The latest HD Hyundai Construction Equipment earnings report for Q3 2025, released on October 29, 2025, sent a shockwave of optimism through the market. In an environment filled with economic uncertainty, the company delivered a staggering ‘earnings surprise,’ dramatically outperforming analyst consensus across all key financial metrics. This report isn’t just a set of numbers; it’s a powerful statement about the company’s resilience, strategic execution, and improving position within the global construction equipment market.

In this comprehensive analysis, we will dissect the factors that powered this remarkable performance, explore the underlying market dynamics, and provide a detailed outlook on what this means for the HD Hyundai Construction Equipment stock and potential investors.

Unpacking the Q3 2025 ‘Earnings Surprise’

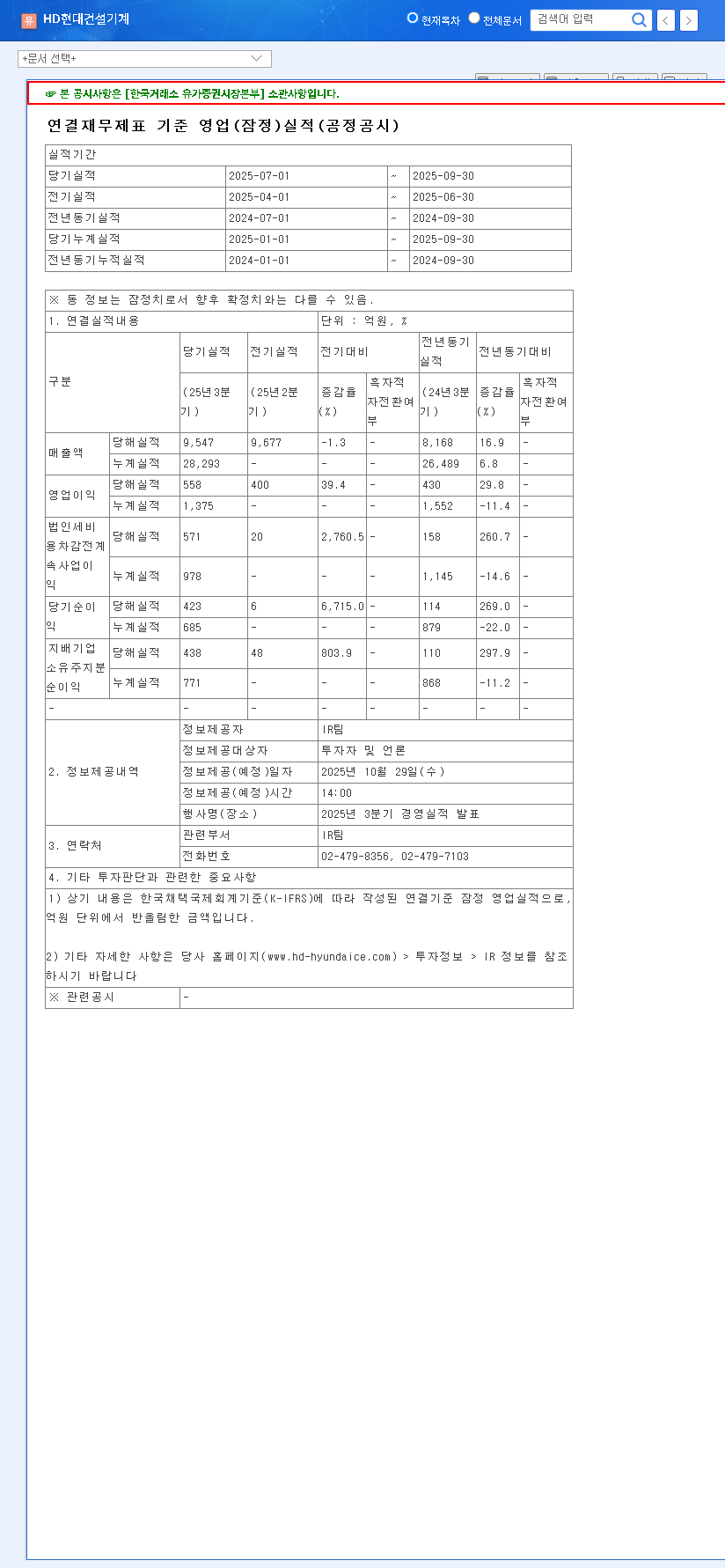

The provisional results for Q3 2025 showcased exceptional growth and profitability that left market expectations far behind. The official numbers highlight a company firing on all cylinders. (Source: Official DART Disclosure)

The sheer magnitude of the outperformance, especially in net income, signals a dramatic improvement in operational efficiency and profitability, catching many analysts by surprise.

