The recent announcement of the Hotel Shilla Macau closure has sent ripples through the investor community, raising critical questions about the future of its Travel Retail (TR) division. On November 4, 2025, HOTEL SHILLA CO.,LTD (KRX: 008770) confirmed the termination of its duty-free operations at Macau International Airport. This move, detailed in an Official Disclosure, eliminates a business unit responsible for KRW 127.1 billion in annual revenue. Is this a sign of deepening trouble for the company’s duty-free segment, or is it a calculated strategic pivot designed to cut losses and strengthen long-term profitability? This comprehensive analysis provides an expert perspective for investors.

The Immediate Impact of the Hotel Shilla Macau Closure

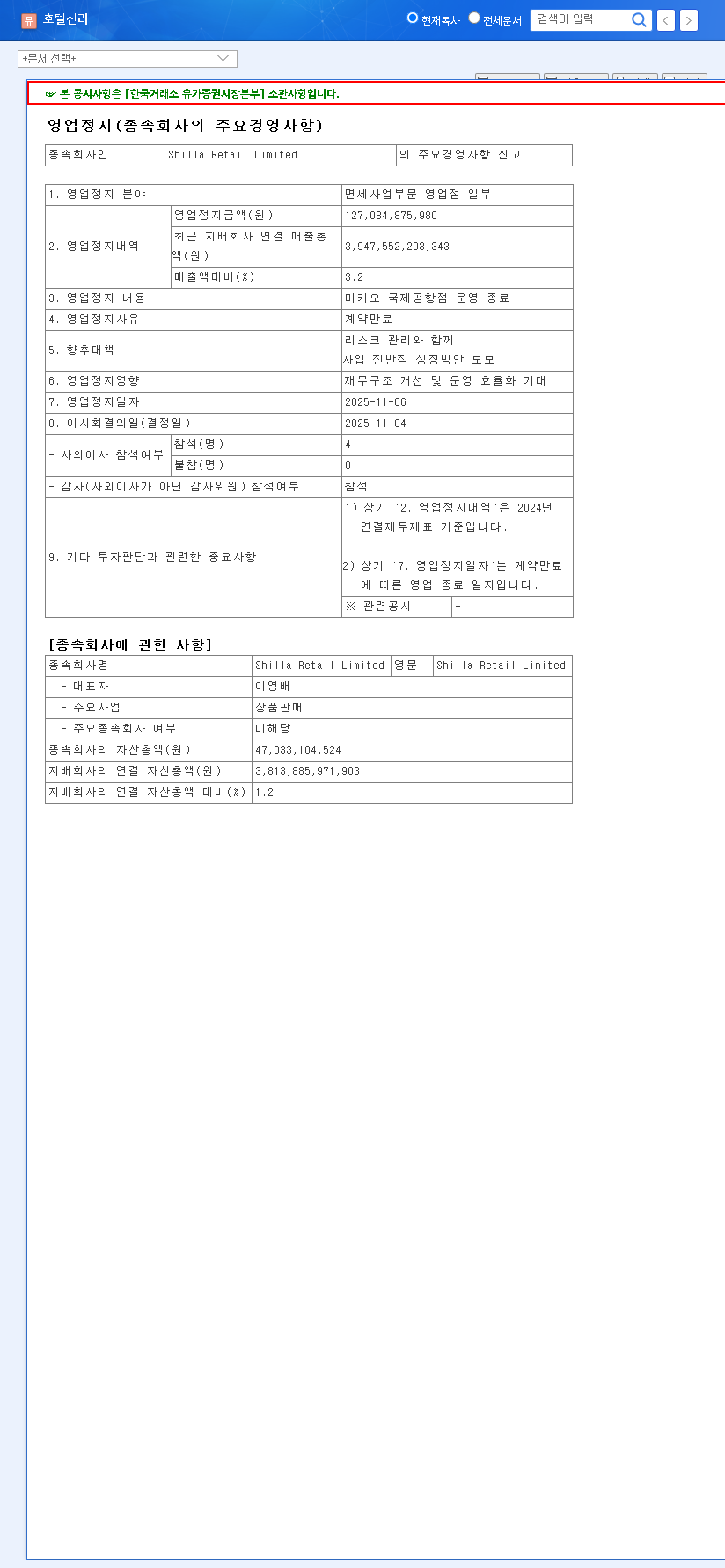

The closure of the Macau Airport store, effective November 6, represents a 3.2% loss of Hotel Shilla’s total sales. While seemingly small, its significance lies in what it signals about the persistent travel retail challenges facing the industry. The duty-free sector, particularly in Asia, has been squeezed by a perfect storm of factors. The decline in high-spending Chinese tourist groups and a governmental crackdown on ‘daigou’ (personal shoppers) have severely impacted revenue streams. Furthermore, intense competition and high fixed costs, such as airport concession fees, have eroded profit margins, leading to continuous operating losses for many operators in the region. This closure is a direct consequence of these harsh market realities.

