An important development for TAESUNG (323280) has captured the market’s attention: a significant stock purchase by its own CEO, Kim Jong-hak. When a top executive invests their personal capital into the company they lead, it’s often interpreted as a powerful vote of confidence. This article provides a comprehensive TAESUNG stock analysis, dissecting the implications of this move, the company’s strategic pivot to new growth engines, and what it means for potential investors.

Is this insider purchase a clear signal of upcoming success in its ventures into secondary batteries and camera modules? Or are there underlying financial risks that warrant caution? We will explore TAESUNG’s core business, financial health, and the potential trajectory of its stock price.

Unpacking the CEO’s Strategic Stock Purchase

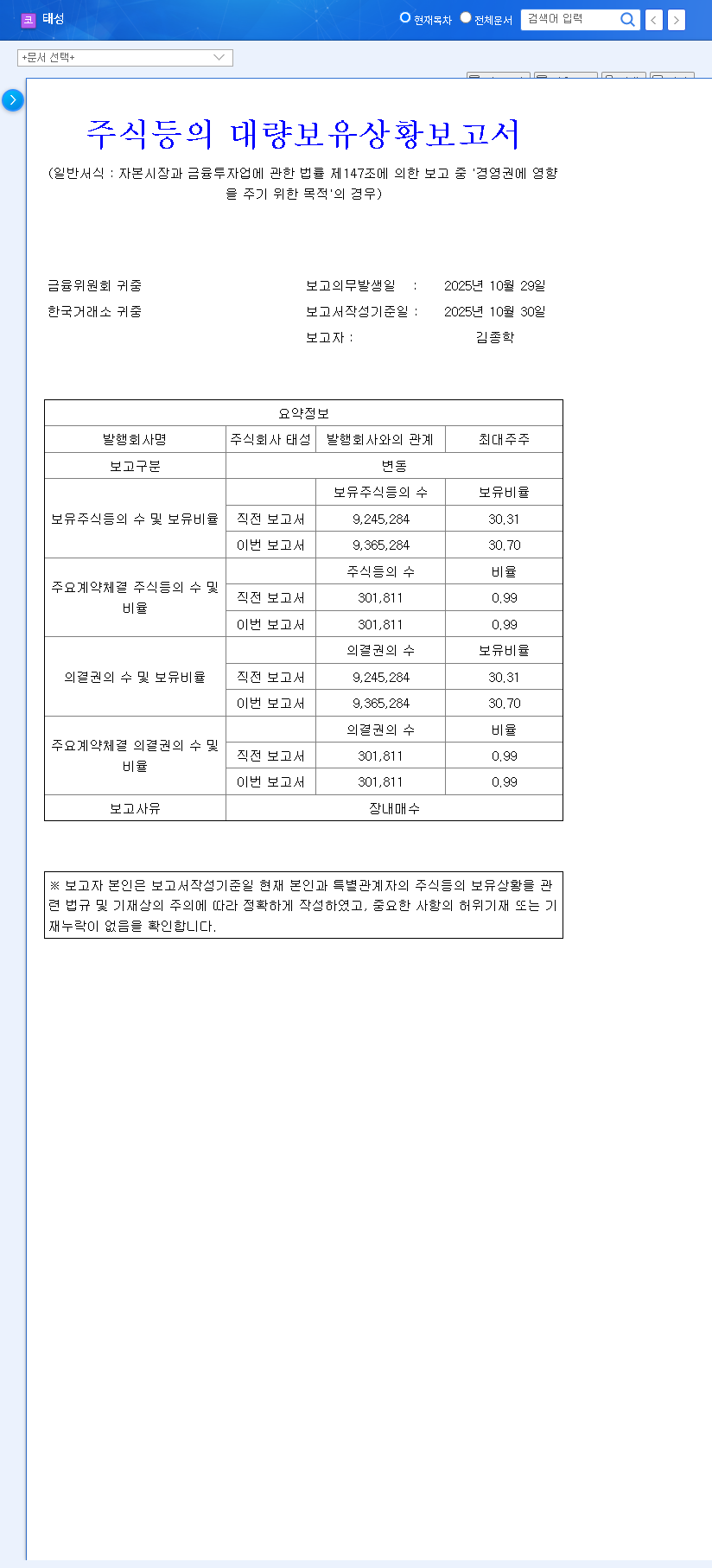

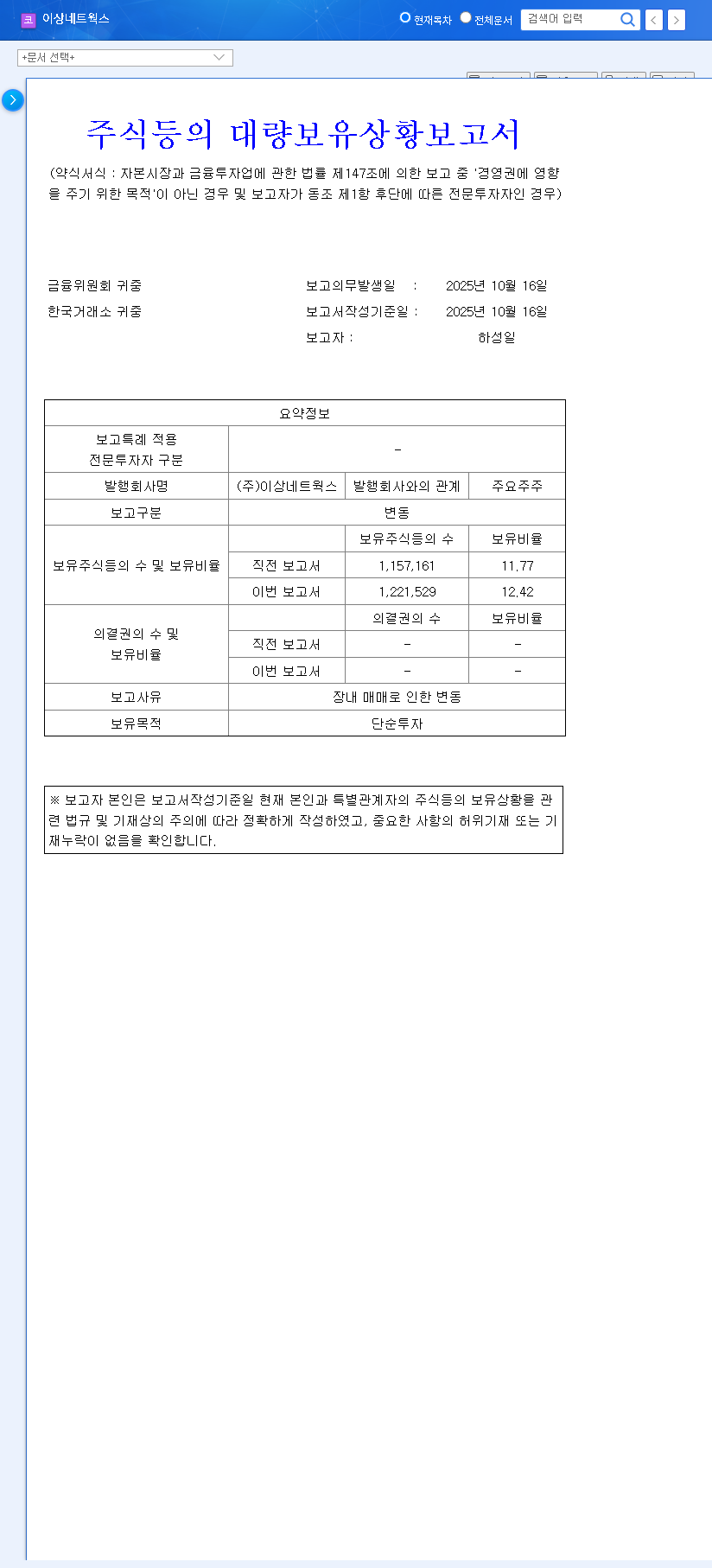

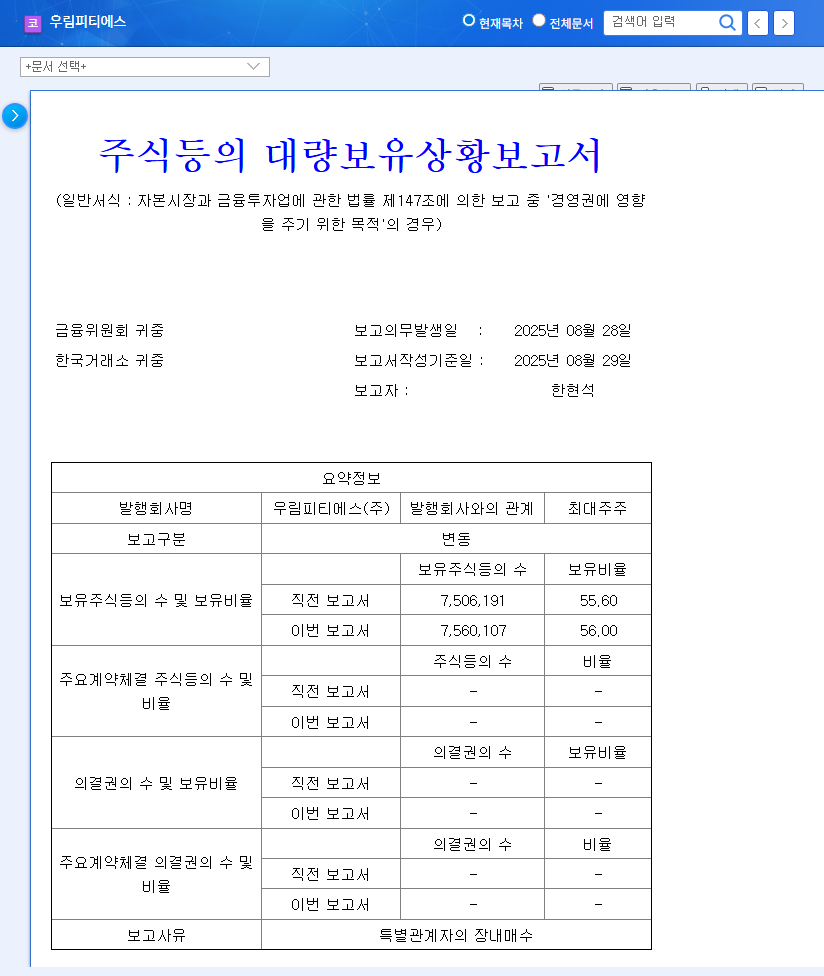

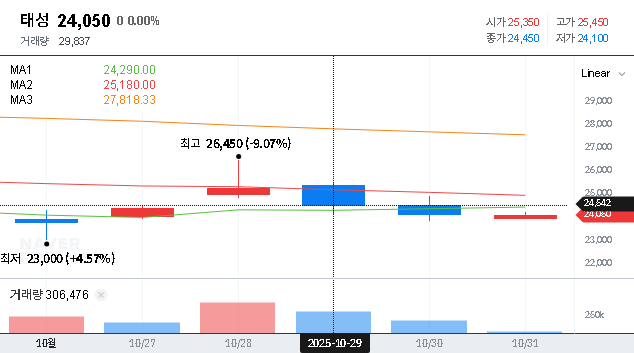

On October 31, 2025, it was disclosed that TAESUNG CEO Kim Jong-hak acquired 120,000 common shares through an open market purchase. This transaction increased his ownership stake by 0.35 percentage points, from 21.23% to 21.58%. The official filing for this event can be viewed here: Official Disclosure (DART).

Insider buying is one of the most compelling indicators in the market. While there can be many reasons for an executive to sell stock, there is generally only one reason to buy: they believe the stock price is going up.

What Does This TAESUNG CEO Purchase Signal?

- •Unwavering Confidence: This act is a direct financial commitment, suggesting the CEO has a firm belief in the company’s long-term strategy and future valuation, far beyond what is presented in standard financial reports. For more on this principle, you can read about the significance of insider trading on authoritative financial sites.

