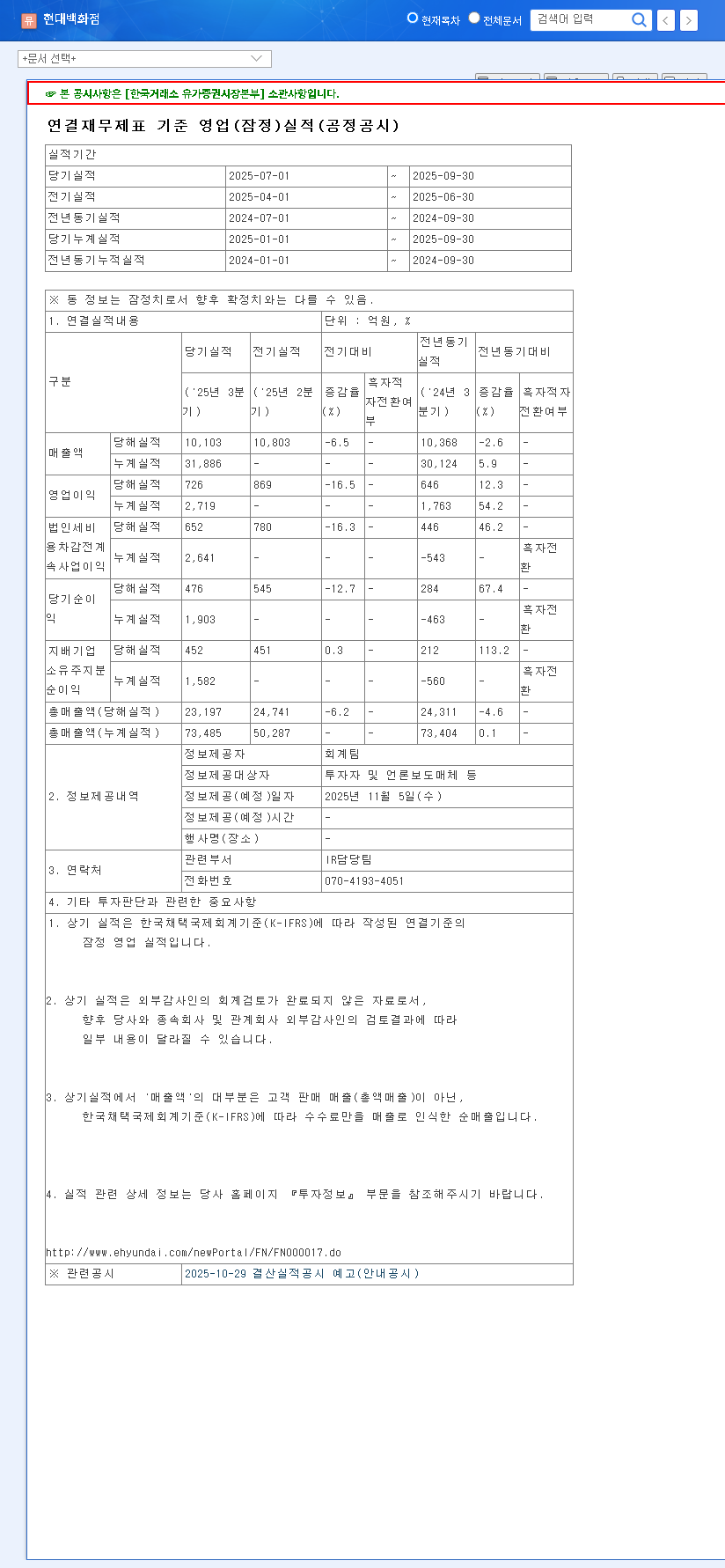

On November 5, 2025, HYUNDAI DEPARTMENT STORE CO.,LTD announced a significant capital increase, a strategic move that has captured the attention of investors and market analysts. This HYUNDAI DEPARTMENT STORE CO.,LTD rights offering, totaling ₩179.55 billion, is earmarked for its subsidiary, The Hyundai Gwangju. The core purpose is to fund the ambitious new flagship store, ‘The Hyundai Gwangju,’ set to become a cornerstone of the company’s national expansion. But what does this mean for the Hyundai Department Store stock? This deep-dive analysis explores the strategic rationale, financial implications, and potential impact on shareholder value.

