Hyundai ADM Bio Inc. has just executed a significant financial maneuver by exercising its convertible bond rights, a move that injects fresh capital but also introduces over a million new shares to the market. For investors, this creates a critical dilemma: is this a strategic cash infusion that will fuel growth, or a desperate measure that will lead to significant share dilution? This comprehensive analysis will dissect the Hyundai ADM Bio Inc. convertible bond event, examine the company’s precarious financial health, and provide actionable strategies for investors navigating this pivotal moment.

The Core Event: A Closer Look at the Convertible Bond Exercise

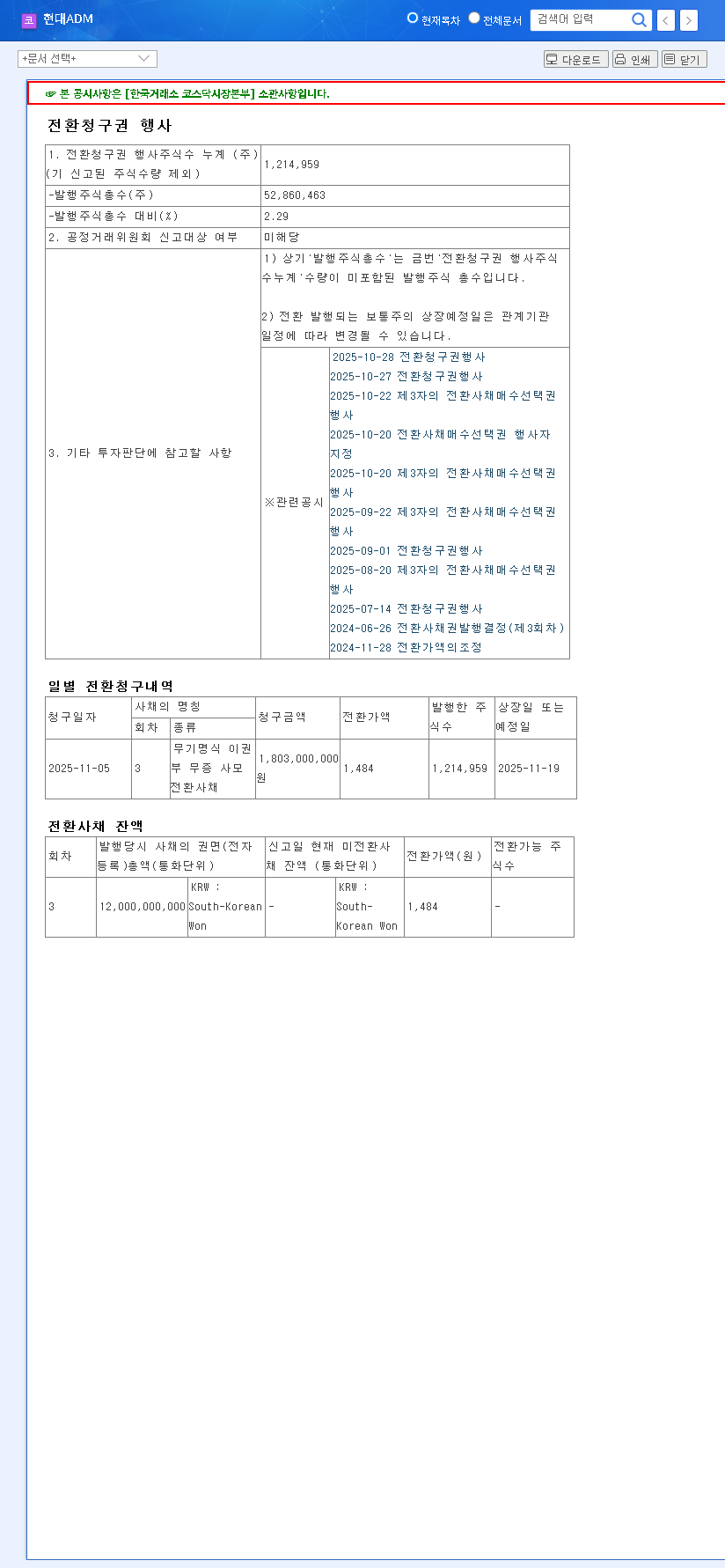

On November 5, 2025, Hyundai ADM Bio Inc. confirmed the exercise of conversion rights for its outstanding convertible bonds. In simple terms, bondholders are choosing to swap their debt for equity, betting on the future value of the company’s stock. This move has immediate and tangible consequences for the company’s capital structure and stock market dynamics.

