This comprehensive SEEGENE stock analysis provides a deep dive into the company’s recent activities, including its treasury stock disposal and H1 2025 earnings report. For investors considering a SEEGENE investment, understanding these developments is crucial. We’ll explore SEEGENE’s financial health, its position in the dynamic molecular diagnostics market, and provide a forward-looking perspective to help you make informed decisions about stock 096530.

Understanding the SEEGENE Treasury Stock Disposal

On November 12, 2025, SEEGENE announced a strategic decision to dispose of 1,334 common shares from its treasury. According to the company’s official disclosure, this action is not a market sale but is specifically intended for granting Restricted Stock Units (RSUs) to its employees. RSUs are a form of equity compensation used to incentivize and retain key talent by aligning their interests with those of shareholders. The complete details can be reviewed in the official filing. (Source: DART Report)

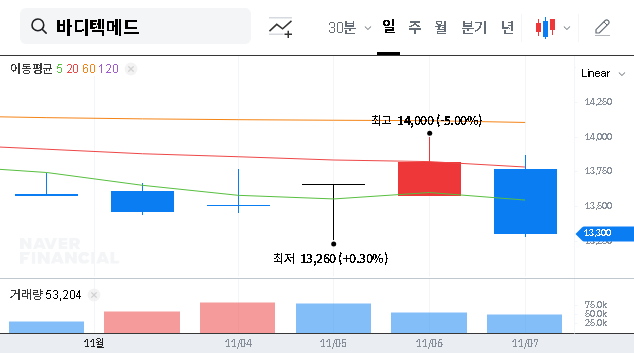

Impact on Stock Price and Investor Sentiment

Given the small volume of the disposal (1,334 shares) relative to the total shares outstanding, the direct, short-term impact on the stock price is expected to be minimal. In fact, markets often interpret RSU grants positively, viewing them as a sign of a healthy corporate culture focused on long-term growth and employee motivation. From a mid-to-long-term perspective, a well-motivated team can drive innovation and operational excellence, which are fundamental to increasing corporate value. Therefore, this move is unlikely to negatively affect the overall SEEGENE investment thesis.

