This comprehensive Samsung Electronics stock analysis provides a meticulous look into the company’s current standing and future trajectory. Following a recent large shareholding report from Samsung C&T, investors are keen to understand the implications for management stability, stock performance, and long-term value. Simply looking at share percentages misses the bigger picture.

We will dissect the details of this report, evaluate Samsung Electronics’ fundamentals based on its H1 2025 performance, and identify the key Samsung Electronics future growth engines. We’ll also examine how macroeconomic variables could shape its path forward, offering an expert perspective for savvy investors.

Unpacking the Samsung C&T Shareholding Report

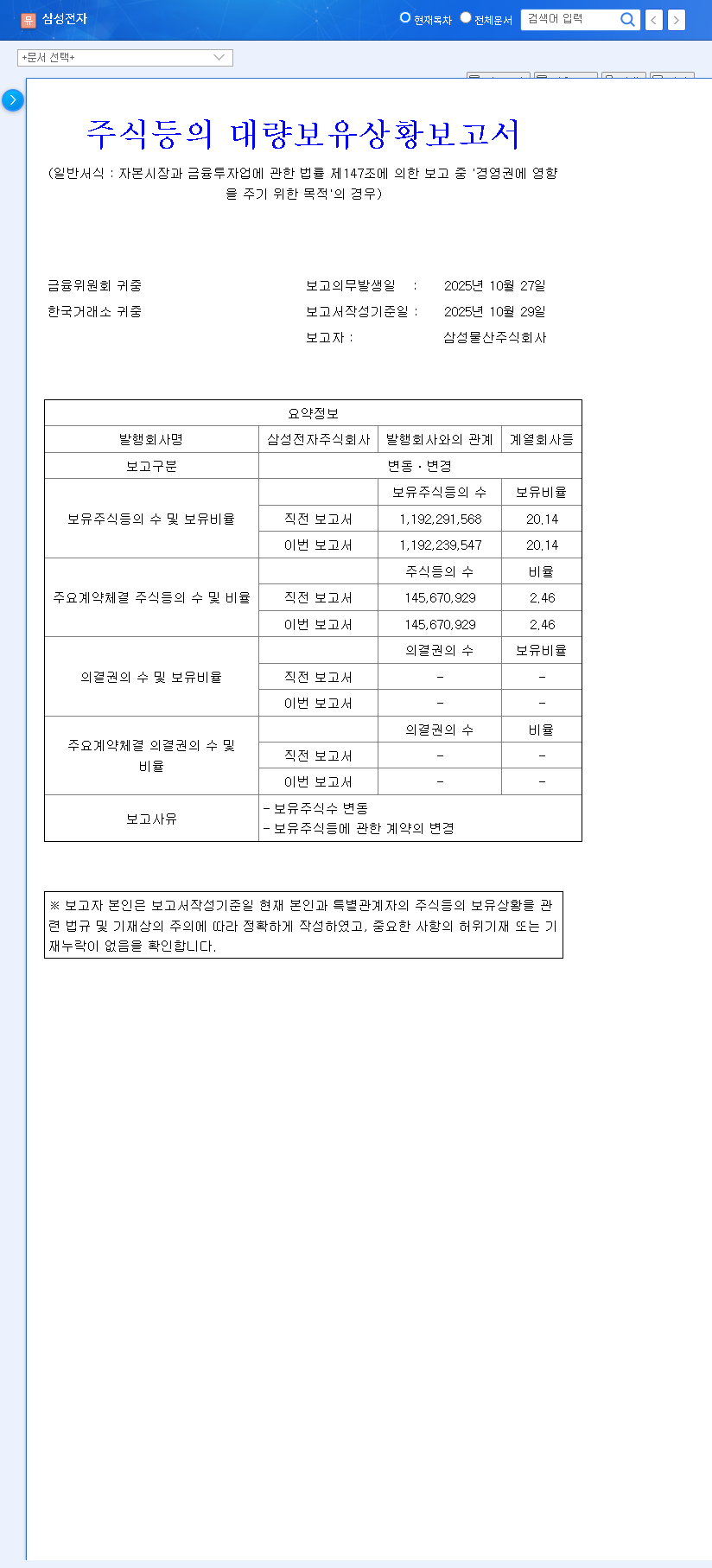

On October 31, 2025, Samsung C&T filed a ‘Report on the Status of Large Shareholdings’ concerning Samsung Electronics. The filing, available via this Official Disclosure, confirmed that Samsung C&T’s stake in Samsung Electronics Co., Ltd. remained unchanged at 20.14%. The primary reason cited for the report was minor changes in share-related contracts and small-scale transactions by related parties, not a strategic shift in ownership.

The key takeaway from the report is not change, but stability. It reaffirms a consistent governance structure, which is a crucial factor for long-term investors conducting a thorough Samsung Electronics stock analysis.

What This Signifies for Governance and Stability

The report explicitly states the holding purpose as ‘Influence over Management.’ This is a clear signal of Samsung C&T’s enduring commitment to participating in Samsung Electronics’ core strategic decisions. As a central entity in the group’s governance, this ensures a consistent and stable management direction. The minor share transactions by Samsung Life Insurance were part of routine portfolio adjustments and are too small to have any meaningful impact on the Samsung Electronics stock price or overall ownership structure.

Deep Dive: Samsung Electronics’ Robust Fundamentals (H1 2025)

Beyond governance, the company’s H1 2025 performance reveals powerful growth drivers that are solidifying its role as a leader in the AI era. These fundamentals are the true engine behind the company’s value.

Powering the AI Revolution: The DS (Device Solutions) Division