The core dilemma for investors is whether to view this closure as an admission of defeat in a key market or as a prudent, albeit painful, step towards a more resilient and profitable business model.

Beyond Duty-Free: Hotel Shilla’s Diversified Strength

While the struggles of the Hotel Shilla duty-free division capture headlines, it’s crucial to analyze the company’s broader portfolio. The performance of its Hotel & Leisure division offers a powerful counterbalance and a glimpse into the company’s underlying stability.

The Resilient Hotel & Leisure Powerhouse

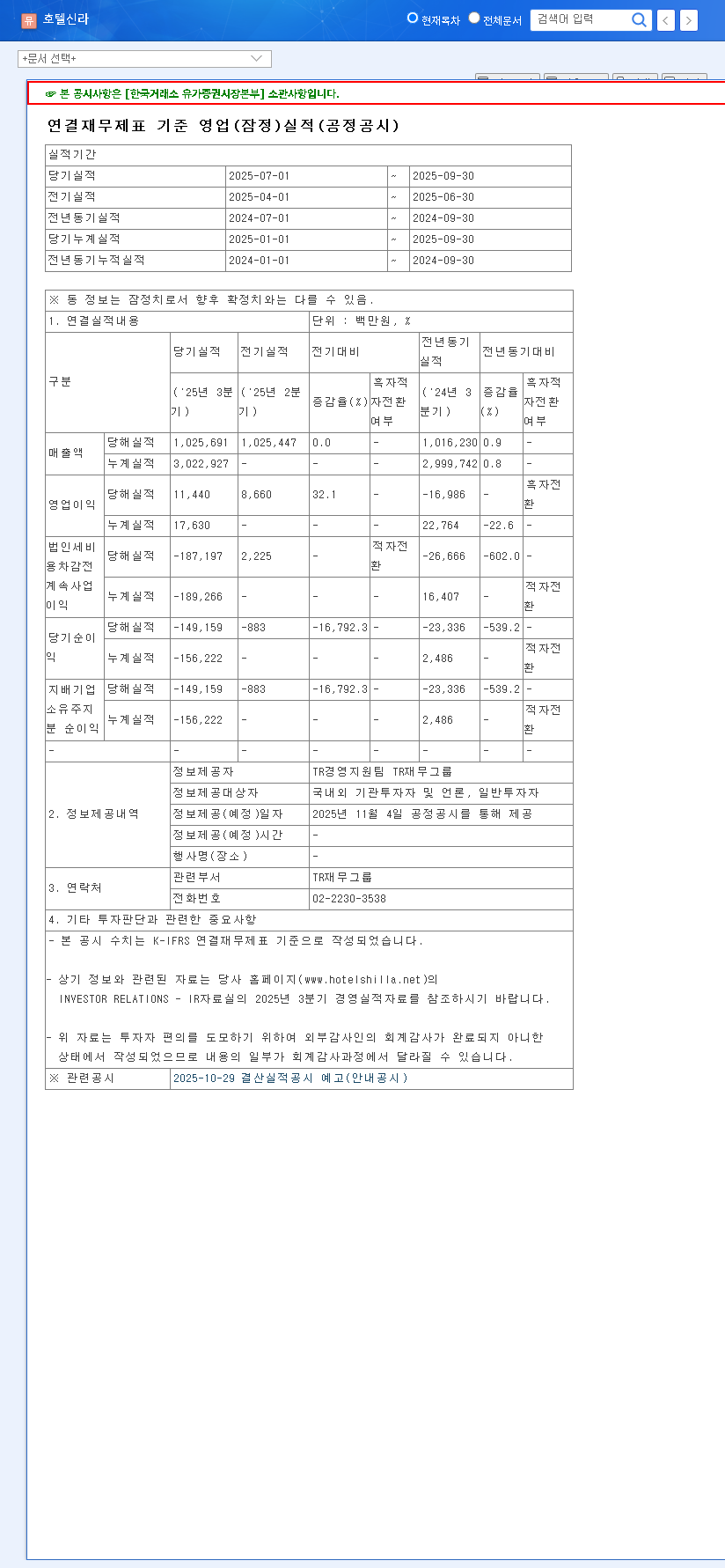

Driven by the post-pandemic resurgence in global travel and domestic demand, the Hotel & Leisure segment has demonstrated robust and steady growth. This division, which includes the iconic The Shilla Seoul and a portfolio of Shilla Stay business hotels, acts as a crucial buffer, partially offsetting the volatility of the TR business. This diversification is a key pillar of the company’s financial health, evidenced by a stable debt-to-equity ratio of 58.65% and significant cash reserves.

Pivoting to New Growth Engines

Hotel Shilla’s management is not standing still. The company has actively expanded its business objectives to include promising new ventures such as integrated resorts, condominium sales, and senior living facilities. These initiatives signal a forward-thinking strategy to secure future growth engines that are less dependent on the unpredictable travel retail market. Monitoring the progress of these new ventures is essential for any long-term Hotel Shilla stock analysis.

Investor Outlook: Key Factors to Monitor (008770)

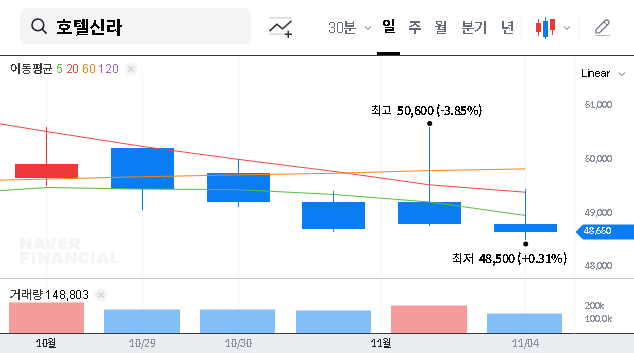