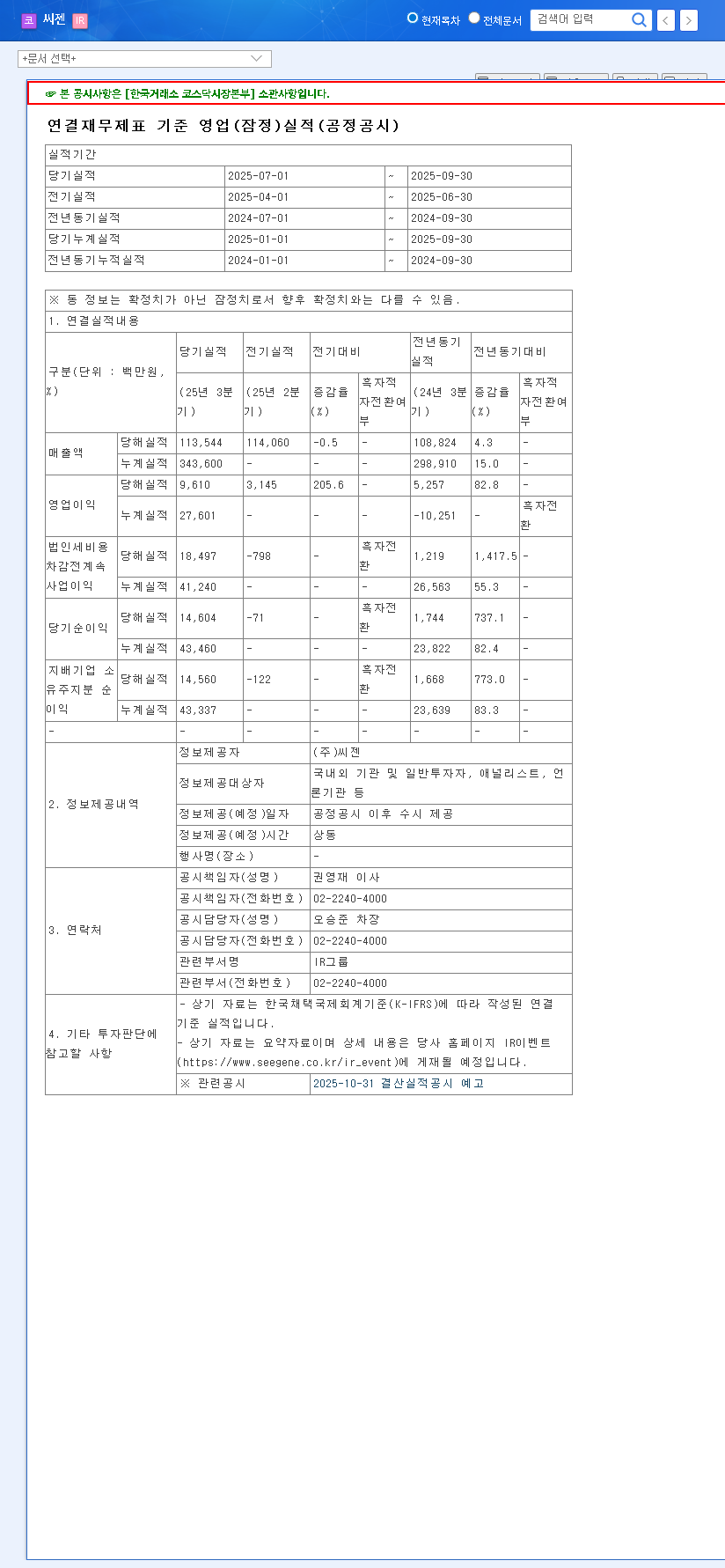

Decoding the H1 2025 Earnings Report

The 096530 earnings report for the first half of 2025 revealed a crucial pivot towards profitability, even as top-line revenue saw a decline from pandemic-era highs. This demonstrates effective cost management and operational efficiency.

- •Positive Operating Profit: The company successfully returned to operating profitability, recording 17.99 billion KRW.

- •Improved Net Profit: Net profit showed significant improvement, reaching 28.86 billion KRW.

- •Key Financial Drivers: Profitability was driven by the integration of subsidiaries, the strength of its core technologies, and successful global market penetration initiatives.

- •Solid Financial Health: SEEGENE maintains a stable debt-to-equity ratio of 22.02% and a strong capital structure, all while dedicating a significant 14.58% of revenue to R&D.

Core Strengths and the Molecular Diagnostics Market

SEEGENE’s long-term value is anchored in its technological superiority and the favorable trends in its target market. The global in-vitro diagnostics (IVD) market is on a strong growth trajectory, projected to reach $119.4 billion by 2030, according to a report from Grand View Research. Within this, the molecular diagnostics market continues to expand as demand for precise, early-stage disease detection grows.

SEEGENE’s competitive edge comes from its proprietary technologies like High Multiplex and 3Ct, which allow for the simultaneous detection of multiple pathogens in a single test, increasing efficiency and reducing costs for healthcare providers.

Potential Risk Factors to Monitor

No investment is without risk. For SEEGENE, investors should keep a close eye on the following factors:

- •Exchange Rate Volatility: With 93% of its revenue from exports, fluctuations in currency exchange rates can significantly impact reported profits. A 10% change could alter net profit by approximately 27.7 billion KRW.

- •Internal Controls: While improvements have been made, historical deficiencies in internal controls related to distributor revenue recognition require ongoing vigilance.

- •Macroeconomic Headwinds: Global interest rate trends, inflation, and geopolitical factors can affect investment sentiment and operational costs. For more on this, see our guide to understanding macroeconomic risks.

Final SEEGENE Stock Analysis and Investment Thesis

In summary, SEEGENE demonstrates strong fundamentals and is well-positioned in a growing industry. The company’s return to profitability, commitment to R&D, and dominant technological capabilities present a compelling case for a long-term SEEGENE investment. The recent SEEGENE treasury stock disposal for RSU grants is a non-event for valuation but a positive signal for corporate governance.

Based on this analysis, the overall outlook remains positive. Investors with a mid-to-long-term horizon may find the current position an attractive entry point. However, it is crucial to continuously monitor the identified risk factors, particularly currency fluctuations and global economic conditions, and adjust your strategy accordingly.