The HARIM Q3 2025 earnings report has sent ripples through the investment community, presenting a stark contrast to the company’s triumphant performance in the first half of the year. After celebrating a remarkable 12% revenue growth and an explosive 238% surge in operating profit, investors are now faced with preliminary Q3 figures that suggest a significant slowdown. This has sparked a critical question: Is this a temporary hiccup or the beginning of a new, more challenging chapter for HARIM Co., Ltd. (136480)?

This comprehensive HARIM stock analysis will dissect the latest financial results, explore the underlying factors driving this shift, and evaluate the internal and external risks that could shape the company’s future. We will provide a clear outlook for investors, highlighting the key metrics to watch as HARIM navigates this pivotal moment.

Deconstructing the HARIM Q3 2025 Earnings Report

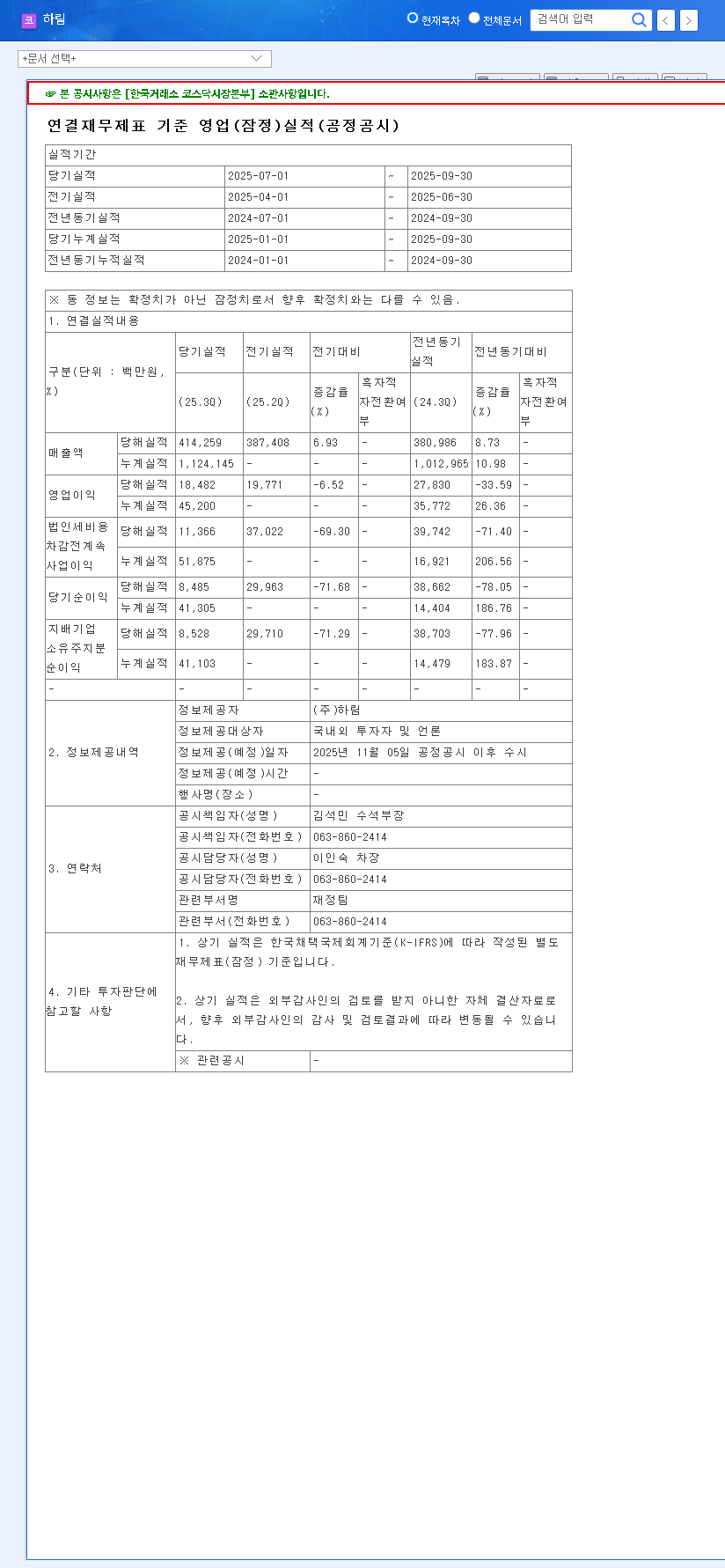

On November 5, 2025, HARIM released its preliminary operating results for the third quarter, revealing a noticeable deceleration. The official filing provides the granular details for investors. For a complete breakdown, investors can consult the company’s official filing on DART. Source: Official Disclosure. The key figures are:

- •Revenue: KRW 402.4 billion (a marginal increase from Q2).

- •Operating Profit: KRW 18.6 billion (a significant decrease from Q2).

- •Net Profit: KRW 9 billion (also a marked decrease from Q2).

These numbers confirm that the powerful growth engine seen in H1 has throttled back, prompting a deeper investigation into the causes.

From a ‘Sunny’ H1 to a ‘Cloudy’ Q3: What Changed?

