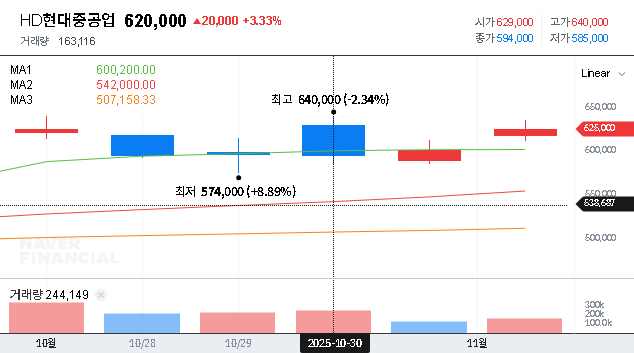

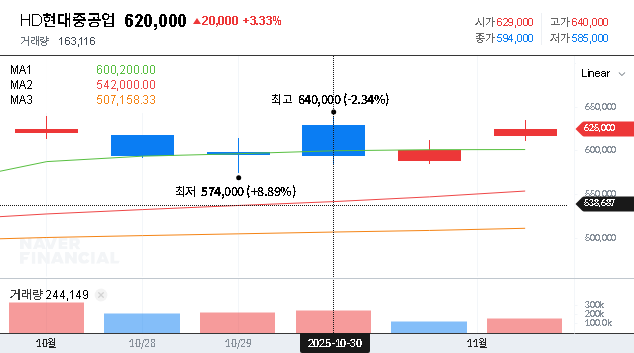

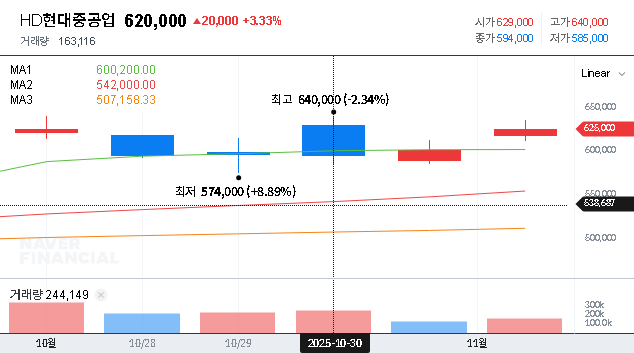

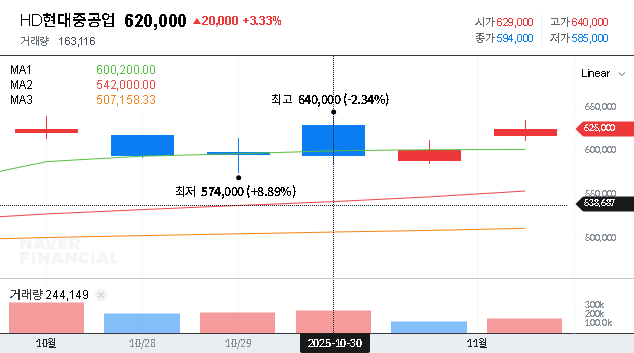

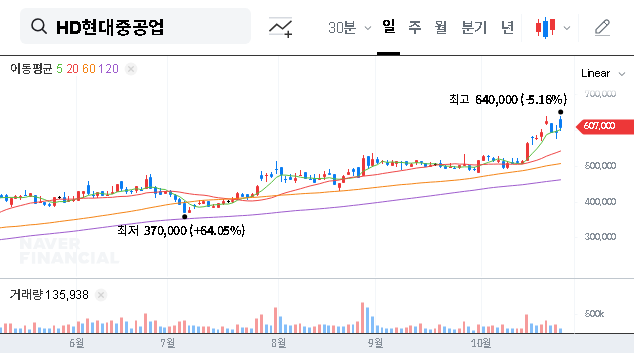

For investors tracking the global shipbuilding industry, HD Hyundai Heavy Industries stock (HD현대중공업) has become a critical focal point. Recent news surrounding negotiations for major eco-friendly vessel orders, coupled with the confirmed acquisition of two Very Large Crude Carrier (VLCC) contracts, has ignited market discussion. This comprehensive investment analysis delves into these developments, examining the company’s Q3 2025 fundamentals and the macroeconomic currents shaping its future. We aim to provide actionable insights for those considering an investment in HD Hyundai Heavy Industries stock.

