This comprehensive Hyundai Glovis stock analysis dives into the company’s recent Q3 2025 earnings report, which fell short of market expectations. While the numbers may cause short-term concern for investors, a closer look reveals a strategic pivot towards long-term growth. We will dissect the financial results, evaluate the underlying fundamental strengths and risks, and outline a prudent investment strategy for navigating the current landscape.

Is the recent dip in Hyundai Glovis earnings a warning sign, or does it present a strategic entry point for long-term investors who believe in the company’s future in smart logistics and green energy? Let’s explore the data.

Deconstructing the Q3 2025 Earnings Miss

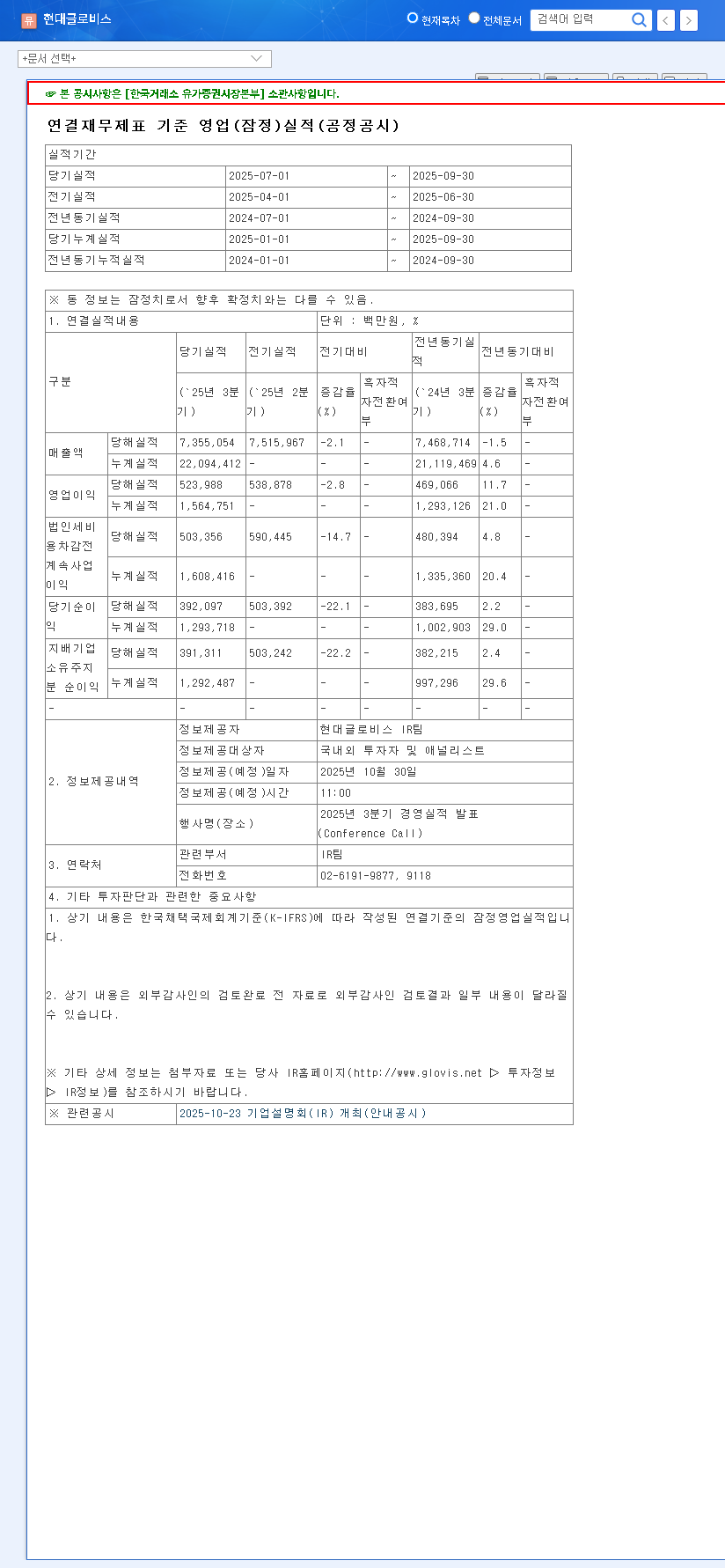

On October 30, 2025, Hyundai Glovis released its provisional consolidated financial results, revealing a slight underperformance against analyst consensus. The market reacted with caution, particularly to the more significant drop in net profit.