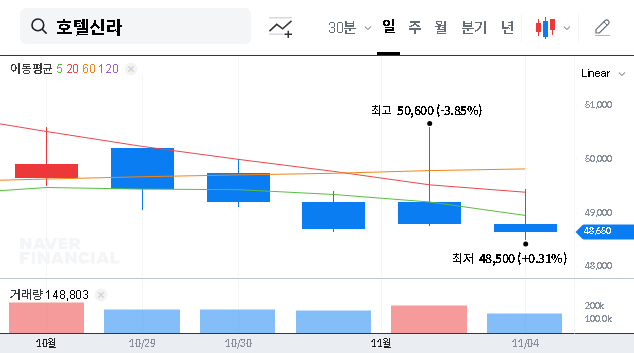

The Hotel Shilla Macau closure forces a re-evaluation. Short-term stock price volatility is likely as the market digests the revenue loss. However, savvy investors should focus on the mid-to-long-term strategic execution. The key is to assess whether this is the beginning of a successful portfolio optimization. For a complete picture, investors should also consult broader industry reports, such as this global travel retail market overview from Reuters.

Here are the critical points to monitor:

- •TR Division Restructuring: Watch for concrete plans to improve profitability in remaining duty-free locations. Is the company exiting other underperforming contracts or renegotiating terms?

- •Hotel & Leisure Margins: Monitor quarterly earnings to see if the hotel division’s growth can continue to offset the TR slump. Pay attention to occupancy rates and revenue per available room (RevPAR).

- •New Business Progress: Look for capital allocation announcements and project milestones related to integrated resorts or other new ventures. This is a key indicator of their long-term growth strategy. (Read more about diversification strategies in hospitality).

- •Macroeconomic Indicators: Keep an eye on currency exchange rates (especially USD/KRW), as a 5% change can impact pre-tax profit by ~KRW 3.9 billion. Interest rates and international travel recovery data are also crucial.

In conclusion, while the Macau exit is a short-term blow, it may prove to be a necessary step in Hotel Shilla’s evolution. The company’s future success will depend on its ability to streamline its duty-free operations while successfully cultivating its robust hotel business and new strategic initiatives.