The market is buzzing about HD Hyundai Infracore stock, and for good reason. When South Korea’s largest and most influential institutional investor, the National Pension Service (NPS), significantly increases its stake in a company, it’s more than just a routine transaction—it’s a powerful signal about perceived value and future potential. This move has thrust HD Hyundai Infracore into the spotlight, prompting investors to ask a critical question: What does the NPS see that we should be paying attention to?

This comprehensive HD Hyundai Infracore analysis will dissect the implications of the NPS’s increased shareholding. We will go beyond the headlines to provide an in-depth review of the company’s fundamentals, explore its strategic growth initiatives, and offer a balanced perspective on the potential rewards and risks for anyone considering an HD Hyundai Infracore investment.

The NPS Signal: A Major Vote of Confidence

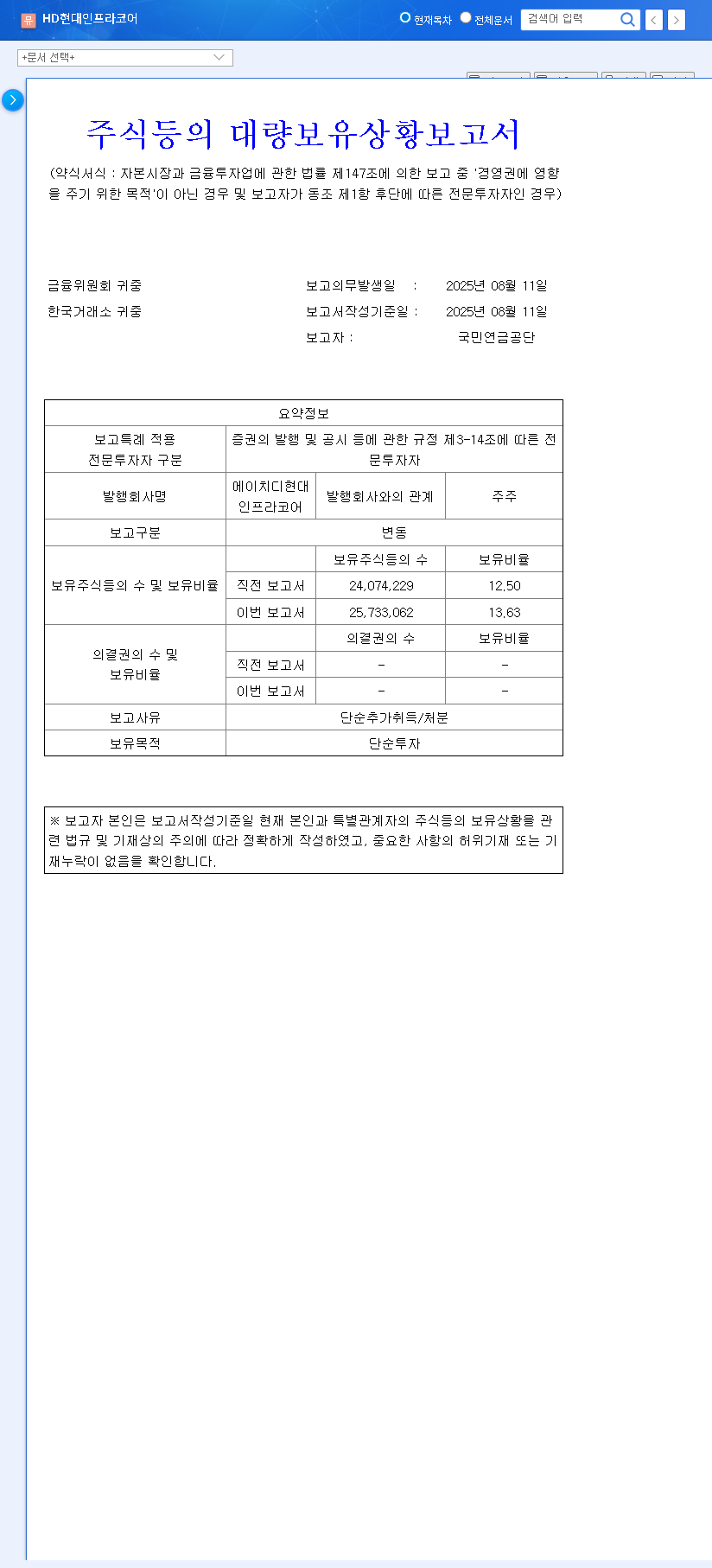

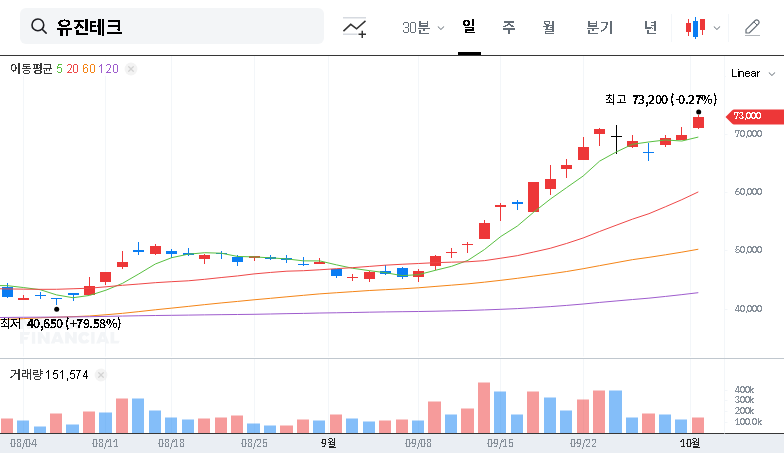

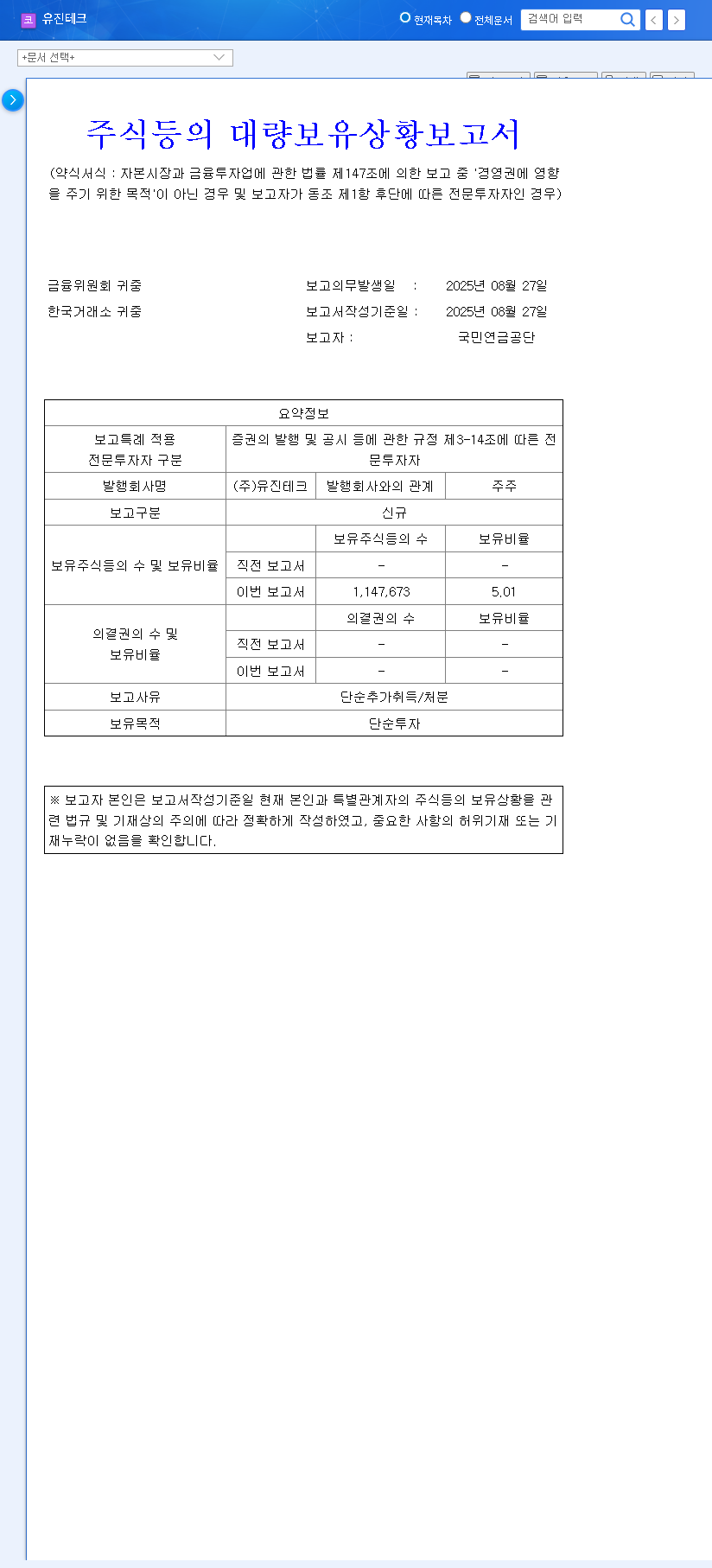

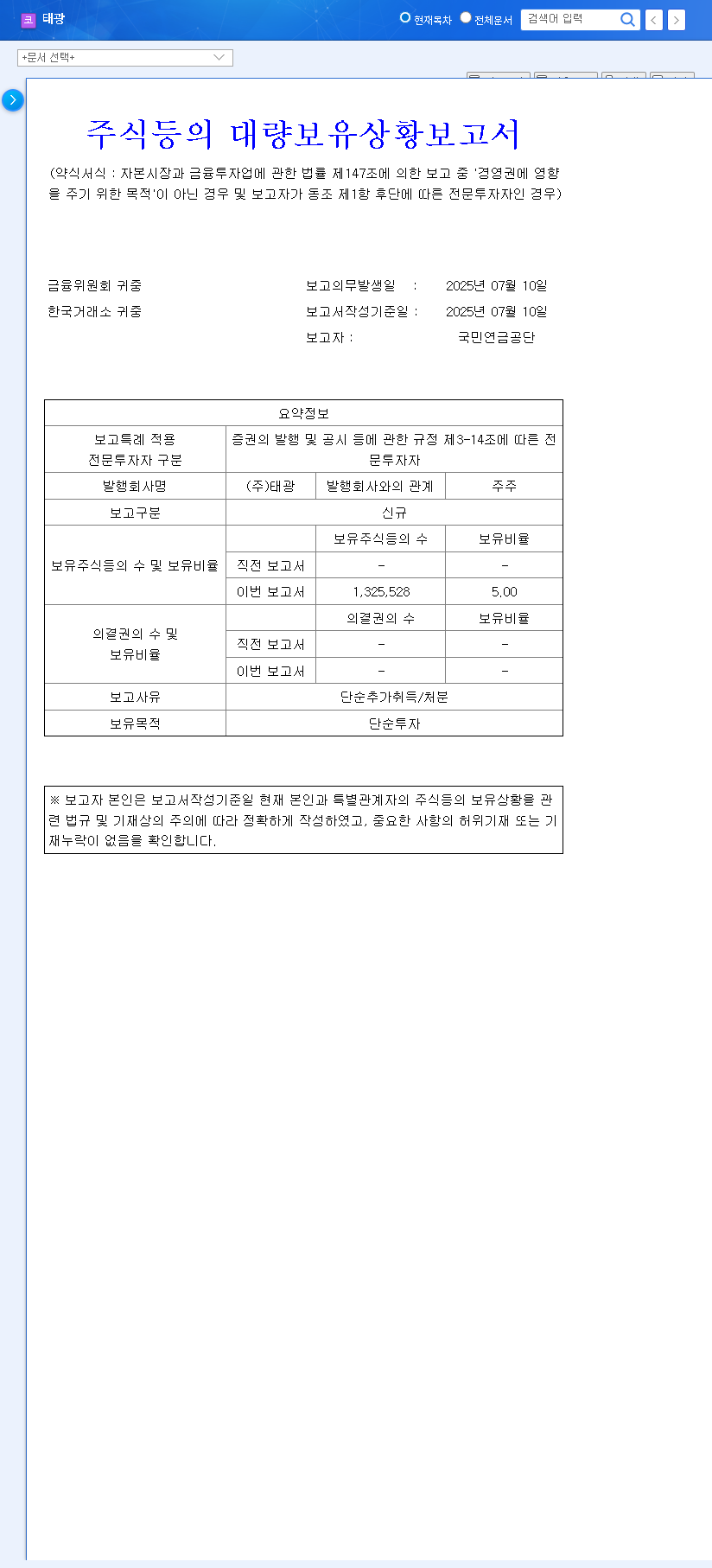

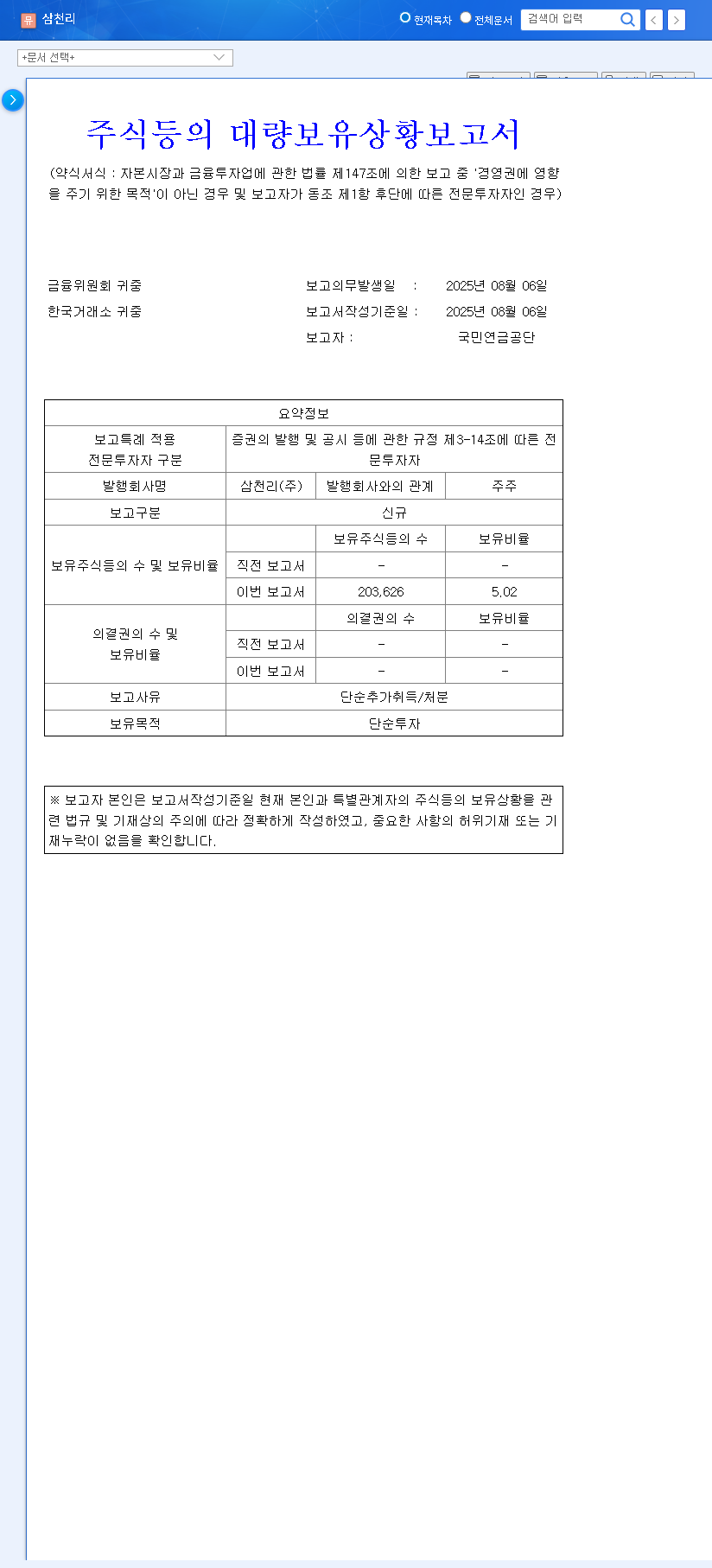

