The Prestige BioPharma Teva deal has sent ripples through the biotech investment community. For a company navigating financial headwinds, this partnership with a global pharmaceutical giant marks a pivotal moment. Prestige BioPharma Limited, a developer specializing in biosimilars, has officially announced a supply agreement with Teva Pharmaceuticals, facilitating its long-awaited entry into the lucrative European market. But what does a short-term, KRW 1.2 billion contract truly signify for the company’s future and its stock price? This comprehensive analysis will dissect the agreement, evaluate the underlying financials, and provide a strategic outlook for investors considering Prestige BioPharma stock.

While this deal is a significant validation of Prestige BioPharma’s commercialization strategy for Tuznue, investors must weigh this short-term victory against the company’s persistent long-term financial challenges. Prudence and continuous monitoring are key.

Breaking Down the Prestige BioPharma Teva Deal

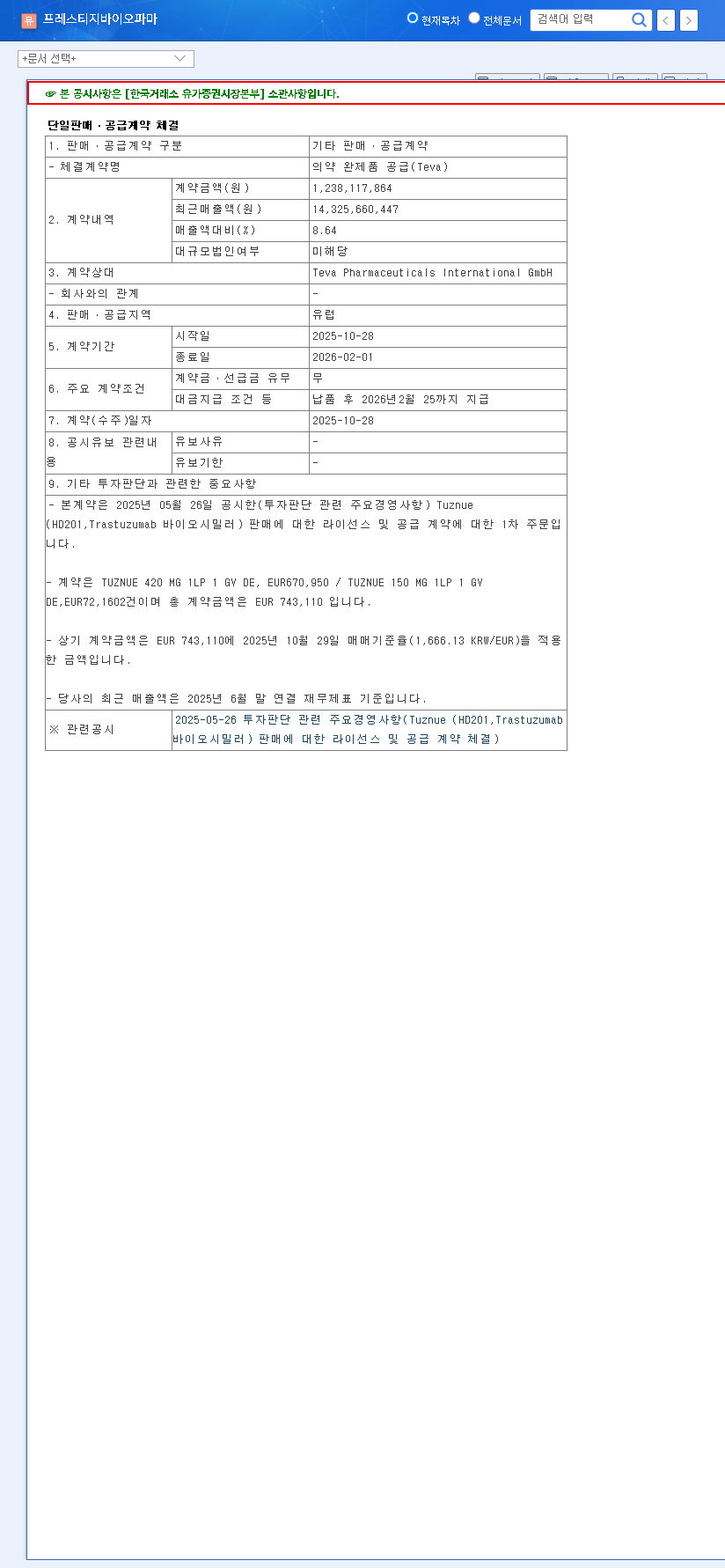

Prestige BioPharma has confirmed a single-product sales and supply agreement with Teva Pharmaceuticals International GmbH. This contract focuses on supplying finished pharmaceutical products to the European market, a critical step for the company’s flagship biosimilar. Here are the core details of the announcement, which can be verified in the Official Disclosure (DART).

- •Contracting Party: Teva Pharmaceuticals International GmbH

- •Contract Value: KRW 1.2 billion (approx. 8.64% of recent sales revenue)

- •Product: Finished Pharmaceutical Products (Tuznue – HD201)

- •Supply Region: Europe

- •Contract Period: A short-term, three-month window from October 28, 2025, to February 1, 2026.

Investment Analysis: The Bull vs. Bear Case

This deal presents a classic duality for investors. On one hand, it’s a monumental step forward; on the other, it doesn’t erase the underlying financial risks. A thorough biosimilar investment analysis requires looking at both sides.

The Bull Case: A Gateway to Commercial Success

The positive signals from this agreement are clear and compelling. The successful marketing authorization for Tuznue in Europe is now being actualized. Tuznue (HD201) is a biosimilar for Herceptin (trastuzumab), a widely used breast cancer treatment, representing a massive market opportunity. Partnering with a distributor as established as Teva provides instant credibility and market access that would otherwise take years to build. This move could also create powerful synergies with its growing CDMO (Contract Development and Manufacturing Organization) business, Prestige Biologics, reinforcing its entire operational ecosystem. For more context on biosimilars, you can read the FDA’s official overview.

The Bear Case: Financial Health and Contract Limitations

