their strategy to diversify and find new growth engines outside the traditional steel sector, with sales planned for late 2025.

What are the key factors to monitor for Dongkuk Steel stock?

Investors should closely watch any further selling by the NPS, the actual sales performance of the new GFRP business, the pace of the global steel market recovery, outcomes of any major legal issues, and the company’s overall ESG compliance.