- •Belief in New Ventures: With the traditional PCB business facing headwinds, the company’s future is tied to its TAESUNG growth engines. This purchase signals that the CEO anticipates significant breakthroughs and revenue generation from the camera module and secondary battery divisions.

- •Shareholder Value Alignment: By increasing his personal stake, the CEO further aligns his financial interests with those of other shareholders, reinforcing a commitment to enhancing long-term value.

TAESUNG (323280): A Company in Transition

To understand the context of the CEO’s move, it’s crucial to analyze TAESUNG’s business segments. The company is evolving from a traditional manufacturer into a diversified tech player.

Core and Emerging Business Areas

- •PCB Automation Equipment: The foundational business, known for high-tech polishing and etching equipment. While a stable base, this market faces cyclical demand and intense competition.

- •Camera Module Components: A high-growth area, manufacturing M-Spacers for apertures. This division is poised to benefit from the proliferation of multi-camera systems in smartphones, autonomous vehicles, and advanced surveillance.

- •Secondary Battery Equipment: Perhaps the most exciting venture, involving anode plating equipment. This positions TAESUNG to capitalize on the explosive growth of the global electric vehicle (EV) market. For more on this sector, see our guide on investing in the secondary battery supply chain.

Financial Health & Investment Thesis

A balanced TAESUNG investment strategy requires a clear-eyed look at the financials. As of H1 2025, the company reported sales of KRW 16.187 billion and an operating loss of KRW 2.741 billion. While the ongoing losses are a concern, they must be weighed against the company’s strengthened balance sheet.

