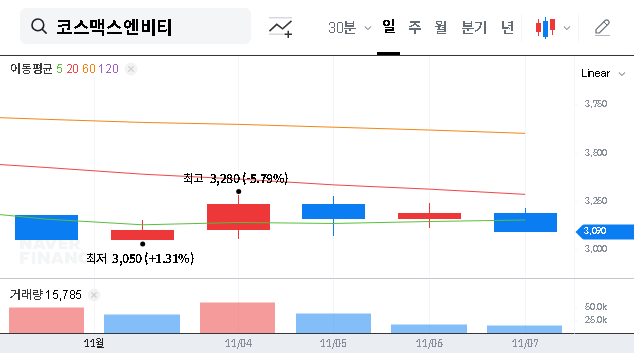

The latest COSMAX NBT, INC. earnings report for Q3 2025 has sent a shockwave through the investment community. As a leading health functional food OEM/ODM manufacturer, the company’s preliminary results, released on November 7, 2025, revealed a performance that significantly missed market consensus. This isn’t merely a minor setback; it raises critical questions about the company’s operational competitiveness, financial stability, and future growth trajectory. This in-depth COSMAX NBT analysis will dissect the numbers, explore the underlying causes, and provide a clear, actionable strategy for current and potential investors navigating this turbulence.

With profitability plummeting and financial risks mounting, understanding the full picture of the Q3 2025 COSMAX NBT, INC. earnings is no longer optional—it’s essential for prudent investment decisions.