H1 2025: A Foundation of Solid Growth

The first half of 2025 was a period of robust recovery for HARIM. The company successfully turned a profit, driven by key fundamental strengths. A major contributor was a significant improvement in the cost structure, achieved through stabilizing feed raw material prices, optimizing chicken slaughter yields, and minimizing packaging losses. This, combined with its unshakable No. 1 position in the domestic chicken market, created a powerful combination for profitability.

Key Factors Behind the Q3 Earnings Slowdown

The Q3 downturn appears to be a result of several converging headwinds:

- •Commodity Price Volatility: While H1 saw favorable feed prices, the market is inherently volatile. Any subsequent rise in core ingredients directly squeezes profit margins. According to a recent market report from Bloomberg, global grain markets remain sensitive to geopolitical and climate factors, posing an ongoing risk.

- •Intensified Market Competition: As the market leader, HARIM is a prime target for competitors. Aggressive pricing strategies from rivals can erode market share and put downward pressure on prices, impacting revenue and profitability.

- •Macroeconomic Pressures: External factors like currency fluctuations are critical. With the KRW/USD exchange rate hovering around 1,444.00, a weaker Won increases the cost of imported raw materials. Furthermore, persistent high interest rates amplify the burden of HARIM’s debt, which, despite improving to a 101.66% ratio, remains a significant financial consideration.

- •Operational Risks: The poultry industry is perpetually exposed to the risk of disease outbreaks like avian influenza (AI), which can devastate supply chains and lead to substantial financial losses.

Market Impact and Investor Outlook

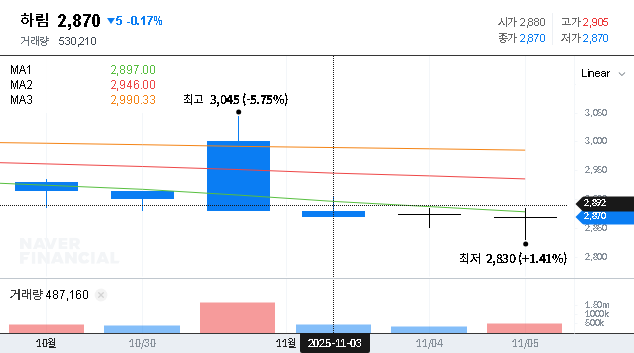

The market had priced in continued momentum after a stellar H1. The Q3 results have introduced a dose of realism, shifting investor sentiment from bullish optimism to cautious observation. The next two quarters will be crucial in determining the stock’s trajectory.

The unexpected slowdown is likely to increase short-term stock price volatility as the market recalibrates its expectations for the 136480 stock analysis. Investors who rode the wave of H1’s success may look to secure profits, while new investors will be looking for clarity on the company’s strategy to counter these new challenges.

Future Challenges and Strategic Imperatives

Moving forward, investors should closely monitor HARIM’s strategic responses. Key areas to watch include:

- •Profitability of Core Divisions: Scrutinize management’s plans to address any losses or margin compression in the meat processing division.

- •Growth Initiatives: The success of expanding online sales channels and launching innovative new products will be vital to offsetting traditional market pressures. For more on industry trends, see our complete guide to the food processing sector.

- •Financial Discipline: Continued efforts to manage the high debt ratio and mitigate interest cost burdens are non-negotiable for long-term stability.

- •ESG and Governance: Addressing legal risks from Fair Trade Act violations and strengthening ESG management, such as animal welfare systems, are crucial for building long-term corporate value and maintaining investor trust.

Conclusion: A Balanced View on HARIM’s Future

While the HARIM Q3 2025 earnings signal a period of caution, it’s important to weigh this against the company’s fundamental strengths. HARIM’s dominant market position and vertically integrated cost structure provide a resilient foundation. However, the path forward will depend on its ability to navigate commodity volatility, fend off competition, and manage its financial liabilities effectively. For investors, this is a time for diligent monitoring rather than hasty decisions. The company’s long-term growth potential remains intact, but its short-term performance now hinges on strategic execution in a more demanding environment.

Frequently Asked Questions

Q1: What were the key takeaways from HARIM’s Q3 2025 earnings?

A1: HARIM’s Q3 2025 earnings showed a significant growth slowdown. While revenue saw a slight increase to KRW 402.4 billion, both operating profit (KRW 18.6 billion) and net profit (KRW 9 billion) decreased considerably compared to the first half of the year.

Q2: Why was HARIM’s performance so strong in H1 2025?

A2: In H1 2025, HARIM’s revenue grew by 12.31% and operating profit surged by 238.09%. This was driven by effective cost reduction, stable raw material prices, and leveraging its #1 market share in South Korea.

Q3: What caused the slowdown in HARIM’s Q3 performance?

A3: The slowdown is attributed to a mix of factors, including rising raw material costs, increased competition in the domestic market, macroeconomic pressures like exchange rate volatility, and persistent operational risks like potential disease outbreaks.

Q4: What should investors watch for regarding HARIM’s stock?

A4: Investors should monitor the company’s strategy for improving margins, the performance of its new products and online channels, its progress in managing debt, and any updates on external factors like interest rates and commodity prices. This HARIM stock analysis suggests a period of heightened vigilance.