Is this capital injection a masterstroke for securing long-term growth, or does it introduce risks of short-term stock dilution and financial strain? We examine the fundamentals to provide investors with a clear, comprehensive outlook.

Decoding the HYUNDAI DEPARTMENT STORE CO.,LTD Rights Offering

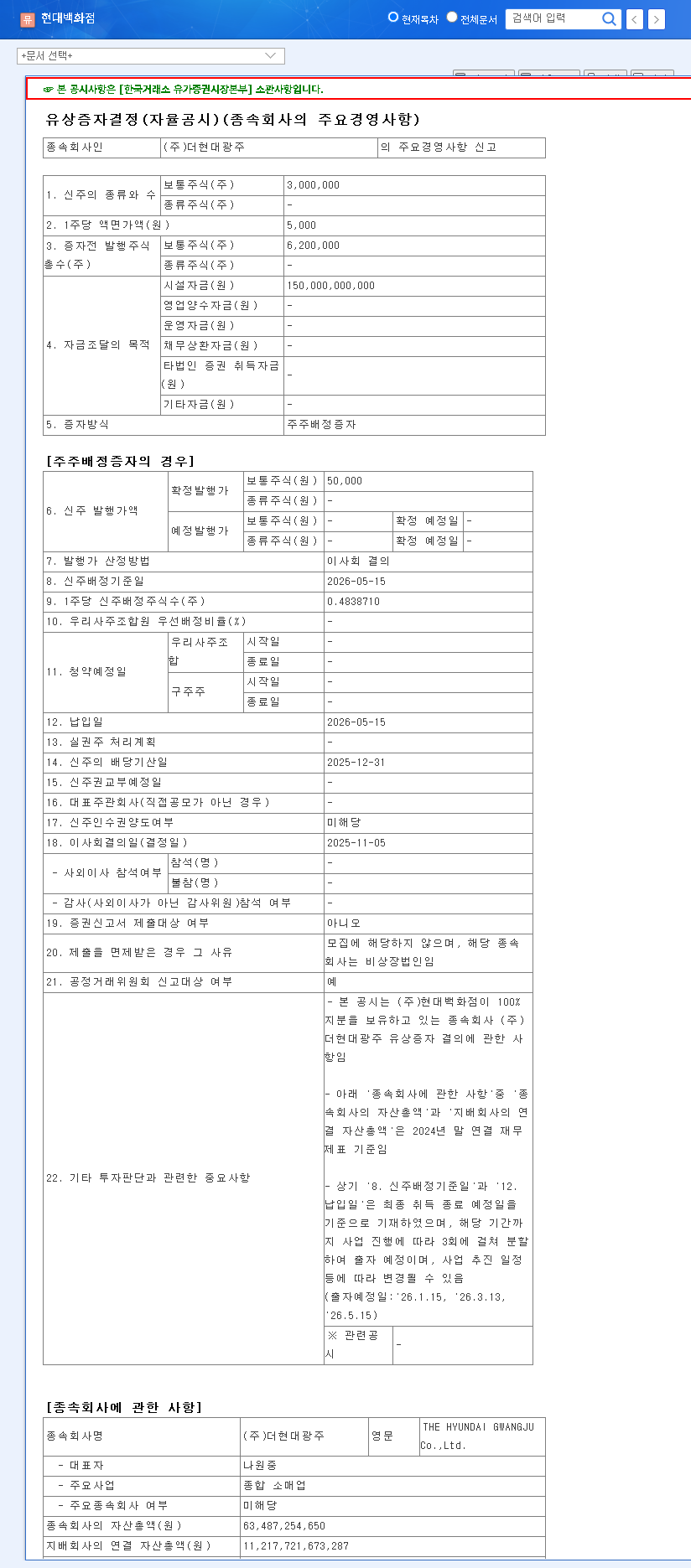

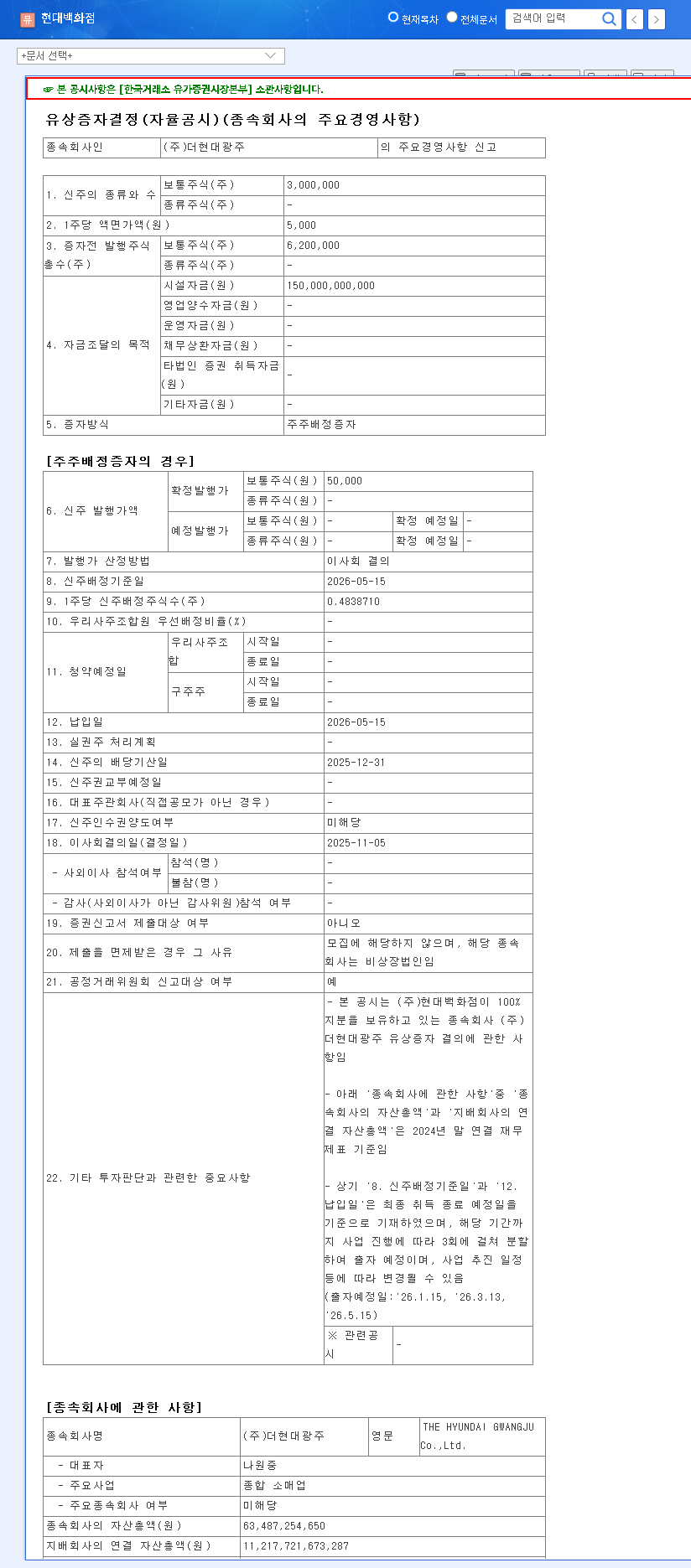

The company formalized this move via an official disclosure (Official Disclosure), detailing the specifics of the capital raise. This isn’t just a simple fundraising effort; it’s a calculated investment in a key future growth driver. The structure of the offering is a shareholder allocation, meaning existing shareholders are given the right to subscribe to new shares. Let’s break down the key figures:

- •Total Capital Raised: ₩179.55 billion

- •Issuance Method: Shareholder Allocation (Rights Offering)

- •Allocation Ratio: 0.48 new shares per 1 existing share

- •Primary Use of Funds: ₩150 billion for facility construction and operation of ‘The Hyundai Gwangju’

- •Payment Date: May 15, 2026

The ₩150 billion allocated for facility funds is the lifeblood for the new department store, which is slated to open its doors in 2027. This project is a critical piece of the company’s broader strategy to establish a presence in five major metropolitan cities across South Korea, solidifying its national retail footprint.