Deconstructing the Q3 2025 Earnings Miss

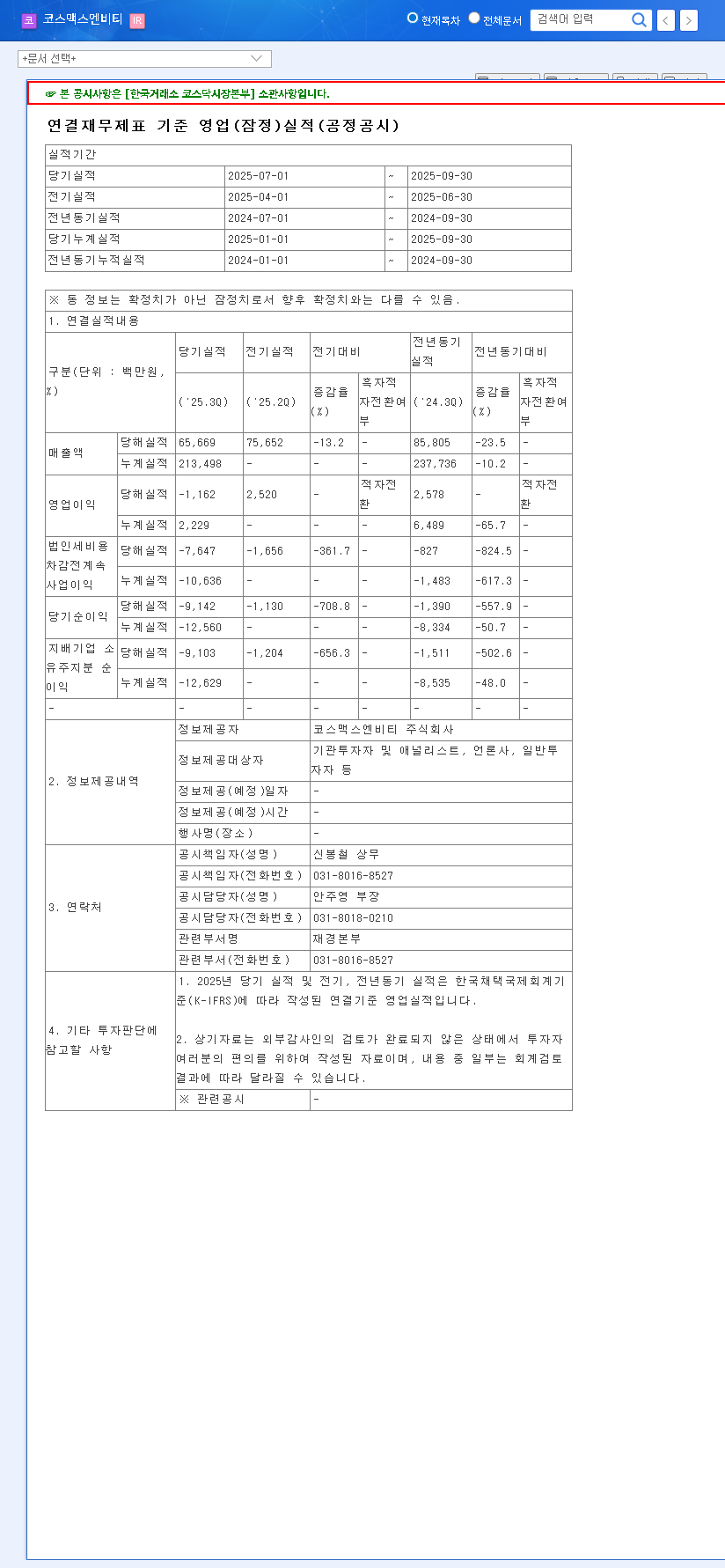

The official preliminary consolidated financial results, which can be viewed in the Official Disclosure on DART, painted a stark picture. The deviation from market expectations was not subtle, highlighting a severe operational disruption. Let’s break down the key figures:

- •Revenue: Reported at KRW 65.7 billion, a staggering 17% below the market estimate of KRW 79.1 billion.

- •Operating Profit: A loss of KRW -1.2 billion, which is 135% below the consensus forecast for a KRW 3.4 billion profit.

- •Net Profit: The most alarming figure, a net loss of KRW -9.1 billion, representing a shocking 3133% miss compared to the expected KRW 0.3 billion profit.

This sharp reversal into a significant loss, especially after a promising turnaround to profitability in Q2, indicates escalating earnings volatility and deep-seated structural issues that a single positive quarter could not resolve.

Core Factors Driving the Disappointing Performance

This poor showing is not a one-off event but the result of a confluence of negative factors. Understanding these drivers is key to assessing the future of the COSMAX NBT stock.

1. Revenue Erosion and Severe Profitability Decline

The 17% revenue miss signals significant challenges in business expansion and penetrating new markets. Compounding this, the company’s high dependency on overseas revenue (65.47%) has become a double-edged sword. The continued strength of the USD and EUR against the Korean Won has led to substantial foreign exchange-related valuation losses, severely eroding profitability. Furthermore, global inflationary pressures, including rising oil prices and shipping costs, have inflated production costs, squeezing margins from all sides.

2. The Crushing Weight of a High Financial Burden

As of H1 2025, COSMAX NBT’s debt-to-equity ratio stood at an alarming 359.10%. In the current high-interest-rate environment, this massive debt load translates into crippling interest payments, which directly consume any potential profits. This high leverage not only deepens profitability issues but also heightens liquidity risk, making financial restructuring an urgent priority. Investors can learn more about how to analyze a company’s financial health in our related guide.

3. Navigating a Mature and Saturated Domestic Market

The domestic health functional food market in Korea is showing signs of maturation, having contracted by 1.7% in 2024. While a shift towards personalized nutrition presents new opportunities, the slowdown in overall market growth makes it increasingly difficult for established players like COSMAX NBT to find new avenues for substantial expansion. Increased competition for a shrinking pie adds another layer of pressure.

Outlook for COSMAX NBT Stock and Investor Sentiment

The immediate fallout from this earnings report will undoubtedly be negative for the COSMAX NBT stock price. According to market analysis from sources like Reuters, such a significant earnings miss typically leads to a sharp sell-off as investor confidence is shaken. We can expect strong downward pressure on the stock in the short term. The mid-to-long-term outlook depends entirely on the company’s response. Without a clear and convincing turnaround plan, investor sentiment is likely to remain bearish, leading to a prolonged period of stock price stagnation or decline.

A Strategic Playbook for Investors

Given the severity of the Q3 2025 earnings report and the underlying financial concerns, a highly conservative and cautious approach is warranted. Prematurely buying the dip could be a costly mistake. Instead, investors should adopt a wait-and-see strategy focused on the following key areas:

- •Demand for Transparency: The management must provide a clear, detailed explanation for the earnings collapse, going beyond surface-level excuses.

- •Scrutinize Turnaround Plans: Look for concrete, measurable plans for cost management, FX hedging strategies, and, most importantly, a specific roadmap to reduce the high debt ratio and improve the financial structure.

- •Monitor Growth Initiatives: Keep a close watch on any new raw material developments or overseas market expansion efforts for tangible signs of progress and revenue generation.

In conclusion, the latest COSMAX NBT, INC. earnings report is a clear red flag. Until the company demonstrates a credible path to recovery with visible results, investors are advised to remain on the sidelines. The risk currently outweighs the potential reward, making caution the most valuable asset.