Thanks to a successful IPO and rights offering, TAESUNG boasts substantial current assets (KRW 99.997 billion) and total equity (KRW 128.126 billion). This robust financial cushion is critical, as it provides the necessary capital to fund R&D and scale production for its new businesses without immediate liquidity concerns. The core challenge, and the central point of the investment thesis, is translating these investments into profitable revenue streams.

Investment Strategy: A Balanced View

The CEO’s purchase is a strong positive catalyst, but it doesn’t erase the fundamental challenges. Investors should consider the following:

- •Bull Case (Positive Outlook): The CEO’s conviction proves prescient. TAESUNG secures key patents and mass-production contracts in the secondary battery sector, leading to a significant revenue inflection point. The camera module business grows steadily, and the company achieves profitability within the next 18-24 months.

- •Bear Case (Cautionary Outlook): The transition takes longer than expected. Delays in mass production, intensifying competition, or macroeconomic headwinds stall growth. The company continues to burn cash without a clear path to profitability, and the initial positive sentiment from the CEO’s purchase fades.

Key Milestones to Monitor

For those considering an investment in TAESUNG (323280), it’s crucial to track concrete progress. Watch for company announcements regarding:

- •Successful acquisition of secondary battery patents.

- •Commencement of mass production for new product lines.

- •New client contracts or supply agreements.

- •Quarterly earnings reports showing a trend toward reduced operating losses and revenue growth in the new segments.

In conclusion, the CEO’s share purchase is a compelling narrative for TAESUNG (323280), but it should be seen as the beginning of a story, not the end. It validates the potential of the company’s strategic shift and offers a reason for optimistic monitoring. Diligent investors will now watch for the fundamental execution that must follow this signal of confidence.