The latest HD HYUNDAI Q3 earnings report for 2025 has unveiled a complex and contradictory financial narrative that has captured the attention of the market. While the company delivered a robust ‘earnings surprise’ with impressive top-line growth, a severe ‘earnings shock’ in its bottom line has left investors seeking clarity. This deep-dive analysis unpacks the provisional results, examines the fundamentals of each business segment, and provides a forward-looking investment outlook on HD HYUNDAI’s trajectory.

We will explore the specific drivers behind this paradoxical performance, providing a comprehensive view for anyone conducting an HD HYUNDAI stock analysis or following its financial results.

The Core Paradox: Decoding the HD HYUNDAI Q3 2025 Report

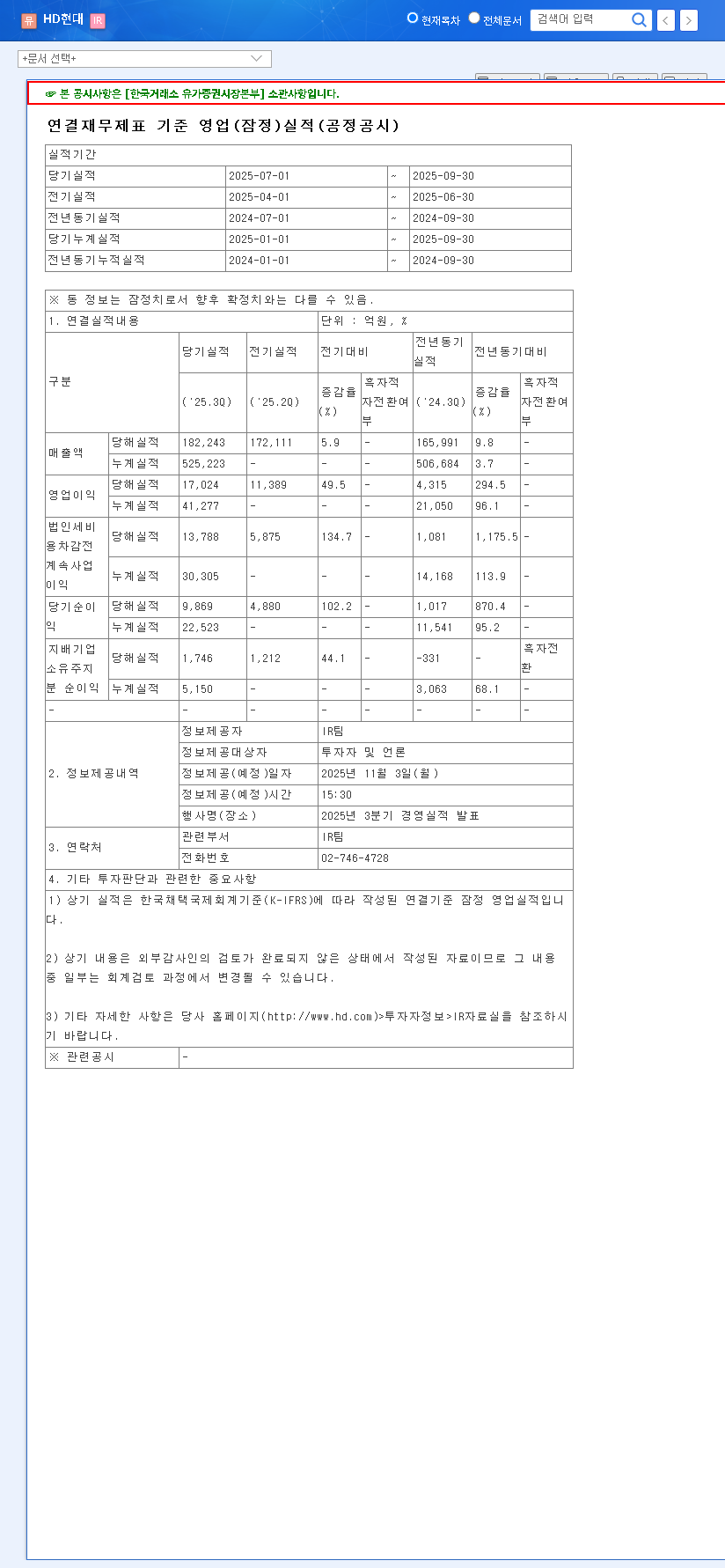

According to the company’s Official Disclosure, HD HYUNDAI CO.,LTD. announced impressive provisional figures for Q3 2025. The company reported a consolidated revenue of KRW 18.22 trillion and an operating profit of KRW 1.70 trillion. These figures decisively surpassed market consensus estimates compiled by sources like Reuters, exceeding revenue forecasts by 7% and operating profit by a remarkable 16%.