Despite the positive news, the company’s financial foundation remains a significant concern. Prestige BioPharma has been dealing with persistent operating losses and capital impairment, driven by high R&D costs essential for its pipeline. A high debt ratio adds another layer of financial risk, making the company vulnerable to market volatility and increasing the importance of future fundraising. Furthermore, the contract’s short three-month duration limits its immediate financial impact. It is more of a pilot program than a long-term revenue stream, meaning the market will be watching intently for signs of extension or a larger, more definitive agreement.

Impact on Prestige BioPharma Stock and Future Strategy

The announcement is likely to provide a short-term boost to Prestige BioPharma stock, as it validates the commercial potential of its key asset, HD201. However, the market’s reaction will likely be tempered. The KRW 1.2 billion value is not substantial enough to fundamentally alter the company’s financial trajectory on its own. Instead, savvy investors will view this as a ‘show me’ story. The real upside for the stock depends on this deal being the first of many.

Strategically, this is a masterstroke. It’s a low-risk way for Teva to test the market with Tuznue and for Prestige BioPharma to prove its manufacturing and supply chain capabilities. A successful execution of this contract could open doors for deeper collaborations, expanded territories, and partnerships for other drugs in its pipeline. Learn more by reading our guide on how to analyze biotech stocks.

Investor Action Plan & Key Monitoring Points

For current and potential investors, a prudent, watchful approach is recommended. While the Prestige BioPharma Teva deal is unequivocally positive news, it is a single data point. The investment thesis hinges on what comes next. Investors should closely monitor the following developments:

- •Contract Extension: Any news of Teva extending the contract beyond the initial three months would be a major bullish signal.

- •European Sales Data: Tracking the initial sales performance of Tuznue in the European market will be crucial to forecasting long-term revenue.

- •Financial Improvement: Watch for progress in quarterly reports on reducing operating losses and improving the company’s balance sheet.

- •Global Expansion: Keep an eye on the progress of the US FDA approval process for Tuznue, which is the next major catalyst for global market penetration.

In conclusion, this agreement is a significant achievement that moves Prestige BioPharma from a development-stage company to a commercial-stage one. It provides positive momentum, but the journey towards sustainable profitability requires continued execution and financial discipline. The coming months will be critical in determining if this deal is the start of a major turnaround or merely a brief positive interlude.