JS Corporation Q3 Earnings: A Deceptive Victory?

The latest preliminary JS Corporation Q3 earnings report for 2025 has captured the market’s attention, presenting a complex picture for investors. With headline figures like revenue and operating profit impressively surpassing market consensus, a wave of initial optimism is understandable. However, a deeper dive into the numbers reveals potential pitfalls, most notably a sharp year-on-year decline in net income. This comprehensive JS Corporation financial analysis will dissect the results, explore the underlying fundamentals, and provide a clear-eyed view to help you make an informed investment decision.

The headline numbers paint a picture of success, but the footnotes reveal a story of caution. Understanding the disconnect between operating profit and net income is the key to evaluating JS Corporation’s true health.

The Q3 2025 Preliminary Earnings: By the Numbers

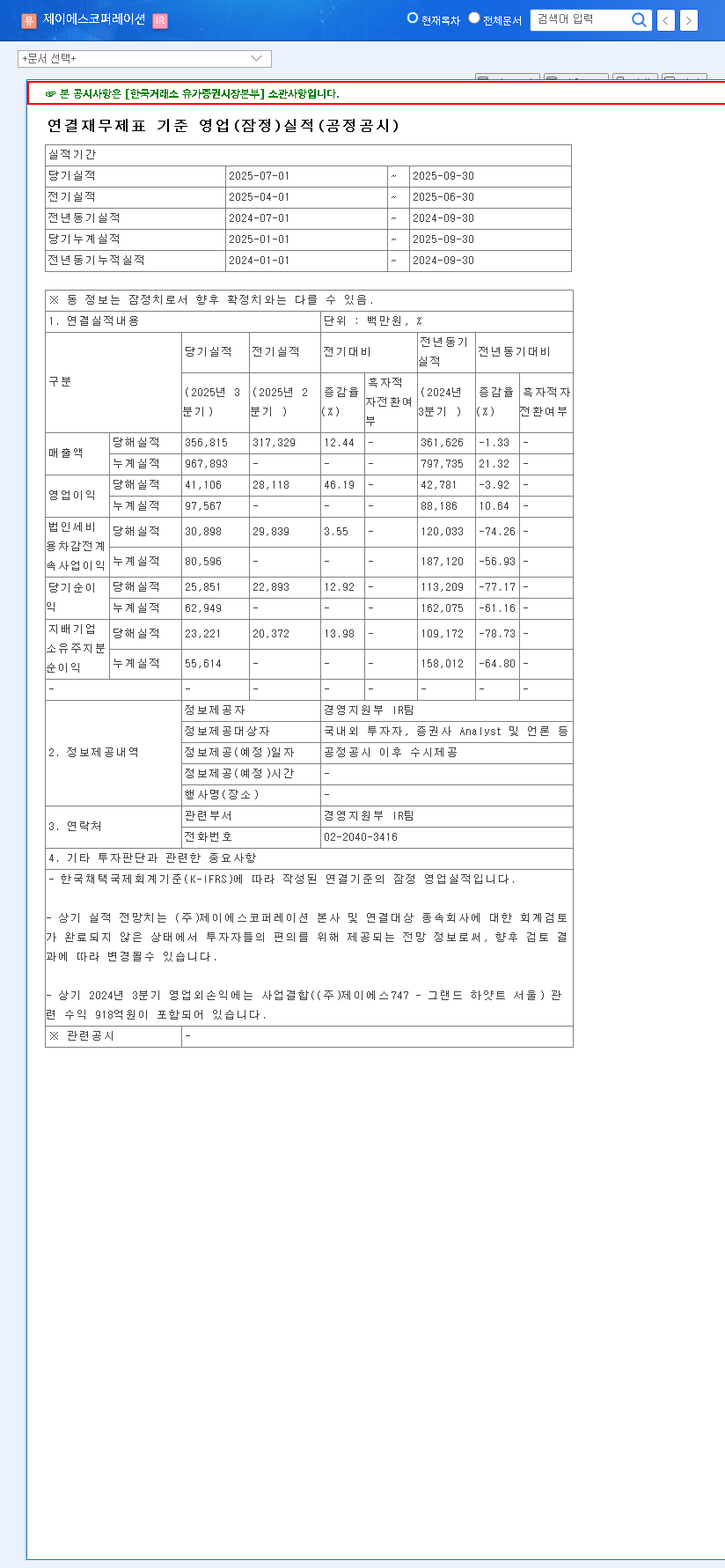

On October 30, 2025, JS Corporation released its preliminary consolidated earnings, showcasing a beat on top-line metrics but raising questions on the bottom line. While these figures represent a sequential improvement from the previous quarter, they tell a different story when compared to the same period last year.