Strategic Implications & Financial Health Analysis

Fueling Future Growth: The Vision for The Hyundai Gwangju

The success of ‘The Hyundai Gwangju’ is paramount. It represents more than just a new building; it’s an engine for long-term revenue growth and market share expansion. By securing this funding, HYUNDAI DEPARTMENT STORE CO.,LTD ensures the project can proceed without delays, aiming to replicate the success of its other flagship locations. However, the initial phase will be critical. The new store must navigate a highly competitive retail landscape and achieve profitability swiftly to validate this massive investment. Success here could significantly bolster the Hyundai Department Store stock valuation in the long run.

A Look at the Balance Sheet: Financial Risks & Realities

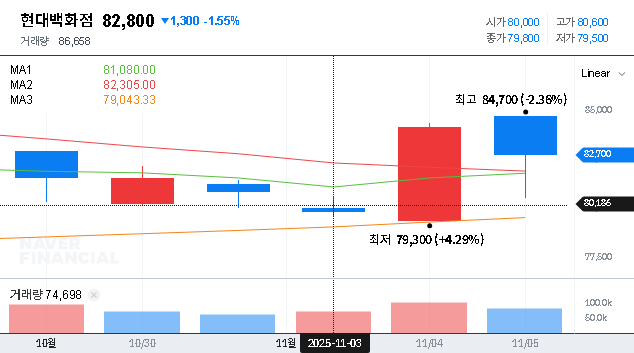

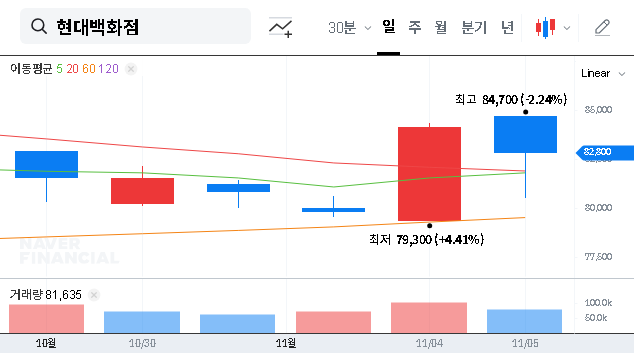

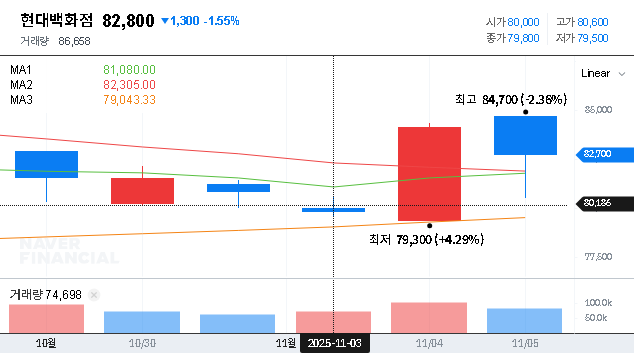

While the Hyundai capital increase is an investment in a subsidiary and not a direct addition to the parent company’s debt, it does have financial implications. The company’s consolidated debt-to-equity ratio of 78.94% already warrants careful management. The primary short-term risk for existing shareholders is dilution. By issuing new shares, the ownership stake of each existing share is reduced. This can create downward pressure on the stock price until the market is convinced that the future earnings from ‘The Hyundai Gwangju’ will outweigh the dilution effect. For more on sector trends, investors often consult major outlets like Reuters’ retail analysis.

Investment Thesis: A ‘Neutral’ Stance with Key Catalysts

After a thorough Hyundai stock analysis, our investment opinion remains ‘Neutral’. The decision balances a compelling long-term growth story with tangible short-term risks. Here’s a summary of the key factors shaping our view:

Positive Catalysts (The Bull Case)

- •Secured Growth Pipeline: The funding for ‘The Hyundai Gwangju’ provides a clear, long-term growth trajectory.

- •Diversified Portfolio: Beyond department stores, the company has interests in duty-free and furniture, providing some resilience.

- •Shareholder-Friendly Actions: Stated plans to acquire and retire treasury shares signal a commitment to enhancing shareholder value.

Negative Headwinds (The Bear Case)

- •Share Dilution: The rights offering will dilute existing shareholders’ stakes, potentially capping short-term stock performance.

- •Financial Leverage: The consolidated debt ratio remains a point of concern that requires prudent financial oversight.

- •Profitability Pressures: The duty-free business continues to be a drag on overall profitability, and recent earnings trends have been negative.

