The upcoming HYUNDAI HOME SHOPPING NETWORK CORPORATION IR (Investor Relations) event represents a pivotal moment for the company, its shareholders, and potential investors. This is more than a standard corporate briefing; it’s a crucial platform where the company will outline its strategic direction, address profitability concerns, and shape market perception for the foreseeable future. For those tracking the company’s performance, this event is an unmissable opportunity to gain insight directly from its leadership.

This in-depth analysis will dissect the core details of the IR, evaluate its potential market impact, and highlight the critical metrics and narratives that investors should closely monitor to make informed decisions.

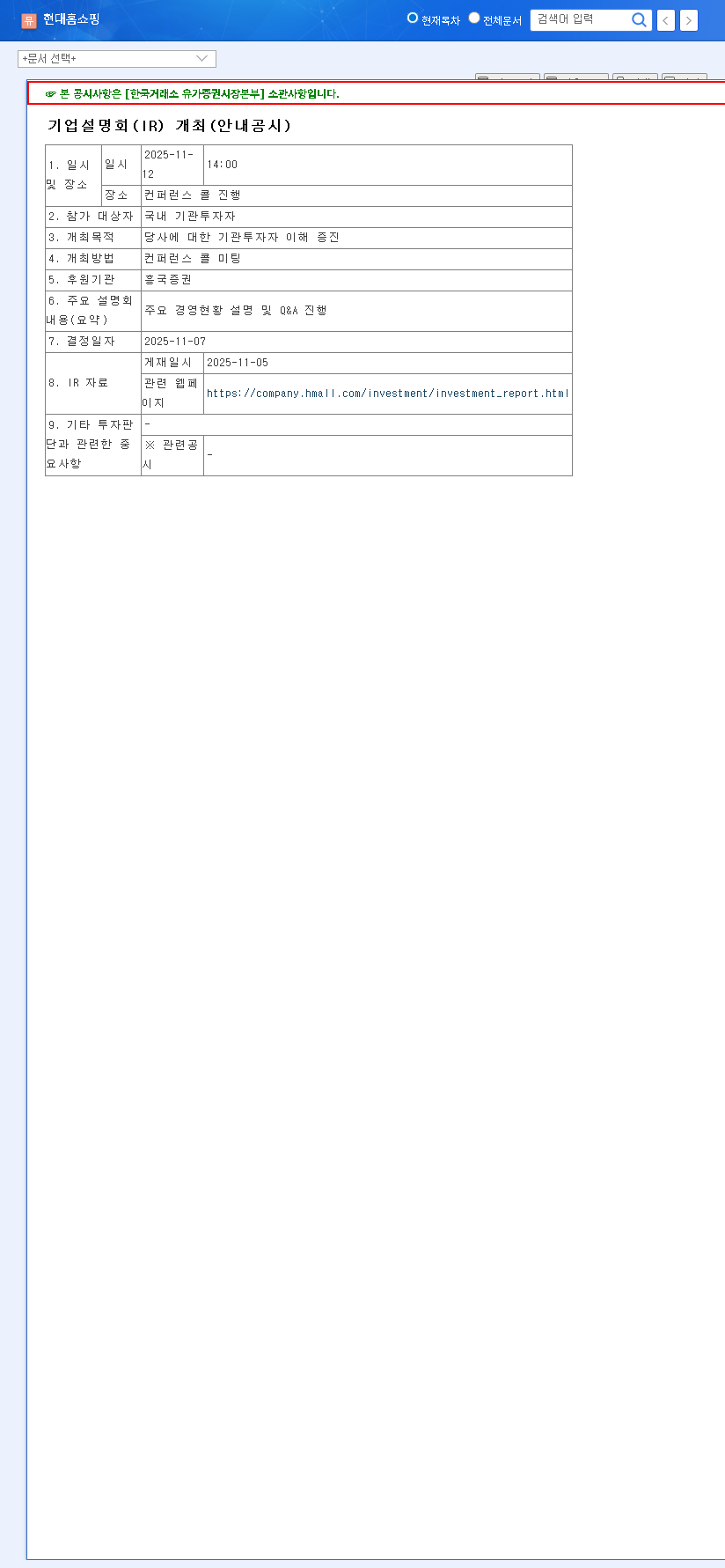

Event Details: The HYUNDAI HOME SHOPPING NETWORK CORPORATION IR

HYUNDAI HOME SHOPPING NETWORK CORPORATION has officially scheduled an IR event for institutional investors. The primary goal is to foster a deeper understanding of the company’s current operational status and forward-looking strategy.

