The upcoming HD Hyundai Infracore merger with HD Hyundai Construction Equipment Co., Ltd. is a pivotal event for investors. With the recent completion of the stock appraisal rights exercise, a major hurdle has been cleared, paving the way for the merger’s finalization. This development has significant implications for the HD Hyundai Infracore stock price, its long-term corporate value, and the competitive landscape of the global construction equipment market.

This comprehensive analysis dissects the merger details, explores the potential synergies and risks, and provides a forward-looking perspective on the company’s fundamentals. We’ll equip you with the critical insights needed to make informed decisions about your HD Hyundai Infracore investment strategy in this transformative period.

Merger on Track: Analyzing the Stock Appraisal Rights Results

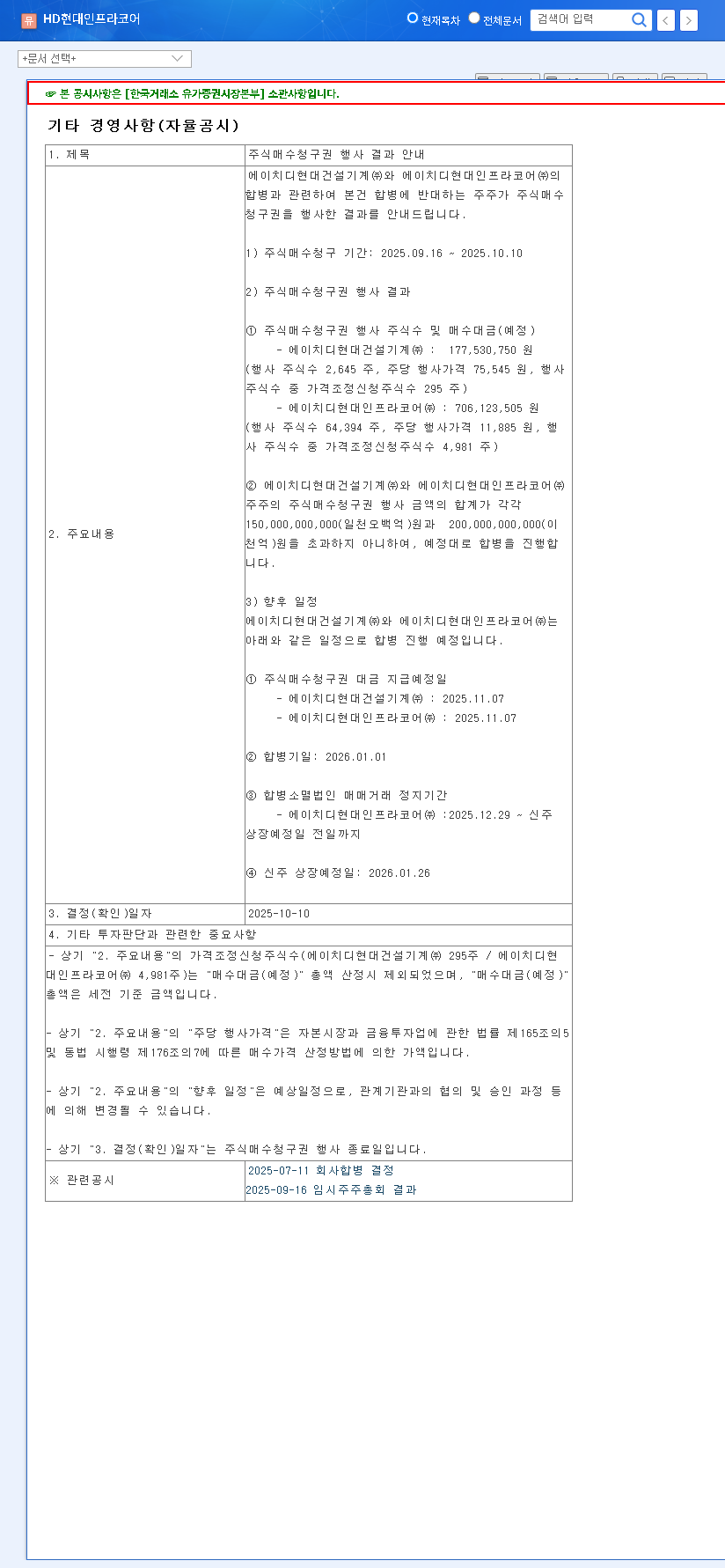

On October 13, 2025, HD Hyundai Infracore released the results of its stock appraisal rights exercise. This mechanism allows shareholders who oppose a merger to sell their shares back to the company at a predetermined fair price. The outcome is a crucial indicator of shareholder sentiment and can determine whether a merger proceeds.