- •Revenue: KRW 954.7 billion, a significant 7% above the expected KRW 893.8 billion.

- •Operating Profit: KRW 55.8 billion, soaring an impressive 29% above the consensus estimate of KRW 43.1 billion.

- •Net Income: KRW 43.8 billion, a monumental 80% above the anticipated KRW 24.3 billion.

Key Drivers Behind the Stellar Performance

This outstanding financial report wasn’t a matter of luck. It was the result of several strategic and macroeconomic factors converging to create a perfect storm of profitability.

1. Global Market Recovery and Strategic Sales

After navigating a challenging period, HDHCE has demonstrated a strong turnaround since Q1 2025. The Q3 results confirm that this recovery is accelerating. This is fueled by a gradual but steady rebound in the global construction equipment market, particularly in key regions like North America and emerging economies. The company capitalized on this by deploying aggressive and effective sales and marketing strategies. Furthermore, the significant improvement in operating profit margin points directly to successful cost controls and a strategic shift towards selling more high-margin products, such as advanced excavators and wheel loaders.

2. Favorable Foreign Exchange Tailwinds

With an export ratio hovering around an astonishing 90%, HD Hyundai Construction Equipment is exceptionally sensitive to currency fluctuations. The upward trend of the EUR/KRW and USD/KRW exchange rates during the third quarter provided a substantial boost. A stronger dollar and euro mean that revenue earned in these currencies translates into more Korean Won, directly inflating both the top and bottom lines and contributing significantly to foreign exchange gains.

3. Navigating the Macroeconomic Landscape

While rising oil prices and shipping costs presented potential headwinds, HDHCE’s results show they successfully managed these pressures. The company’s ability to improve margins suggests a strong pricing power or highly efficient cost management that more than offset these inflationary forces. The U.S. Federal Reserve’s decision to hold interest rates also likely provided a stable backdrop for investment sentiment in the sector. For deeper insights into global trends, many investors follow publications like the Financial Times for macroeconomic analysis.

Strategic Outlook and Investor Action Plan

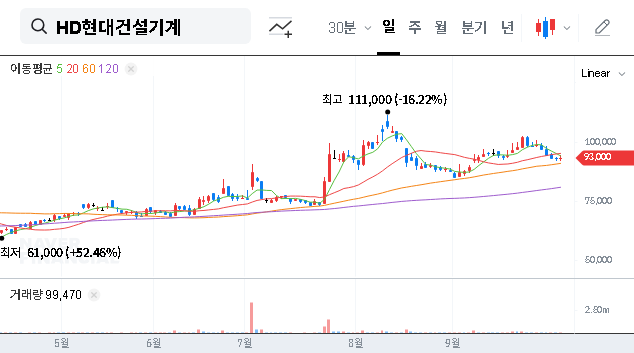

The strong HD Hyundai Construction Equipment earnings for Q3 signal a robust fundamental recovery. This performance is likely to have a positive impact on the stock price in the near term. However, savvy investors should look beyond the headline numbers.

Future Catalysts to Monitor

- •HD Hyundai Infracore Merger: The planned merger remains a key long-term catalyst. Investors are watching closely for updates on the integration process and the realization of expected synergies in R&D, manufacturing, and global sales networks.

- •Technology and ESG Leadership: Continued investment in R&D for next-generation, eco-friendly equipment and a strong ESG (Environmental, Social, and Governance) framework can attract long-term institutional investment and build a sustainable competitive advantage.

- •Market Guidance: The company’s official guidance for Q4 2025 and the full year 2026 will be critical in shaping market expectations and validating the sustainability of this growth trajectory.

In conclusion, HD Hyundai Construction Equipment has delivered a powerful message with its Q3 results, demonstrating a potent combination of operational excellence and favorable market positioning. While the industry is cyclical, as detailed in our detailed analysis of the construction equipment market, the company’s current momentum provides a compelling case for investors looking for exposure to the global industrial recovery. Continuous monitoring of the key catalysts and potential risks will be essential for making informed decisions in this dynamic sector.