Catalysts for Growth: Recent Orders and Disclosures

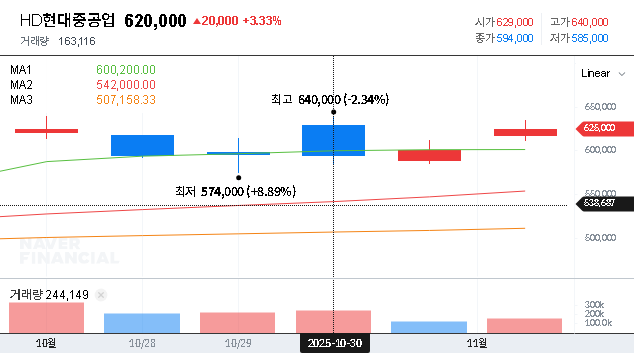

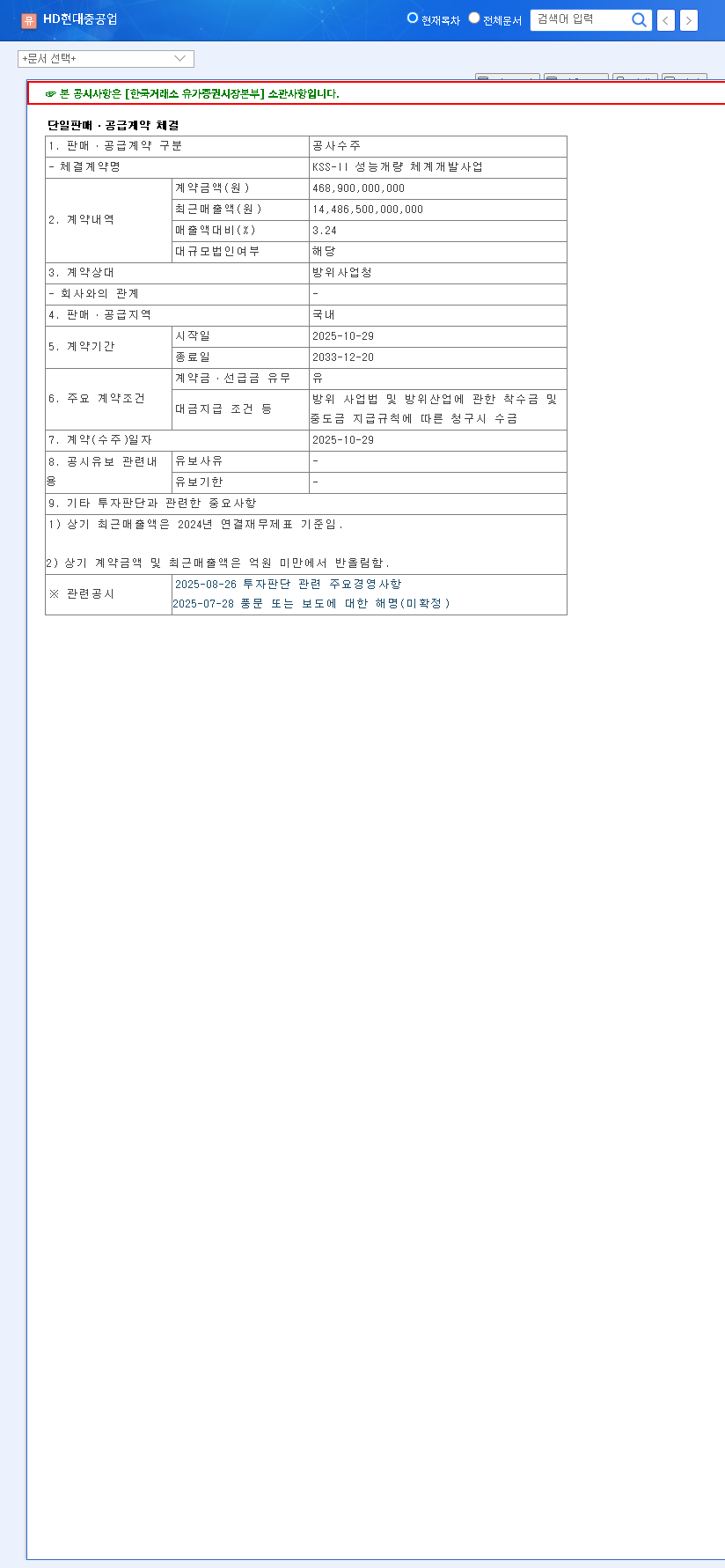

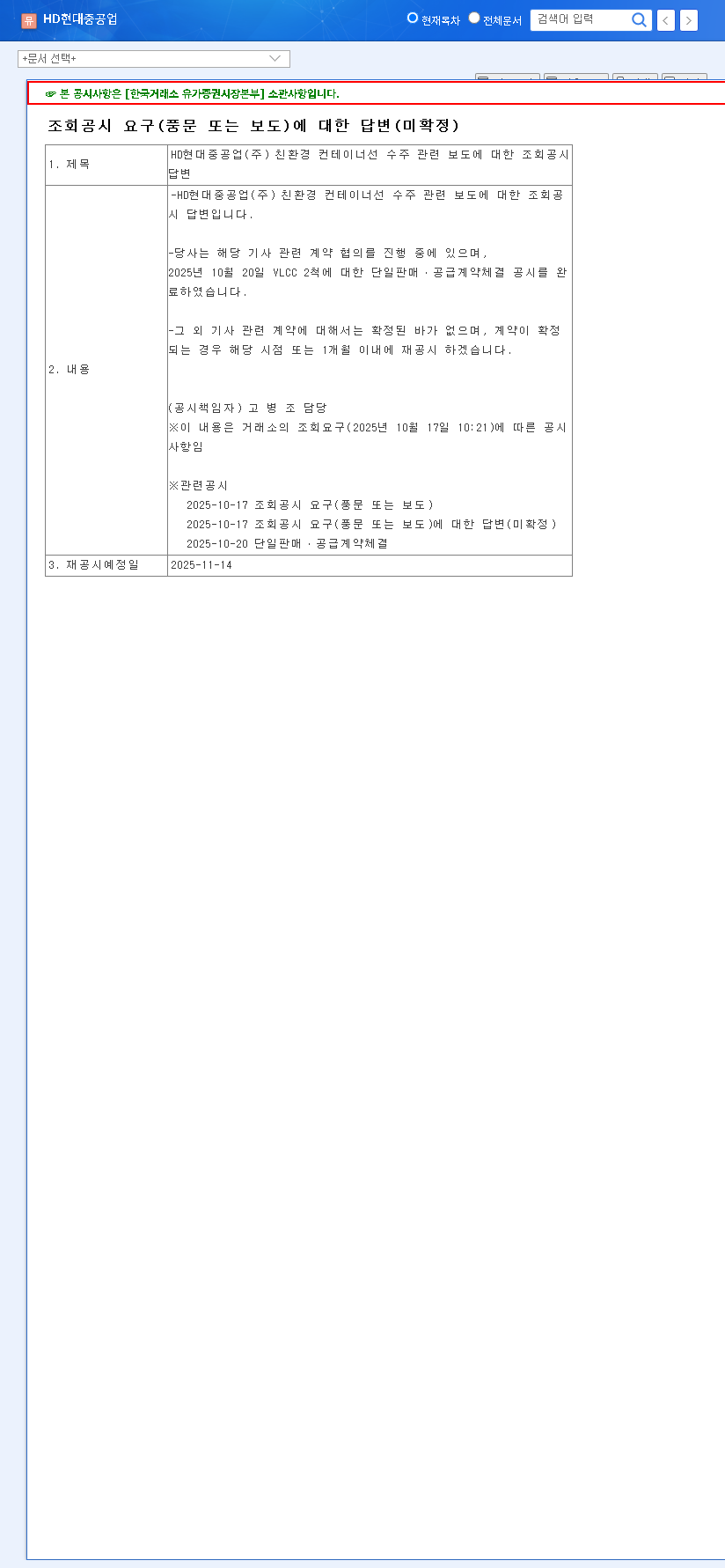

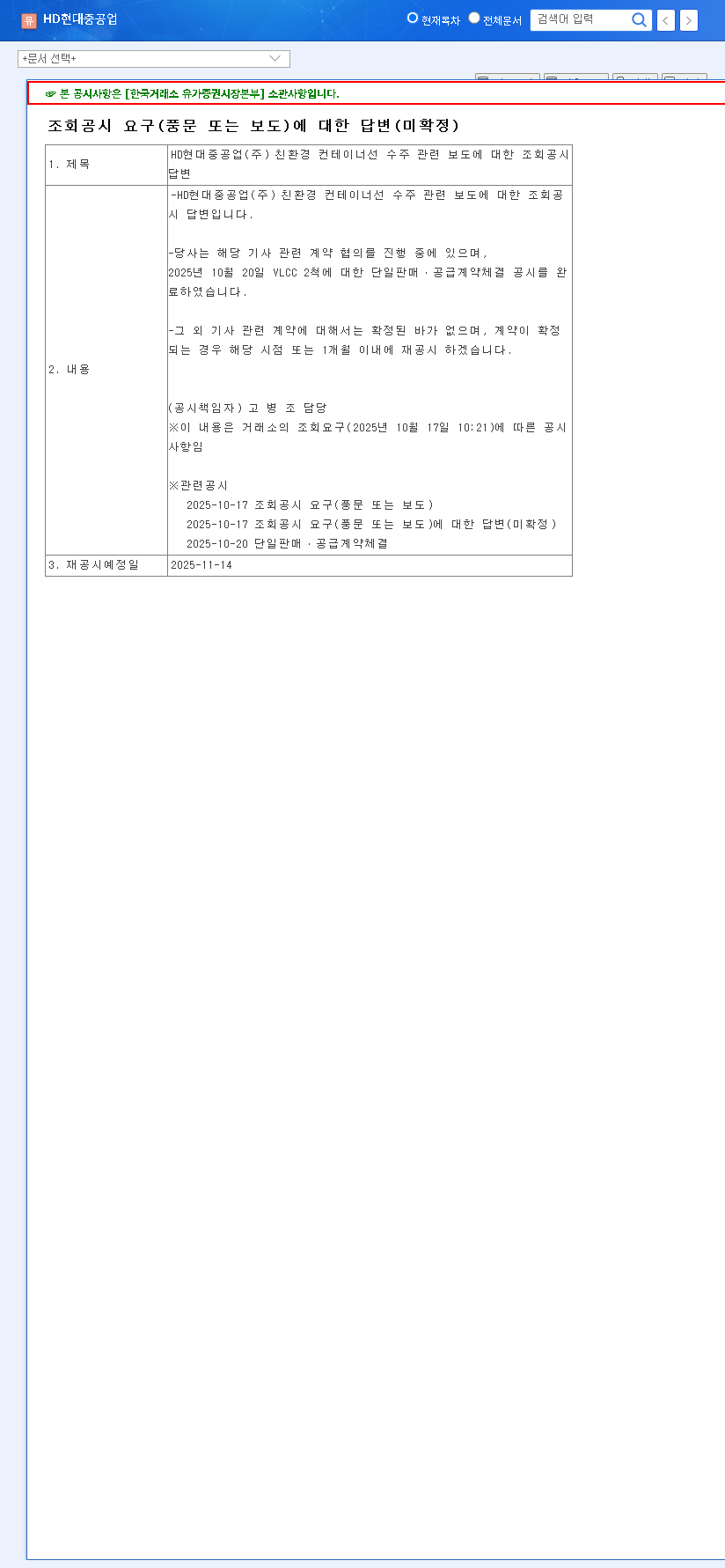

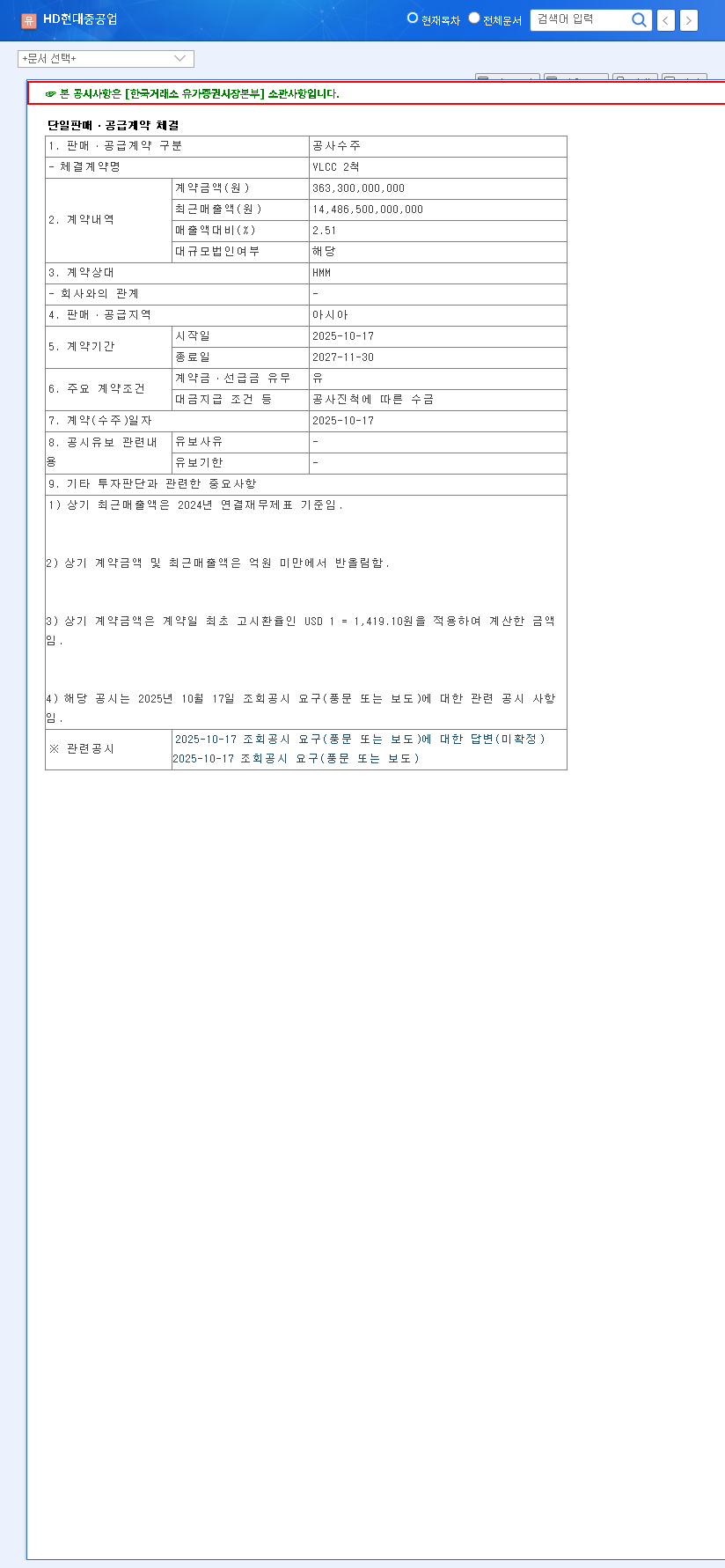

Market attention intensified following two key announcements. On October 17, 2025, the company addressed rumors by confirming active negotiations for a significant order of eco-friendly container ships. This was swiftly followed by an October 20 official disclosure confirming a sales contract for two new VLCCs. These events, detailed in the company’s public filings, signal strong market demand and operational momentum. You can view the Official Disclosure on the DART system for primary source information.

While the VLCC deal is secured, the eco-friendly container ship contract remains under negotiation. The company has committed to a re-disclosure by February 13, 2026, or upon finalization. This pending deal is a major potential catalyst for HD Hyundai Heavy Industries stock, as it would solidify its leadership in the high-value, green-technology vessel market.

The successful negotiation of eco-friendly vessel contracts is not just about revenue; it’s a powerful validation of HHI’s technological edge in a rapidly evolving maritime industry focused on sustainability.