On October 1, 2025, a significant disclosure was made public. HD Hyundai Infracore announced that the National Pension Service had increased its holding from 12.50% to a substantial 13.63%. While the stated purpose of ownership was ‘simple investment,’ seasoned market watchers understand the weight of this phrase. It signifies a long-term belief in the company’s intrinsic value, separate from any short-term market speculation or activist intentions. This move was formally documented in an official disclosure to the financial authorities (Official Disclosure).

An increased stake from a bellwether institution like the NPS is often interpreted as a ‘seal of approval,’ validating a company’s financial health and strategic direction, which can attract a wave of secondary interest from other domestic and foreign investors.

Deep Dive: The Fundamentals Driving the Investment

The NPS’s decision wasn’t made in a vacuum. It is rooted in the robust and promising fundamentals of HD Hyundai Infracore. An examination of the company’s 2025 semi-annual report reveals a multi-faceted picture of stability and forward-looking strategy.

Financial Stability and Shareholder Focus

A healthy balance sheet is the bedrock of any sound investment. HD Hyundai Infracore demonstrates this with key metrics that suggest resilience and prudent management.

- •Manageable Debt: With a debt-to-equity ratio of 135.90% and a net debt ratio of 47.43%, the company maintains a stable, though leveraged, financial position typical for its capital-intensive industry.

- •Strong Solvency: An interest coverage ratio of 6.50 is excellent, indicating that the company’s earnings can cover its interest payments more than six times over, a strong sign of financial health.

- •Shareholder Returns: A commitment to a 31.4 billion KRW share buyback and cancellation program directly enhances shareholder value by reducing the number of outstanding shares, thereby increasing earnings per share.

Dual Engines of Growth: Business Segment Performance

The company’s dual focus on construction equipment and engines provides both diversification and synergistic opportunities. Our internal analysis on diversified industrial portfolios highlights the benefits of such a structure.

