The latest Hansol Paper Q3 2025 earnings report sent shockwaves through the market, revealing a significant deficit where analysts had expected a profit. This wasn’t just a minor miss; it was a deep plunge that raises critical questions about the company’s structural health and future trajectory. For investors holding or considering Hansol Paper (213500) stock, this moment calls for a meticulous analysis beyond the headline numbers. This comprehensive guide will dissect the performance, explore the underlying causes, and provide an actionable investment strategy based on a thorough Hansol Paper stock analysis.

Unpacking the Q3 2025 Earnings Shock

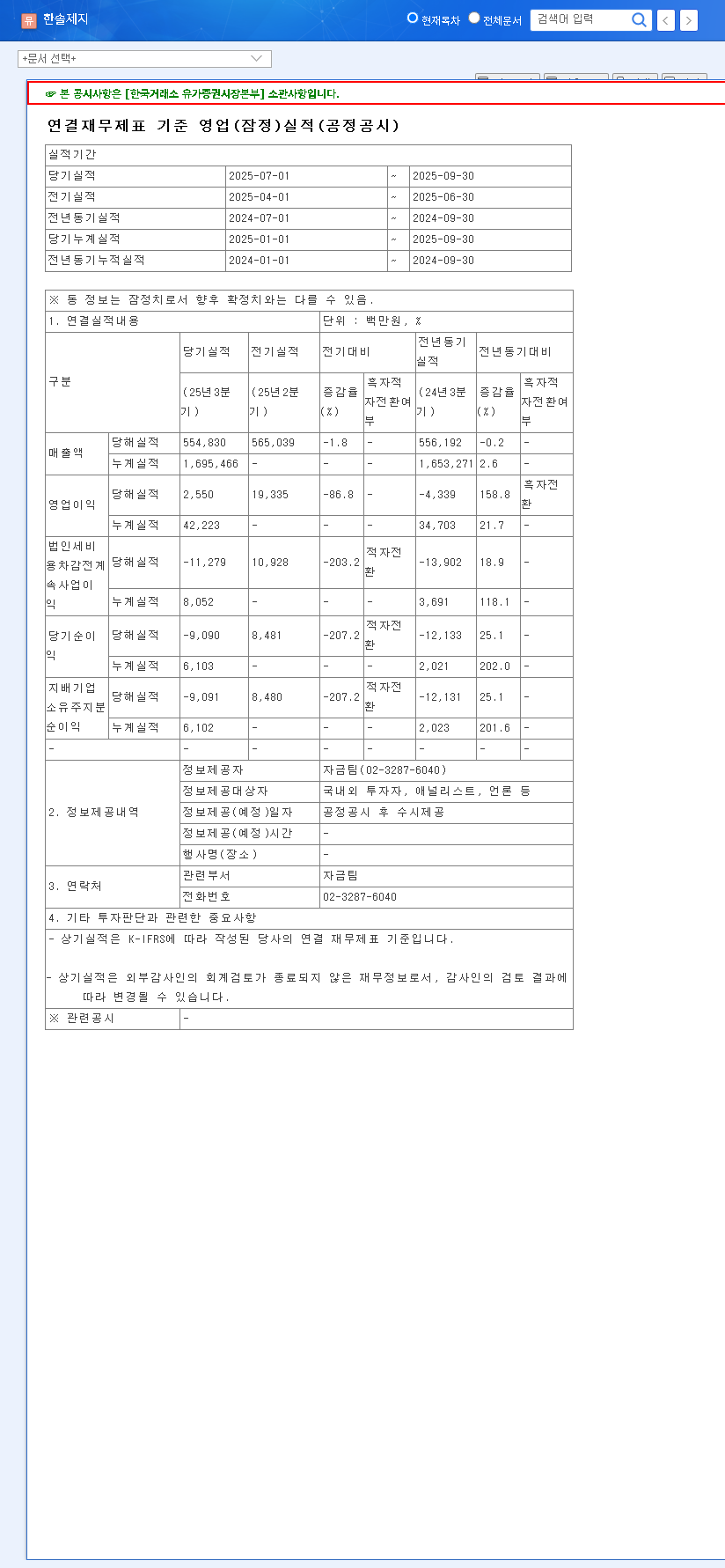

On October 30, 2025, Hansol Paper’s financial release starkly contrasted with market consensus. While revenue showed modest outperformance, the profitability metrics told a completely different, more alarming story.

