The upcoming Hotel Shilla IR Analysis on September 30, 2025, represents a critical juncture for investors. As the company navigates a complex economic landscape, this event will shine a spotlight on its diverging fortunes: the persistent struggles in its core duty-free business and the promising growth in its Hotels & Leisure division. This deep-dive analysis unpacks the key fundamentals, market pressures, and strategic questions that will define the Hotel Shilla stock outlook for the foreseeable future.

This investor relations event is more than a standard corporate briefing; it’s a litmus test for Hotel Shilla’s resilience and strategic vision. The market will be listening intently for a clear roadmap to profitability and sustainable growth.

The Event: What Investors Need to Know

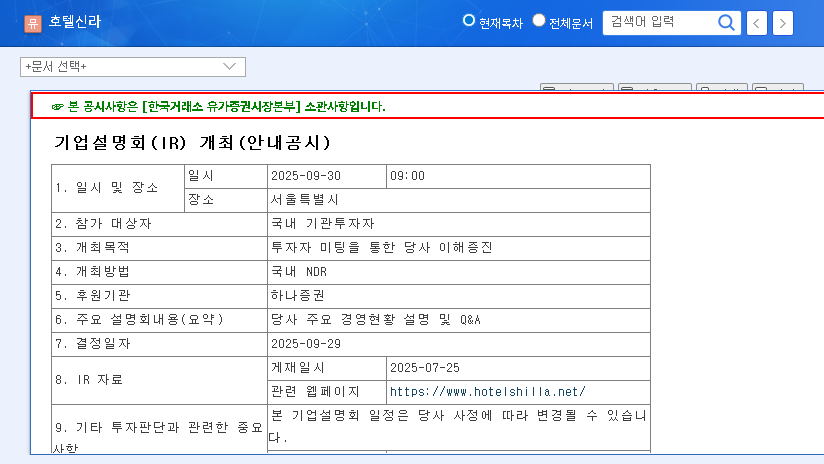

Hotel Shilla has scheduled its corporate investor relations briefing to enhance transparency and communicate its strategic direction. The key details are as follows:

- •Date: September 30, 2025

- •Time: 09:00 AM (KST)

- •Agenda: A comprehensive review of key management status, divisional performance, and an open Q&A session.

- •Official Disclosure: The preliminary details can be reviewed in the official filing. (Source: DART)

A Tale of Two Divisions: Analyzing Performance

The core of the Hotel Shilla IR Analysis lies in understanding the stark contrast between its two main business segments. This duality is central to its current valuation and future potential.

The Duty-Free Business (TR Division): Navigating Headwinds

The TR Division, long the company’s flagship, is facing significant challenges. The first half of the fiscal year saw sales dip to KRW 1.69 trillion and an operating loss of KRW 19.8 billion. This isn’t a temporary blip but a result of several converging factors:

- •Slow Tourism Recovery: While travel is resuming, the volume and spending patterns of key demographics, particularly Chinese tourists, have not returned to pre-pandemic levels.

- •Economic Pressures: A rising USD/KRW exchange rate diminishes the price advantage of Korean duty-free shops, while global inflation curbs discretionary spending.

- •Structural Shifts: The reliance on ‘daigou’ (Chinese resellers) has become less profitable due to regulatory changes and increased competition, as noted by industry analysts at sources like Reuters.

Investors will demand a concrete, actionable strategy to reverse this trend. Vague promises will not be sufficient to restore confidence in this critical duty-free business segment.

The Hotels & Leisure Division: A Beacon of Growth

In stark contrast, the Hotels & Leisure division is thriving. With first-half sales of KRW 341 billion and an operating profit of KRW 22.6 billion, this segment demonstrates robust health. The post-endemic travel boom, coupled with a successful strategy of expanding its property portfolio, has fueled this growth. Furthermore, the company’s exploration into new ventures like comprehensive resorts, condominiums, and even premium elderly care facilities signals a forward-thinking approach to diversification and securing new revenue streams. This proactive strategy is a key positive factor for the overall Hotel Shilla stock narrative.

Financial Health & Macroeconomic Risks

While the balance sheet appears sound with a healthy debt-to-equity ratio of 58.65%, the negative diluted EPS of -KRW 187 is a red flag, indicating a net loss on a per-share basis. The company is also highly exposed to macroeconomic volatility. Rising interest rates increase debt servicing costs, while high oil prices inflate logistics and operational expenses. The IR presentation must address how management plans to navigate these external financial risks effectively.

Action Plan for Investors: Key IR Focus Points

To make an informed decision, investors should scrutinize the IR for clear answers to the following critical questions. This is the core of a useful Hotel Shilla IR analysis.

- •TR Turnaround Plan: What specific, measurable steps will be taken to improve duty-free profitability beyond simply waiting for tourism to recover?

- •Leisure Growth Acceleration: How will the company capitalize on the Hotels & Leisure division’s momentum? What are the timelines and expected ROI for new ventures?

- •Financial Risk Management: How is the company hedging against currency fluctuations and preparing for a prolonged high-interest-rate environment?

The clarity and conviction of the answers provided will likely determine the short-to-medium term trajectory of the Hotel Shilla stock price. A compelling vision that balances the recovery of the old with the growth of the new could unlock significant shareholder value. For more on the market dynamics, consider our analysis on the Future of Korean Hospitality.