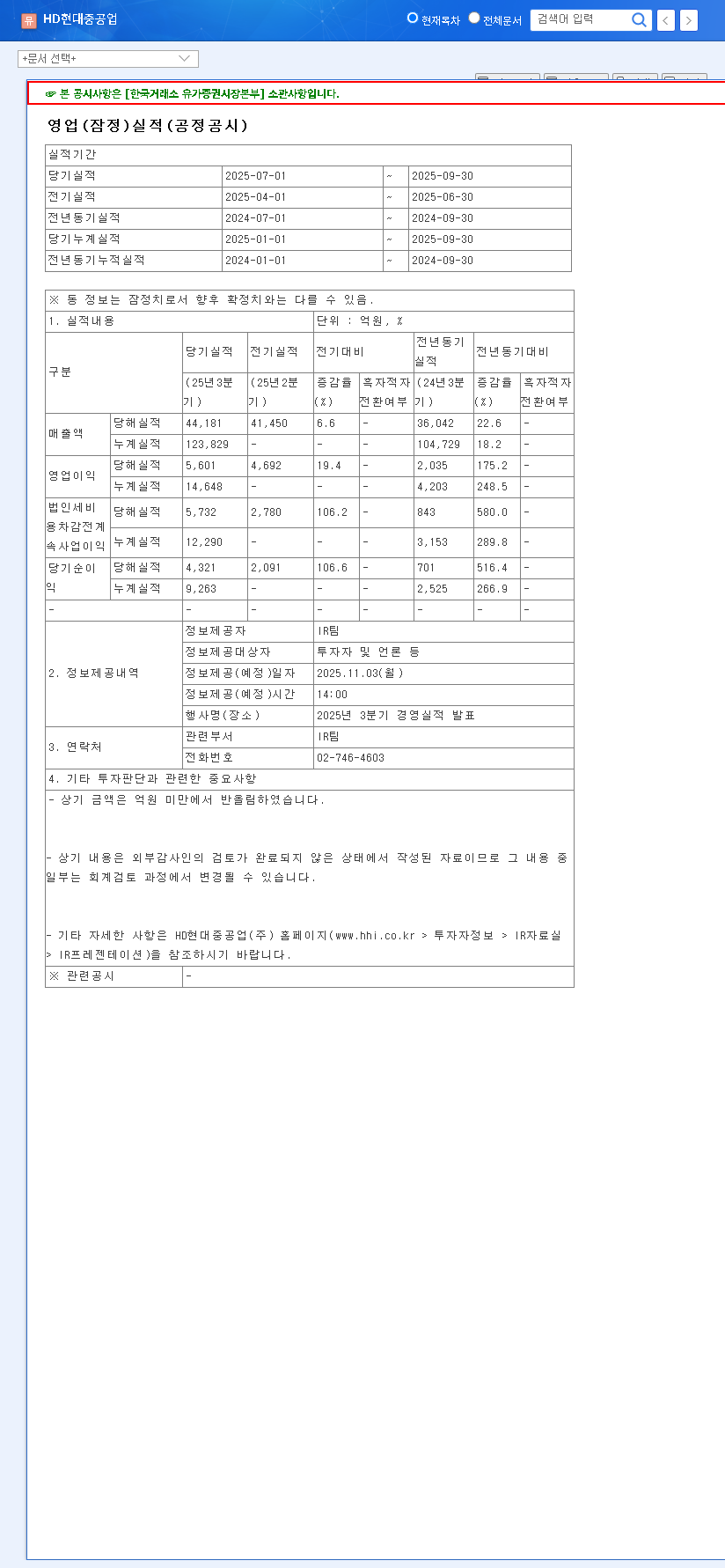

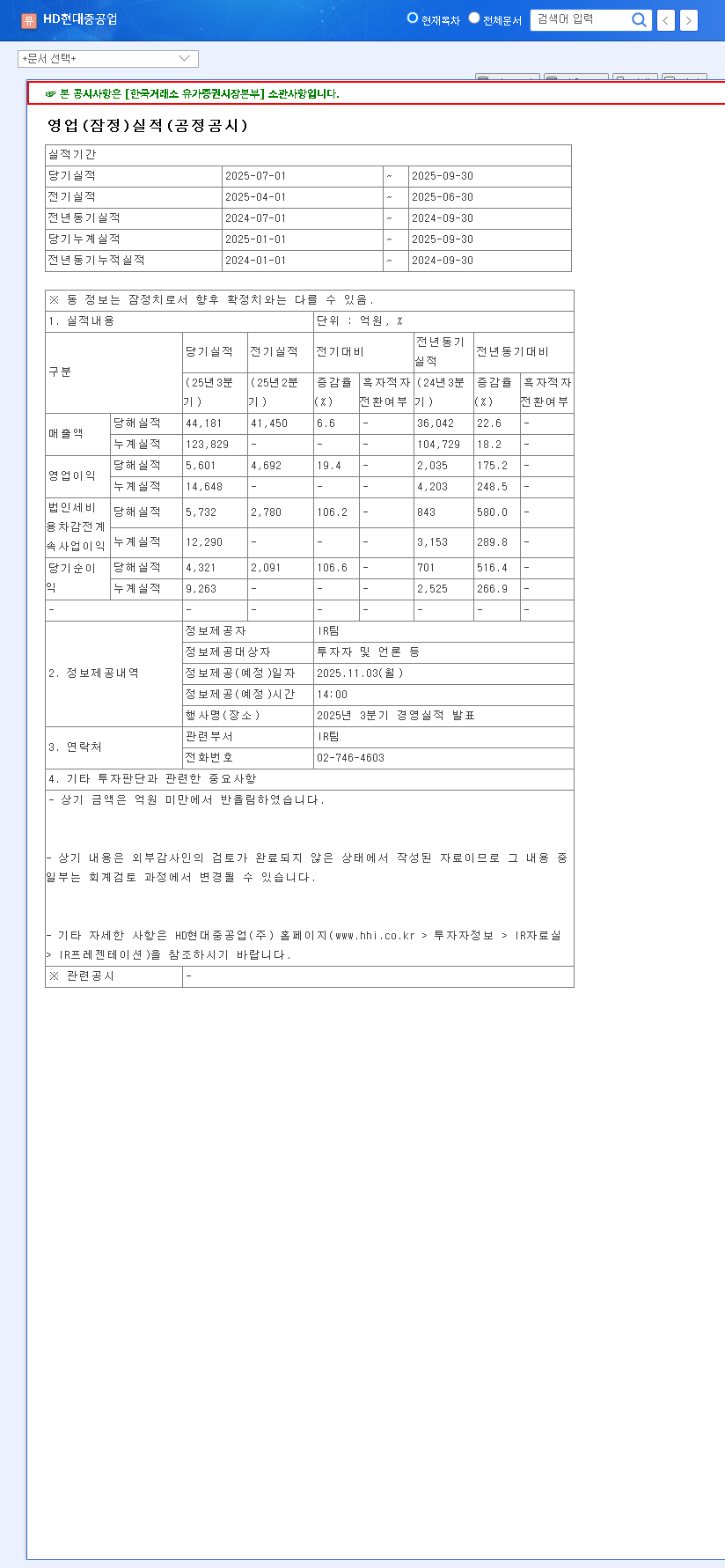

Deep Dive: Q3 2025 Fundamental Analysis

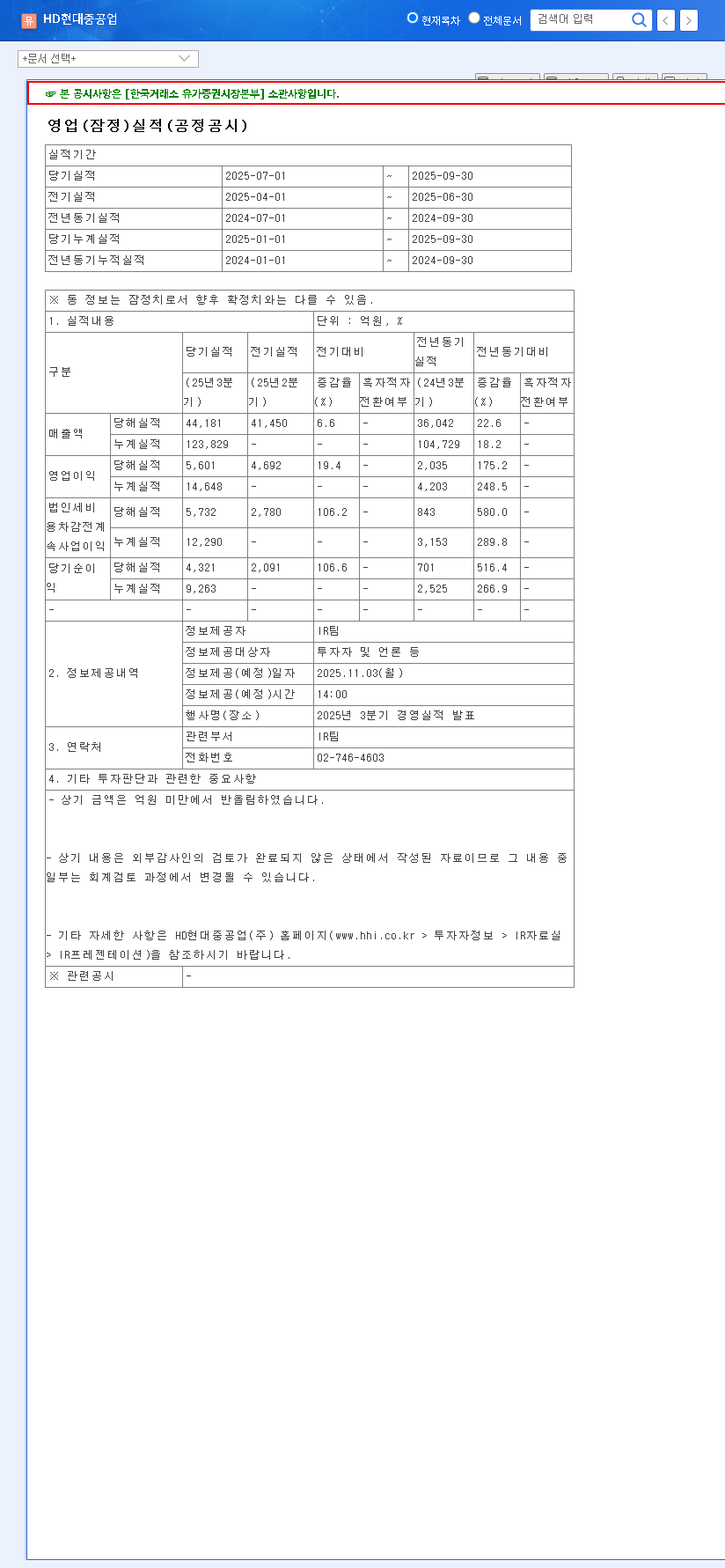

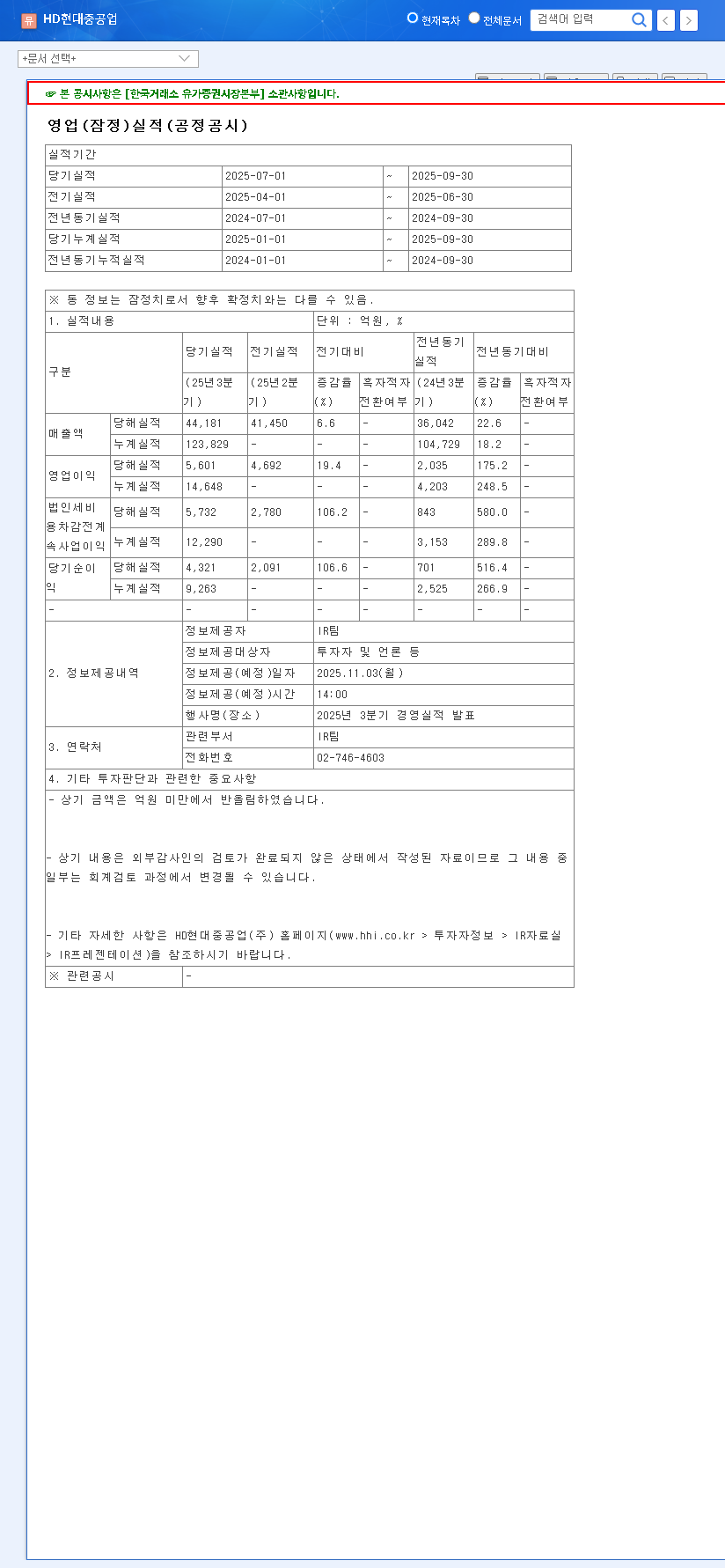

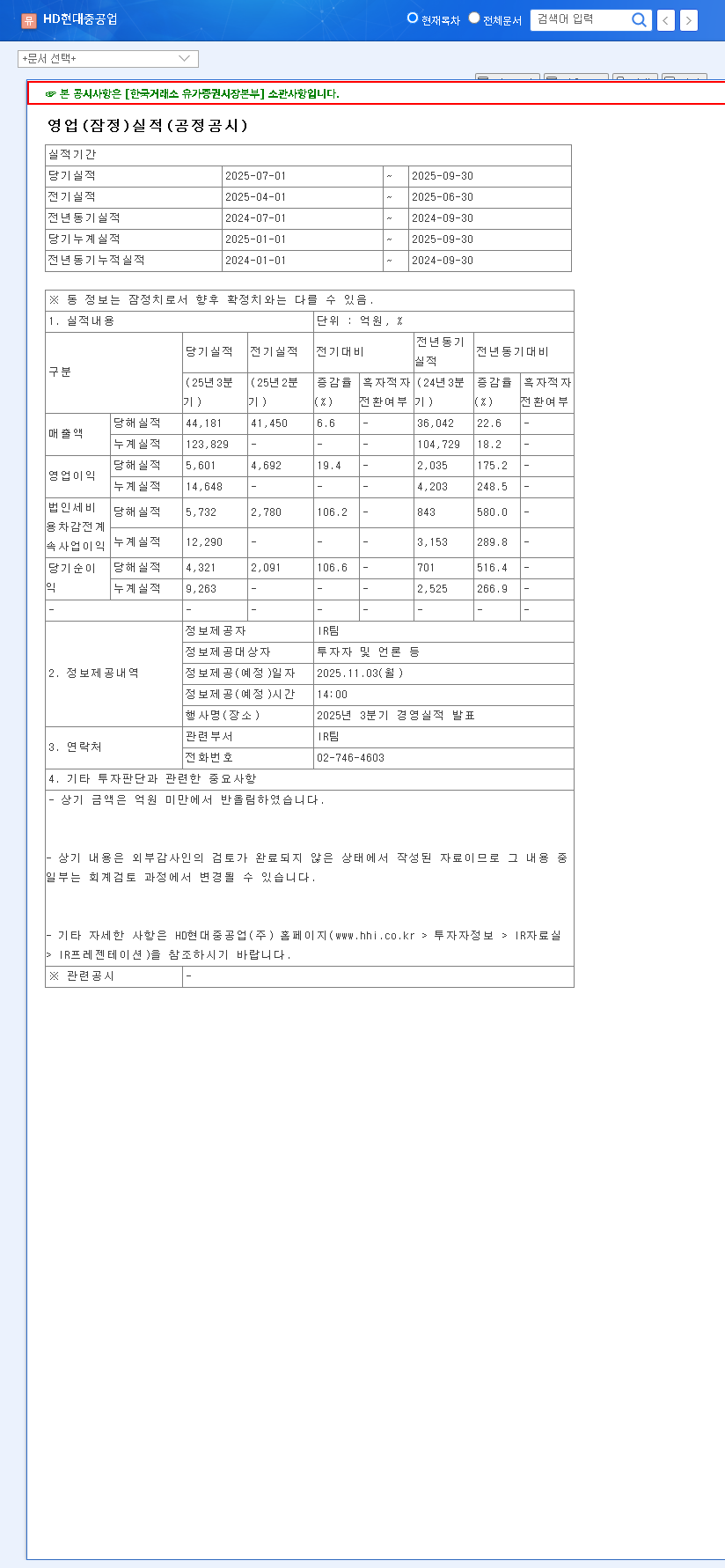

The recent order news is even more compelling when viewed against the backdrop of the company’s solid Q3 2025 performance. An analysis reveals a company firing on multiple cylinders, with a robust financial foundation.

1. Shipbuilding Division: The Engine of Profitability

- •Strengths: Representing nearly 70% of consolidated revenue, this core division saw a significant rise in operating profit. This is largely due to a strategic shift towards high-value-added and eco-friendly vessel orders. A massive order backlog exceeding 32 trillion won ensures stable revenue streams for the foreseeable future.