- •Date: November 12, 2025

- •Time: 2:00 PM (KST)

- •Agenda: Key management status updates, strategic initiatives, and an open Q&A session.

- •Source: View the Official Disclosure (DART Report)

Why This IR Matters: Decoding the Impact on Fundamentals

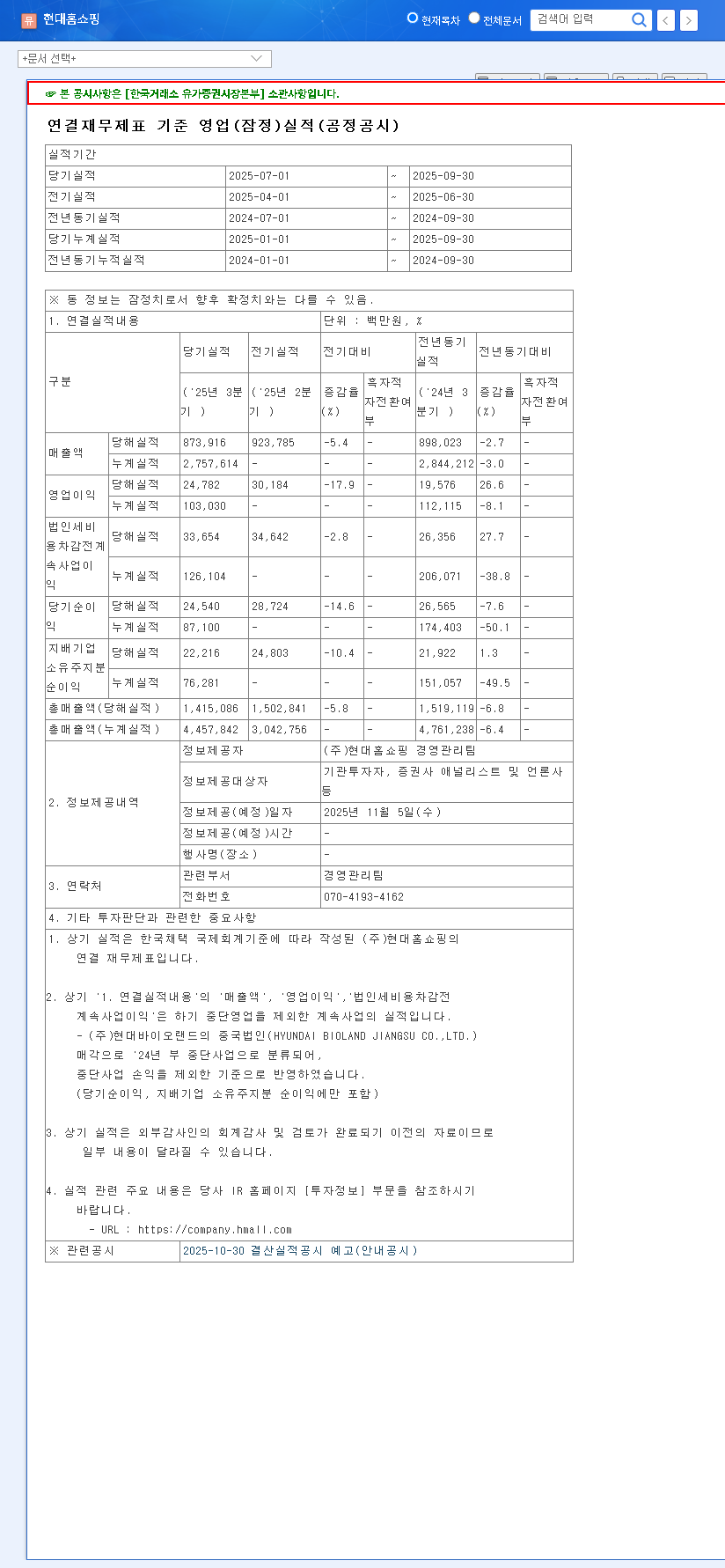

It’s essential to distinguish between a company’s actions and the market’s perception of those actions. An IR announcement, in itself, does not alter the company’s core corporate fundamentals—its financial health, assets, or operational efficiency. However, it can profoundly influence the market’s valuation of those fundamentals.