- •Construction Equipment: Despite macroeconomic headwinds causing a slight sales dip, the division is aggressively future-proofing. Through its new ‘DEVELON’ brand, it is targeting emerging markets and investing heavily in smart construction solutions like automation and telematics. A planned 208.8 billion KRW investment will further boost production capacity.

- •Engine Business: This segment has been a pillar of stability, showing solid performance by capitalizing on demand for high-output engines and stricter emissions standards. A planned 250.5 billion KRW investment is aimed at capturing new markets, such as the 1MW ultra-large power generation sector.

HD Hyundai Infracore Stock Outlook & Key Risks

The NPS’s backing provides a strong tailwind for the HD Hyundai Infracore stock outlook. In the short term, this institutional buying pressure is likely to increase trading volume and support the stock price. Over the long term, the validation of the company’s strategy could lead to a positive re-rating by the broader market.

However, a prudent investment decision requires acknowledging potential risks:

- •Macroeconomic Volatility: The company’s performance is tied to the global economy. As noted by leading financial publications like Bloomberg, factors like interest rates, commodity prices, and currency fluctuations can impact profitability.

- •Intense Competition: The construction equipment sector is highly competitive, with major global players. Continuous innovation and market share defense are crucial.

- •Synergy Realization: The potential benefits from the absorptive merger with HD Hyundai Construction Equipment are significant, but the successful integration and realization of these synergies are key to unlocking future value.

The Final Verdict

The National Pension Service’s increased stake is a compelling endorsement of the HD Hyundai Infracore investment thesis. It points to a company with a stable financial base, clear growth strategies in its core businesses, and a commitment to enhancing shareholder value. While external market risks persist, the combination of strong institutional backing and solid underlying fundamentals makes HD Hyundai Infracore stock a noteworthy candidate for investors with a long-term horizon. Continuous monitoring of financial disclosures and industry trends remains essential for any investment decision.