The semiconductor division is at the heart of Samsung Electronics future growth. Surging demand for AI servers has fueled impressive sales of high-bandwidth memory like HBM3E and high-capacity DDR5 modules. The company is also pushing the boundaries of technology by launching 2nm foundry products for mobile applications, strengthening its competitive edge against rivals. This positions Samsung to capture a significant share of the expanding AI chip market, which market analysts predict will see exponential growth.

Dominating Consumer Tech: DX, SDC, and Harman

Samsung’s other divisions continue to perform strongly:

- •DX (Device Experience): Continued leadership in the TV and mobile markets, highlighted by an expanded AI TV lineup and enhanced Galaxy AI features that are defining the next generation of smartphones.

- •SDC (Samsung Display): The OLED panel business is thriving, with diversification into IT, automotive, and foldable device applications ensuring a broad revenue base.

- •Harman: Showing impressive growth in lifestyle audio and successfully nurturing its automotive components business for next-gen vehicles.

Navigating Macroeconomic Headwinds

While the Samsung C&T shareholding news has a limited short-term impact, global economic factors will play a more significant role. Investors should monitor several key variables:

- •Interest Rates: Potential rate cuts by the US Federal Reserve (policy rate at 4.00%) could boost investor sentiment and appetite for tech stocks. The correlation with Korea’s policy rate (2.50%) will be crucial.

- •Exchange Rate Fluctuations: A strong US dollar against the Korean Won (KRW/USD ~1,648) benefits export profitability but introduces volatility risk for a global operator like Samsung.

- •Commodity & Shipping Costs: Volatility in oil prices and changes in shipping costs, reflected by indicators like the Baltic Dry Index, directly impact manufacturing and logistics expenses.

Conclusion: Investor Outlook for Samsung Electronics

This event should be viewed as a confirmation of long-term stability rather than a trigger for short-term price movement. Our Samsung Electronics stock analysis concludes that the company’s intrinsic value and future growth potential are the primary factors to consider. The company is strategically positioned to capitalize on the AI boom, supported by a diverse portfolio and a stable governance structure.

Investors should focus on the execution of its AI and advanced semiconductor strategies while keeping an eye on the broader economic environment. To understand the market better, consider reading our complete guide to investing in the semiconductor sector. Samsung Electronics’ technological leadership and market dominance suggest a strong capacity for sustained growth, provided it continues to manage global risks effectively.