The narrative presented during an IR event can shift investor sentiment dramatically, creating a new lens through which the market assesses a company’s intrinsic value and future growth potential.

Potential Catalysts for a Positive Re-evaluation

- •Robust Growth Strategy: Clear, data-backed evidence of growth in key segments, like the ‘Hansome’ apparel division or advancements in mobile and media commerce, could significantly boost investor confidence.

- •Profitability Roadmap: A detailed plan addressing the recent dip in net profit margins with specific cost-management initiatives and efficiency improvements would be highly valued.

- •Transparent Communication: A management team that provides transparent, candid answers during the Q&A builds long-term trust, which is often priced into the stock.

Potential Triggers for a Negative Outlook

- •Stagnation in Core Business: Any indication of slowing growth in the primary home shopping channel without a viable offset from other ventures could raise red flags.

- •Ambiguous Future Outlook: Vague statements about future drivers or a pessimistic view of the market environment can create uncertainty and deter investment.

- •Evasive Q&A Responses: A failure to adequately address tough questions from analysts can be interpreted as a lack of strategy or a sign of hidden problems.

The Macroeconomic Backdrop: External Pressures

No company operates in a vacuum. The effectiveness of the strategies discussed at the HYUNDAI HOME SHOPPING NETWORK CORPORATION IR will be viewed against a challenging global economic landscape. Investors will be listening for how management plans to navigate these external forces.

Key factors include persistent high interest rates, which increase borrowing costs, and significant currency volatility (KRW/USD, KRW/EUR), impacting the cost of imported goods and international competitiveness. According to global market reports, these pressures are expected to continue, making corporate risk management a key topic of interest.

Investor Action Plan: What to Watch For

This investor relations event is an opportunity for a comprehensive assessment. Investors should focus on both the ‘what’ and the ‘how’—the substance of the plans and the conviction with which they are delivered.

Key Questions to Be Answered

- •Growth Beyond ‘Hansome’: What are the concrete, next-generation growth drivers beyond the successful apparel division?

- •Digital Transformation & AI: What is the strategy for integrating AI to enhance customer experience, optimize logistics, and maintain a competitive edge in a tech-driven market?

- •Financial Resilience: How is the company managing its balance sheet and hedging against currency and interest rate risks?

- •Capital Allocation: Are there plans for share buybacks, dividend increases, or strategic M&A that could enhance shareholder value?

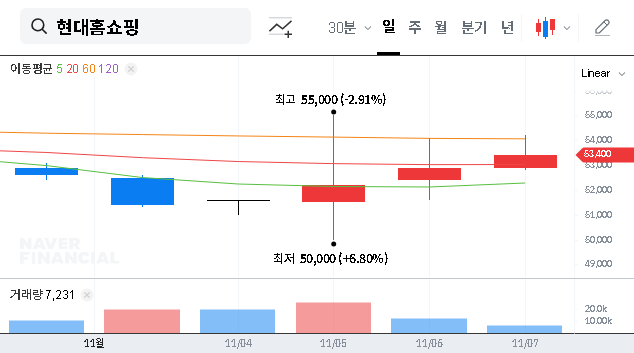

Ultimately, the market’s reaction to the HYUNDAI HOME SHOPPING NETWORK CORPORATION IR will hinge on the credibility and ambition of the vision presented. A clear, confident, and data-driven presentation could unlock significant value, while ambiguity could lead to further stock price pressure. Close monitoring of the event’s outcomes and the subsequent market analysis is therefore essential for all stakeholders.