- •Challenges: A slight year-over-year revenue dip was noted, primarily due to the high-base effect from record orders in 2024. The division remains exposed to geopolitical risks and global trade policy shifts.

2. Offshore Plant & Engine Divisions: Diversification and Stability

- •Offshore Plant: This division has successfully returned to profitability and is exploring long-term growth in renewable energy (offshore wind) and next-gen nuclear (SMRs). However, a low utilization rate of 40.4% remains a key challenge to overcome.

- •Engine & Machinery: A stable pillar accounting for over 24% of revenue, this division maintains strong profitability thanks to its competitive HiMSEN engines and the growing adoption of eco-friendly fuel engines. Rising competition from Chinese and domestic rivals necessitates continuous innovation.

Investor Action Plan & Market Outlook

Given the strong fundamentals and positive order momentum, what is the strategic path forward for investors? A prudent approach involves monitoring several key internal and external factors that will influence the HD Hyundai Heavy Industries stock price.

Key Factors to Monitor

- •Crucial Re-disclosure: The market will be keenly focused on the re-disclosure by February 13, 2026. A successful contract finalization for the eco-friendly container ships could provide significant upside momentum.

- •Macroeconomic Headwinds: Keep a close watch on the won/dollar exchange rate, international commodity prices, and key shipping indices like the Baltic Dry Index. These external factors directly impact profitability and demand. For context, you can review expert analysis on the global shipping market trends from sources like Bloomberg.

- •Competitive Landscape: The shipbuilding industry is fiercely competitive. Monitor the order books and technological advancements of rivals like Samsung Heavy Industries and Hanwha Ocean to gauge HHI’s relative market position. Our deep dive into the shipbuilding market provides more detail.

- •Internal Execution: Track progress on improving the utilization rate of the offshore plant division. Success here could unlock a new, significant stream of revenue and profit.

In conclusion, HD Hyundai Heavy Industries presents a compelling growth story underpinned by a leading position in the transition to green shipping technology and solid financial health. While the uncertainty of the pending container ship deal presents a short-term risk, the long-term outlook appears positive. Cautious monitoring of the key factors outlined above is essential for making a well-informed investment decision.