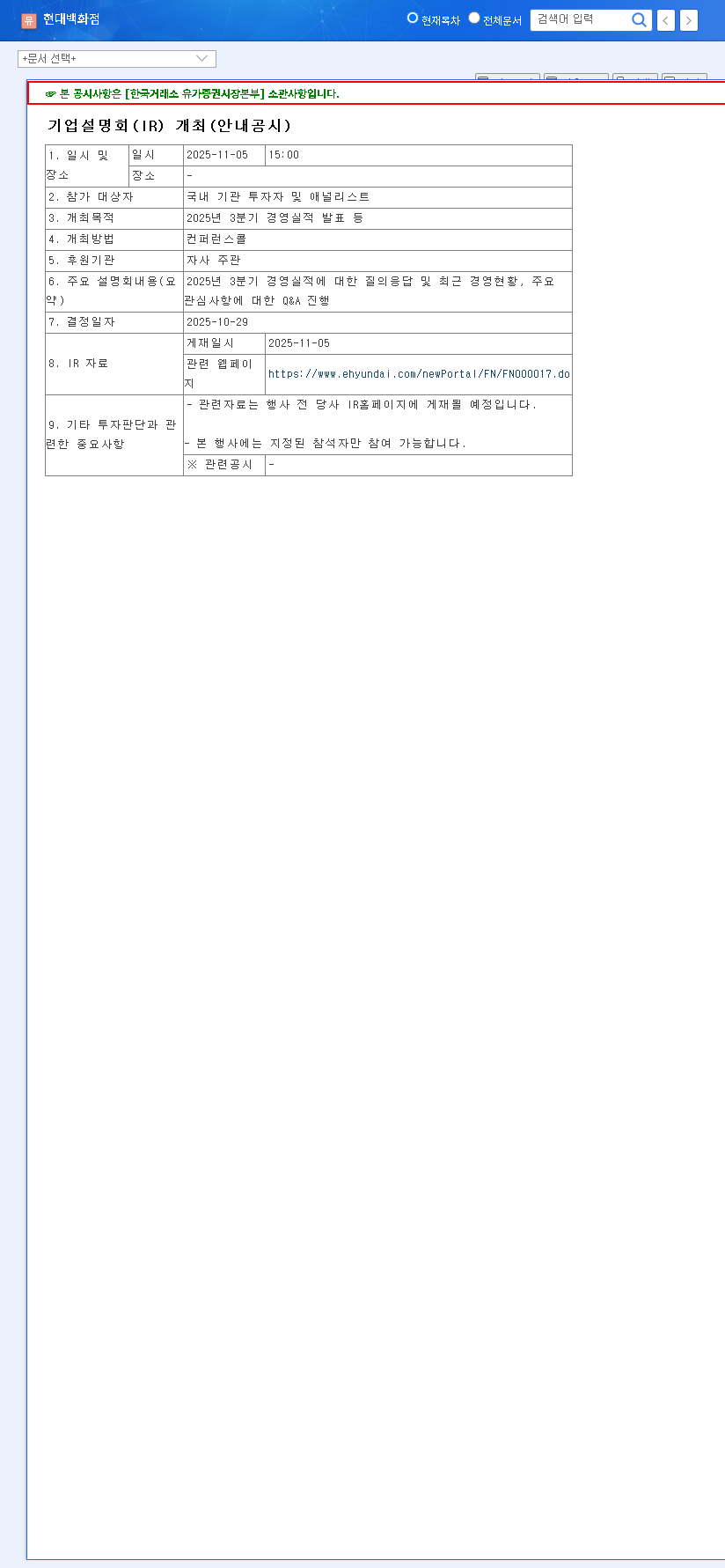

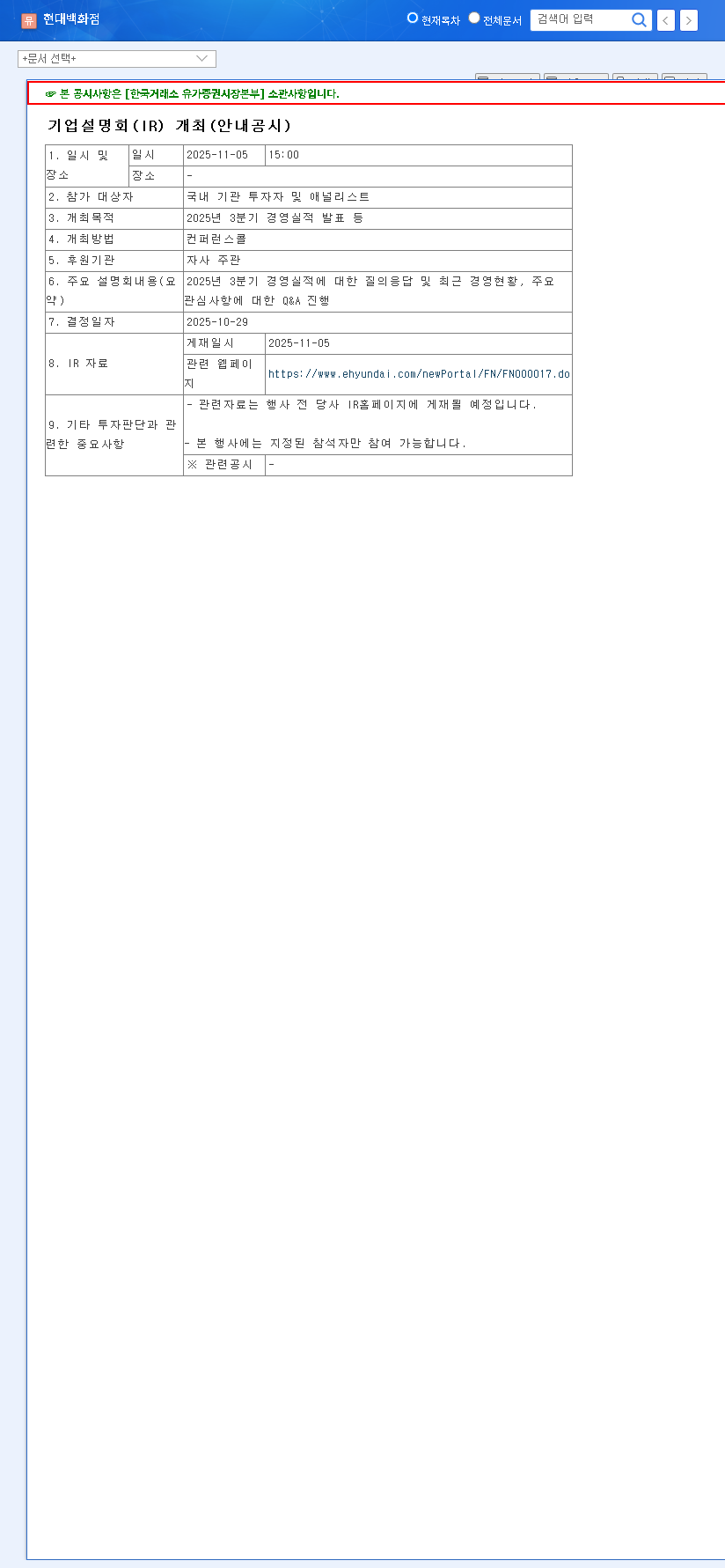

Investors should adopt a watchful waiting approach. Key milestones to monitor include the successful completion of the capital increase, progress reports on the Gwangju construction, and upcoming quarterly earnings. For those interested in this sector, our guide to retail stock investing offers further context. A sustained positive stock movement is most likely once ‘The Hyundai Gwangju’ proves its ability to generate strong returns and contributes positively to the company’s bottom line.

Frequently Asked Questions

What is the main purpose of the HYUNDAI DEPARTMENT STORE CO.,LTD rights offering?

The primary goal is to raise ₩179.55 billion to fund the construction and successful launch of its subsidiary’s new flagship store, ‘The Hyundai Gwangju’, a key project for the company’s national expansion.

How might this capital increase affect the stock price?

In the short term, the stock may face pressure due to concerns about share dilution. In the long term, if ‘The Hyundai Gwangju’ becomes a profitable venture, it is expected to act as a positive catalyst for the stock price and overall corporate value.

Why is The Hyundai Gwangju project so important?

‘The Hyundai Gwangju’ is a central piece of the company’s strategy to create a nationwide retail network by opening new stores in five major metropolitan areas. Its success is crucial for securing mid-to-long-term revenue streams and solidifying its market leadership.