- •Revenue: KRW 356.8 billion, exceeding market forecasts.

- •Operating Profit: KRW 41.1 billion, a solid 12% above market estimates.

- •Net Income: KRW 23.2 billion, marking a significant and concerning decrease from Q3 2024’s KRW 113.2 billion.

Fundamental & Financial Health Analysis

To understand this divergence, we must analyze the performance of its core business segments and the company’s overall financial standing. The JS Corp stock analysis depends heavily on these underlying factors.

Performance by Business Segment

- •Handbag & Apparel Manufacturing: The handbag division remains a pillar of strength, leveraging its order-based production model and strong ODM relationships with global brands. However, the apparel segment is facing headwinds, with sluggish sales attributed to reduced orders from key buyers, reflecting broader consumer spending trends.

- •Hotel Business: This segment is a bright spot, benefiting from the global tourism recovery. Increased occupancy and revenue are positive drivers, but this success is tempered by the looming risk of significant capital expenditure needed for renovating aging facilities.

Key Financial Metrics and Risks

The improved operating profit margin is a testament to either stronger pricing power or efficient cost management—a positive signal of operational resilience. However, the drastic drop in net income demands scrutiny. This could stem from one-time costs, higher interest expenses due to recent convertible bond issuances, or other non-operating factors. A major red flag is the high consolidated debt-to-equity ratio of 243%. Such high leverage increases financial risk, especially in a rising interest rate environment, and requires diligent monitoring. For a deeper understanding of such metrics, investors can review guides on how to analyze a company’s balance sheet.

Forward Outlook: Positive Catalysts vs. Negative Headwinds

Potential Positives

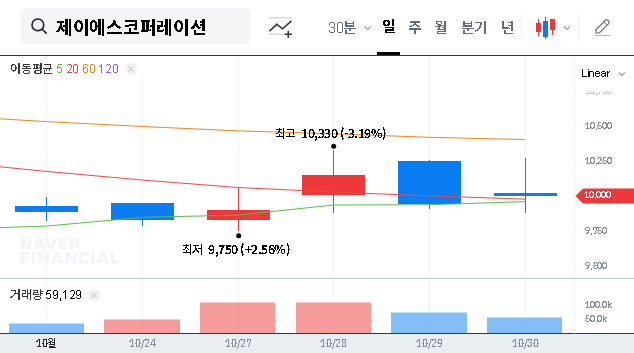

The surprise beat in revenue and operating profit can generate positive short-term stock momentum. The recovery in the hotel business provides a solid growth engine, and the strong US dollar trend, as reported by sources like Bloomberg, could boost margins for the export-heavy manufacturing segments. This confirmed profitability resilience showcases management’s ability to navigate a challenging environment effectively.

Significant Risks and Concerns

The primary concern is the steep decline in net income, which questions the quality of the earnings and could erode investor confidence. The persistent investment risk assessment must highlight the high debt ratio as a long-term burden on corporate valuation. Furthermore, the slump in the apparel division and the potential for macroeconomic volatility (e.g., oil prices, freight costs) pose ongoing threats to the company’s stability and growth trajectory.

Investor Action Plan & Recommendations

Given the mixed signals from the JS Corporation Q3 earnings, a cautious ‘Neutral’ stance is advisable. Prudent investors should move beyond the headlines and focus on the following due diligence before making any decisions:

- •Analyze the Official Filing: The preliminary report is just a snapshot. A thorough review of the detailed financial statements is critical. You can access the Official Disclosure (DART report) to understand the precise causes of the net income decline.

- •Monitor Debt Management: Watch for concrete steps and strategic plans from management aimed at reducing the high debt ratio and strengthening the company’s financial structure.

- •Evaluate Core Business Strategy: Assess the outlook for the apparel segment’s recovery and look for evidence of new growth drivers beyond the current business lines to ensure long-term sustainability.

- •Listen to the Earnings Call: Pay close attention to management’s commentary during the investor conference call for qualitative insights, future guidance, and their tone regarding the challenges ahead.

Ultimately, investing in JS Corporation requires a long-term perspective focused on fundamental improvements and risk mitigation, rather than being swayed by short-term market reactions to a deceptive earnings beat.