The latest KZ Precision Corporation earnings report for Q3 2025 has sent ripples through the investment community. With significant declines in key financial metrics, investors are closely scrutinizing the company’s performance and future viability. Formerly known as Youngpoong Precision Co., Ltd., the company is navigating a challenging economic landscape.

This in-depth KZ Precision analysis will dissect the preliminary Q3 results, explore the underlying causes for the downturn, and evaluate the potential catalysts for recovery. We will provide a comprehensive outlook to help you make informed decisions about KZ Precision stock.

Dissecting the KZ Precision Corporation Q3 2025 Earnings Report

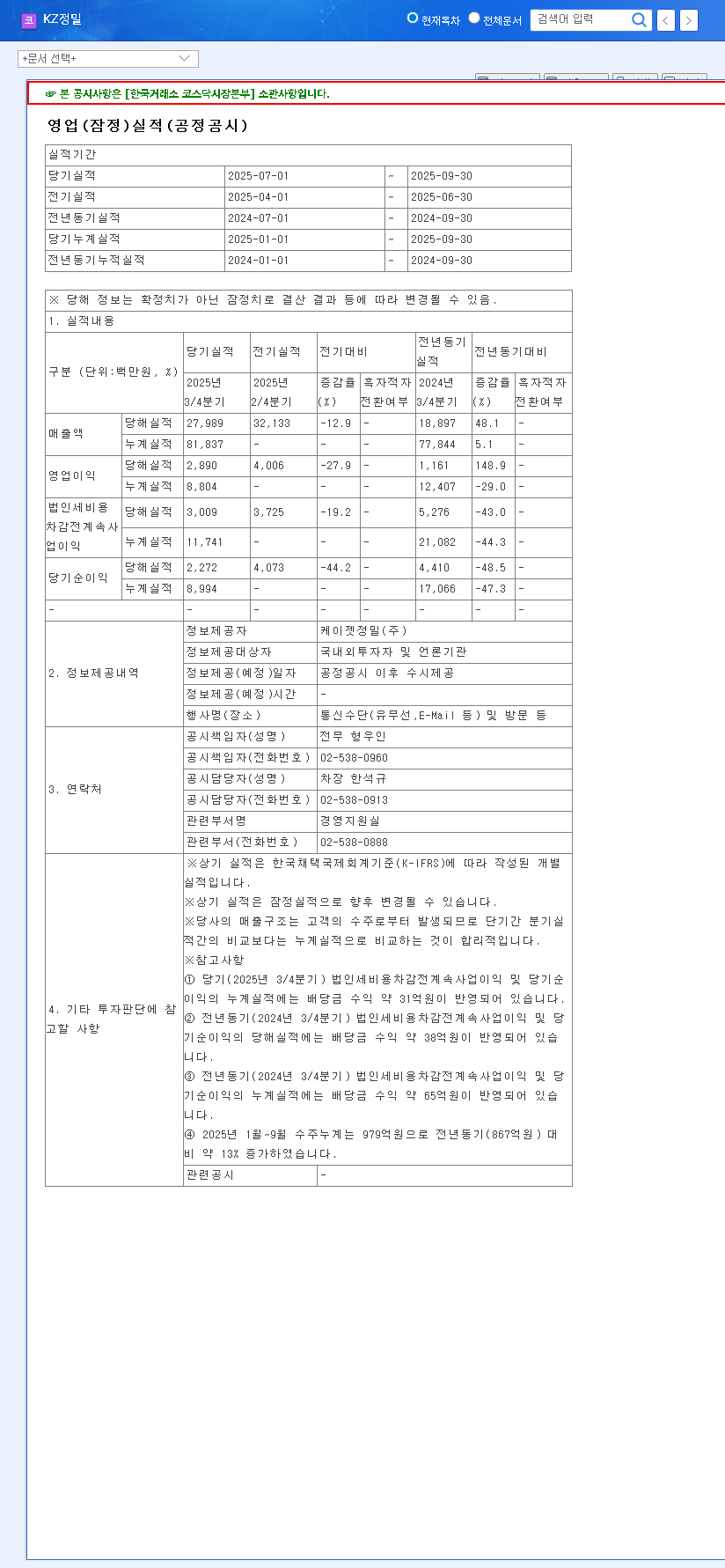

On November 6, 2025, KZ Precision Corporation released its preliminary operating results, revealing a notable contraction compared to the previous quarter. The official figures paint a stark picture of the current operational challenges. (Source: Official Disclosure)

The Q3 2025 numbers show a clear trend that requires careful examination. While the top-line figures are concerning, a closer look reveals nuances in profitability and future potential that shouldn’t be overlooked.

Key Financial Metrics (QoQ)

- •Revenue: KRW 28 billion, a decrease of 12.77%

- •Operating Profit: KRW 2.9 billion, a decrease of 27.5%

- •Net Income: KRW 2.3 billion, a significant decrease of 43.9%

These figures highlight a substantial deterioration in performance, confirming a trend of underperformance that has persisted since 2022. The primary driver behind this is a significant slowdown in sales for the company’s core products.

Fundamental Analysis: Headwinds and Silver Linings

The Core Challenge: Sluggish Product Sales

The root cause of the revenue decline lies in weak domestic and export sales of its main fluid machinery products: ‘Pumps/Valves/Castings.’ This business unit is highly sensitive to capital expenditure cycles in the industrial and petrochemical sectors. A global economic slowdown, as reported by institutions like Reuters, has led to investment contraction, directly impacting demand for KZ Precision’s offerings. Increased competition and a decline in inventory turnover further compound these market pressures.

A Beacon of Hope: The Order Backlog