The total value of exercised appraisal rights was well below the company’s predefined limit. This is a powerful green light, confirming that the HD Hyundai Infracore merger with HD Hyundai Construction Equipment will proceed as scheduled on January 1, 2026.

Key Merger Milestones & Schedule

- •Appraisal Rights Exercised: A minimal 64,394 shares from HD Hyundai Infracore (approx. KRW 706 million) and 2,645 shares from HD Hyundai Construction Equipment were exercised. You can view the Official Disclosure (Source) for details.

- •Trading Suspension: Trading for HD Hyundai Infracore stock will be suspended from December 29, 2025, until the new shares are listed.

- •New Share Listing: The newly merged entity’s shares are expected to be listed on January 26, 2026.

The Upside: Potential Synergies and Positive Impacts

A smooth merger process unlocks significant potential for value creation. By combining operations, the new entity can achieve enhanced scale and efficiency, positioning it more strongly against global competitors like Caterpillar and Komatsu.

Key Areas for Synergy

- •Enhanced R&D and Innovation: Pooling research and development budgets can accelerate the development of next-generation technologies, such as autonomous construction equipment and smart fleet management systems.

- •Operational Efficiency: Consolidating supply chains, manufacturing processes, and administrative functions can lead to substantial cost savings and improved profit margins.

- •Expanded Market Reach: The combined entity will have a stronger global distribution network, allowing it to penetrate new markets and better serve existing customers.

- •Financial Strength: The merger can help alleviate the financial burden of planned large-scale investments totaling KRW 504.16 billion, providing a more robust financial foundation for growth.

The Risks: Potential Headwinds and Investor Considerations

While the outlook is promising, investors must remain aware of potential challenges. The success of any large-scale merger is not guaranteed and depends on flawless execution and favorable market conditions.

- •Integration Challenges: Merging two distinct corporate cultures, IT systems, and operational workflows can lead to unforeseen friction and delays in realizing synergies.

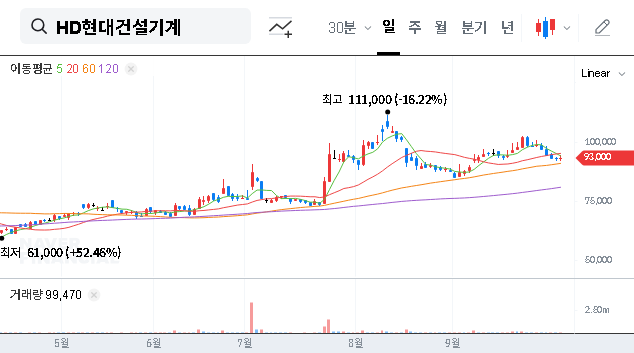

- •Short-Term Market Volatility: The planned trading suspension for the HD Hyundai Infracore stock could lead to price fluctuations and reduced liquidity in the short term.

- •Macroeconomic Pressures: The company faces headwinds from a potential slowdown in the global construction market, as highlighted by various reports from outlets like the Financial Times. High interest rates and currency fluctuations also pose risks.

Fundamental Analysis: A Look Under the Hood

An HD Hyundai Infracore investment decision must be grounded in its current financial health. As of H1 2025, the company has faced some profitability pressure, with revenue and operating profit declining due to market conditions. The debt-to-equity ratio has also increased, largely due to borrowing for strategic expansion.

However, the company is proactively building future growth drivers. The launch of its new ‘DEVELON’ brand, combined with a push into smart technology and defense industry contracts, demonstrates a clear strategy to diversify and innovate. This merger is a key part of that strategy, designed to bolster the company’s fundamentals for the long term. For more on this topic, see our analysis of the heavy equipment industry.

Investor Action Plan & Final Verdict

The successful navigation of the stock appraisal rights phase is a significant positive for the HD Hyundai Infracore merger. However, the overall investment outlook remains cautiously optimistic, or ‘Neutral’, pending the realization of merger synergies and a recovery in the broader construction market.

Key Takeaways for Investors:

- •Short-Term (3-6 Months): Be prepared for potential stock price volatility around the trading suspension and new share listing. This period is best suited for observant investors rather than active traders.

- •Long-Term (1-3 Years): The focus should be on the post-merger execution. Monitor quarterly earnings for evidence of cost savings and revenue synergies. The company’s ability to innovate and gain market share will be the ultimate driver of long-term value.

HD Hyundai Infracore is at a critical juncture. This merger positions it for a new era of growth, but successfully navigating the integration and external market challenges will be paramount. A patient, long-term perspective is advised for investors looking to capitalize on this transformative event.