The core conflict for investors is weighing the short-term benefit of ₩1.8 billion in liquidity against the long-term risk of share value erosion from 1.2 million new shares flooding the market.

Key Details of the Issuance

Understanding the specifics is crucial for any investor strategy. Here are the official details from the company’s disclosure:

- •Company: Hyundai ADM Bio Inc.

- •New Shares Issued: 1,214,959 (representing 2.29% of market cap)

- •Conversion Price: ₩1,484 per share

- •Total Capital Raised: Approx. ₩1.8 billion

- •Expected Listing Date: November 19, 2025

- •Source: Official Disclosure (DART Report)

Analyzing Hyundai ADM’s Shaky Fundamentals

The impact of a financing event like this cannot be judged in a vacuum. The company’s underlying health is the most critical factor. Unfortunately, Hyundai ADM Bio Inc.’s fundamentals are showing signs of significant strain, which magnifies the risks associated with this share issuance.

Struggling Business Segments

The company’s core operations are facing headwinds. The CRO (Contract Research Organization) business is experiencing a revenue decline of 14.4% year-over-year amid fierce competition. Meanwhile, its future growth engine—the anti-cancer drug development in its Bio Business—is still pre-revenue and fraught with uncertainty, including recent clinical trial setbacks. This paints a picture of a company whose primary revenue stream is shrinking while its future prospects remain speculative.

Deteriorating Financial Health

A look at the financial statements reveals a worrying trend that makes this Hyundai ADM Bio Inc. convertible bond exercise look more like a necessity than a strategic choice.

- •Expanding Losses: Operating losses have widened to ₩-4.37 billion, signaling deep profitability issues.

- •High Debt: The debt-to-equity ratio stands at a concerning 178.73%, and this bond conversion only addresses a fraction of its total debt.

- •Negative Cash Flow: With an operating cash flow of ₩-2.856 billion, the company is burning through cash, raising serious liquidity concerns.

Investor Playbook: Navigating the Aftermath

Given the weak fundamentals, investors must approach this situation with extreme caution. The short-term influx of shares will likely create downward pressure on the stock price around the November 19th listing date.

Short-Term Strategy (High Risk)

Traders should be wary of the supply overhang. The arbitrage opportunity—with the current stock price (₩2,780) well above the conversion price (₩1,484)—means bondholders have a strong incentive to sell their newly acquired shares for a quick profit. This could trigger a sell-off. Monitoring trading volume and price action closely on and after the listing date is paramount for anyone considering a short-term position.

Long-Term Investment Outlook

Long-term investors should disregard the noise of the bond conversion and focus entirely on fundamental improvements. Before considering an investment, look for tangible evidence of a turnaround. For more information on what makes these instruments tick, you can review this comprehensive guide to convertible bonds from a reputable financial source. Key milestones to watch for include:

- •Positive clinical trial data or partnerships in the bio-business.

- •A stabilization or return to growth in the CRO segment.

- •A clear plan for debt reduction and a path to positive cash flow.

Without these fundamental shifts, the company’s long-term prospects remain dim. Investors interested in this sector should also read our internal guide on How to Analyze Biotech Stocks for broader context.

Final Verdict: A Warning Sign for Investors

The Hyundai ADM Bio Inc. convertible bond exercise is not a signal of strength. While it provides a temporary liquidity patch, it fails to address the deep-seated problems within the company’s business model and financial structure. The immediate risk of share dilution and supply pressure outweighs the modest benefit of the capital injection. Until Hyundai ADM Bio Inc. demonstrates a credible and sustained operational turnaround, this event should be viewed as a warning sign rather than a catalyst for growth. The company’s future stock performance will be dictated by fundamental execution, not financial engineering.