Despite the grim results, there is a significant positive factor: a substantial order backlog of KRW 63.146 billion as of mid-2025. This backlog represents confirmed future revenue and could serve as a powerful catalyst for a performance turnaround in the upcoming quarters. The key for investors is to monitor how efficiently the company can convert this backlog into actual sales and cash flow.

Financial Stability and Corporate Changes

On a positive note, the company’s financial structure remains stable. A reduction in total liabilities has kept the debt-to-equity ratio at a healthy 25.7%. Furthermore, major corporate shifts, including a name change from Youngpoong Precision Co. and a change in the major shareholder to Jericho Partners Co., Ltd., could signal a new strategic direction. These changes, coupled with potential positive impacts from currency fluctuations, are important variables that could influence long-term growth.

Investment Strategy for KZ Precision Stock

Given the current volatility, a cautious and well-researched approach is paramount. The conflicting signals—poor recent performance versus a strong order backlog—mean investors should focus on leading indicators of a potential turnaround. A successful long-term investment strategy will depend on the company’s ability to execute.

Strategic Investor Checklist: What to Monitor

- •Order Backlog Conversion: Track quarterly reports to see if the KRW 63.1 billion backlog is translating into recognized revenue.

- •Overseas Market Penetration: Look for announcements of new orders from the target markets of the Middle East and Southeast Asia.

- •Profitability Improvements: While revenue is down, the Q3 operating profit margin improved slightly to 10.36%. Monitor for further cost reduction and efficiency gains.

- •New Management Synergy: Observe the strategic direction under Jericho Partners. Are they bringing positive changes that could unlock value?

Conclusion: A Challenging Path to Transformation

The KZ Precision Corporation earnings for Q3 2025 undeniably reflect a difficult period. The company faces significant market headwinds that have impacted its core business. However, it is not without potential. The solid financial footing, a massive order backlog, and a strategic push into new global markets provide a potential pathway to recovery.

Investors should weigh the short-term risks against the company’s long-term transformation strategy. Cautious optimism and diligent monitoring of the key performance indicators outlined above will be crucial in navigating an investment in KZ Precision stock.