Here is a breakdown of the results compared to market estimates, as detailed in the Official Disclosure (DART):

- •Revenue: KRW 7,355.1 billion (Missed estimate of KRW 7,611.4 billion by -3.3%)

- •Operating Profit: KRW 524.0 billion (Missed estimate of KRW 530.3 billion by -1.2%)

- •Net Profit: KRW 391.3 billion (Missed estimate of KRW 428.1 billion by -8.6%)

The shortfall, particularly in net profit, can be attributed to a combination of factors, including fluctuating global freight rates and increased initial investment costs for new business ventures. This suggests a strategic allocation of capital towards future growth, even at the expense of immediate profitability.

Core Strengths: Building the Foundation for Future Growth

Despite the short-term earnings pressure, a thorough Hyundai Glovis stock analysis must look beyond a single quarter. The company is aggressively positioning itself in high-growth sectors that promise substantial long-term returns.

Strategic Expansion into High-Growth Areas

Hyundai Glovis is not just a traditional logistics firm; it’s evolving into a future-focused mobility and energy solutions provider. Key initiatives include:

- •EV Battery Logistics & Recycling: Tapping into the circular economy, this venture addresses the entire lifecycle of EV batteries, a critical component of the sustainable energy transition. This aligns perfectly with the growth of its parent, Hyundai Motor Group. For more on this trend, see our guide to investing in the EV supply chain.

- •Smart Logistics Solutions: The acquisition of Altio enhances its capabilities in automated warehousing and AI-powered logistics, driving efficiency and offering high-margin services to third-party clients.

- •Clean Energy Shipping: Expanding its fleet and capabilities for LNG, hydrogen, and ammonia transport positions the company at the forefront of the global energy shift.

Solid Financials and ESG Leadership

The company’s stable credit ratings (Moody’s Baa1, S&P BBB+) provide a solid financial bedrock for these growth investments. Furthermore, its consistent inclusion in the DJSI World Index and high marks for climate change response (CDP ‘A’ rating) attract a growing pool of ESG-focused institutional capital, which can support the stock’s valuation over time.

While the market may react to a single quarter’s data, savvy investors focus on the strategic capital allocation and structural changes that build long-term enterprise value. Hyundai Glovis’s investments in future-proof industries are a clear signal of its forward-looking strategy.

Navigating Risks and Market Headwinds

No investment is without risk. A balanced Hyundai Glovis investment thesis must acknowledge potential challenges:

- •Macroeconomic Sensitivity: As a global logistics provider, the company’s performance is tied to global trade volumes and economic health. A potential global slowdown, as tracked by institutions like The World Bank, could impact its core shipping and logistics segments.

- •New Business Uncertainty: While promising, new ventures in EV recycling and hydrogen transport carry execution risk and require significant upfront capital, which can continue to weigh on short-term profits.

- •Competitive Landscape: The logistics industry is fiercely competitive. Hyundai Glovis must continue to innovate to maintain its edge and protect its margins against both established players and new tech-driven disruptors.

Investment Strategy: A Prudent Approach

Given the crosscurrents of short-term weakness and long-term potential, a tiered investment strategy is advisable for the 086280 stock.

- •Short-Term (1-3 Months): A cautious, observational stance is warranted. The market may need time to digest the Hyundai Glovis earnings miss, and further price volatility is possible. Avoid chasing the stock and wait for a clear support level to form.

- •Mid-to-Long Term (1 Year+): For investors with a longer time horizon, price corrections could offer an attractive entry point. The strategy should be to ‘buy on dips,’ accumulating a position based on the long-term growth narrative. Key catalysts to monitor are the revenue growth and margin expansion in the new business segments.

In conclusion, while the Q3 2025 earnings were underwhelming, they do not derail the compelling long-term story. The ongoing transformation of Hyundai Glovis into a comprehensive, future-oriented logistics and energy solutions company remains intact. Investors who can look past the immediate noise may be rewarded as these strategic initiatives begin to bear fruit and contribute meaningfully to the bottom line.