The central story of the HD HYUNDAI Q3 earnings is one of operational strength clashing with financial volatility. While the core businesses demonstrated robust health, external and non-recurring factors dealt a significant blow to the net income, creating a tale of two very different financial outcomes.

However, this top-line success was severely undercut by the net income figures. At just KRW 174.6 billion, net income fell short of market expectations by a staggering 84% and represented a 65% plunge from the previous quarter. This dramatic drop was attributed to a confluence of one-off expenses and financial market headwinds.

What Drove the Strong Revenue and Operating Profit?

- •Diversified Portfolio Strength: Robust performance and solid demand across key segments, including shipbuilding, marine services, refining, and construction machinery, fueled top-line growth.

- •Enhanced Operational Efficiency: Disciplined cost-saving initiatives, improved productivity, and a strategic focus on high-value-added products significantly boosted operating margins.

Why Did Net Income Plummet?

- •Foreign Exchange Losses: Significant volatility in global currency markets led to substantial foreign exchange-related losses, directly impacting profitability.

- •Investment Valuation Losses: The company recorded valuation losses on its financial investment assets and experienced a decline in the value of its equity investments in associate companies.

- •One-Off Costs: Although not fully detailed, the report indicated the presence of unexpected, non-recurring expenses that negatively affected the bottom line.

Segment-by-Segment Performance Analysis

A detailed look at the HD HYUNDAI financial results reveals varying dynamics across its core business units.

Shipbuilding & Marine Segment

This division remains a key growth engine, benefiting from strong global demand for eco-friendly vessels. The robust order backlog for high-value ships like LNG carriers provides excellent revenue visibility. However, a potential slowdown in new orders and global economic headwinds pose medium-term risks.

Refining Segment (HD Hyundai Oilbank)

The refining business enjoys strong competitiveness due to its scale and efficiency. Short-term performance is buoyed by rising oil prices and healthy refining margins. The primary risks are volatility in oil and currency markets, alongside the long-term structural decline in demand for fossil fuels due to EV adoption.

Electric & Electronic Segment

This segment is well-positioned to capitalize on global electrification and renewable energy trends. Growing demand for smart grids, power equipment, and Energy Storage Systems (ESS) creates significant opportunities, particularly in the US market. The main challenge is intensifying competition in the high-voltage product space.

Construction Machinery Segment

With a high dependency on exports, this division is sensitive to global economic health and currency fluctuations. While the expansion of compact equipment and rental markets is a positive, a slowdown in major markets like China’s real estate sector presents a significant headwind.

Investment Outlook & Strategic Analysis

The HD HYUNDAI Q3 earnings paint a picture of a company with solid operational fundamentals but facing significant short-term financial volatility. For investors, the key is to look past the one-off shock and evaluate the underlying health and future growth prospects of the core businesses. For a deeper understanding, investors may want to review our guide on How to Analyze Industrial Sector Stocks.

Investment Opinion: Neutral

While the core business strength is undeniable, the net income miss introduces uncertainty that warrants a neutral stance. The market will be closely watching for a recovery in financial stability in the coming quarters. The negative impact on the stock price is likely to be contained if the company can demonstrate that these financial losses were indeed temporary.

Key Monitoring Points for Investors:

- •Q4 Earnings Recovery: The most critical factor will be the resolution of one-off costs and a return to net income stability in the fourth quarter.

- •Macroeconomic Management: How effectively the company mitigates risks from currency and oil price volatility.

- •Eco-Friendly Transition: Progress and profitability in new growth areas like sustainable energy and digital marine solutions.