- •Revenue: KRW 554.8 billion (Slightly beating the KRW 549.2 billion expectation by 1%)

- •Operating Profit: KRW 2.6 billion (A staggering 83% miss from the expected KRW 15.5 billion)

- •Net Income: KRW -9.1 billion (A massive 221% deficit against an expected profit of KRW 7.5 billion)

The swing from an expected profit to a significant net loss indicates that the issues at play are more than temporary headwinds. They point towards deep-seated structural challenges that demand investor attention.

Root Cause Analysis: Why Did Hansol Paper Falter?

The disconnect between revenue and profit suggests a severe margin squeeze. This was not caused by a single factor, but a confluence of internal pressures, market dynamics, and corporate governance questions.

Segment-by-Segment Performance Breakdown

A closer look at the company’s core divisions reveals a widespread struggle:

- •Industrial & Printing Paper: Despite lower pulp costs, a global economic slowdown suppressed demand in developed markets. This led to aggressive price competition, eroding selling prices and neutralizing any cost benefits.

- •Specialty & Thermal Paper: While this segment has been a consistent performer, the overall market deterioration limited its ability to defend profitability, failing to offset the steep declines elsewhere.

- •New Ventures (Eco-friendly Packaging): While strategically vital for future growth, these new business lines are still in a nascent phase. Their contribution to the bottom line remains limited and could not cushion the blow from the core business underperformance. For more on this trend, see our guide to sustainable packaging solutions.

Corporate Governance Red Flags

Adding to the operational woes, a recent correction to public disclosures regarding executive compensation has raised concerns about management transparency. The omission of Chairman Cho Dong-gil’s compensation, detailed in the Official Disclosure (Source: DART), can erode investor confidence and may lead to a higher risk premium being assigned to the stock.

When operational performance falters, investor scrutiny on corporate governance intensifies. Transparency is not just a best practice; it’s a critical component of a company’s valuation and long-term stability.

Future Outlook and Investment Strategy

The disappointing Hansol Paper Q3 2025 earnings create significant uncertainty. Investors must navigate both short-term market reactions and the company’s long-term strategic viability.

Short-Term: Navigating the Volatility

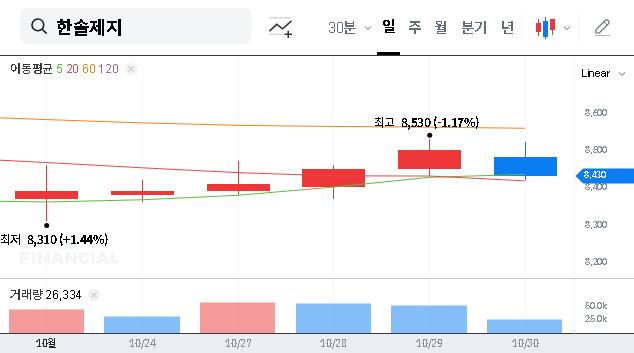

In the immediate aftermath, the stock will likely face significant downward pressure. The market will be laser-focused on the upcoming Q4 report and any guidance for 2026. Any sign of continued margin erosion could trigger further sell-offs. The key short-term catalyst will be a clear and credible plan from management to restore profitability.

Mid-to-Long-Term: The Path to Recovery

Recovery hinges on two pillars: operational efficiency and strategic diversification. While positive macroeconomic shifts like falling oil prices and stabilizing shipping costs provide some relief, they cannot fix internal issues. The success of the company’s pivot to high-growth areas like eco-friendly packaging will be the ultimate determinant of long-term value creation. This requires not just investment but flawless execution.

Investor Action Plan: A Conservative Approach is Warranted

Given the severity of the earnings miss and the underlying structural concerns, a cautious and defensive stance is prudent. Before considering a new or increased position, investors should closely monitor the following checkpoints:

- •Profitability Metrics: Watch for a tangible recovery in operating profit and net income margins in subsequent quarters.

- •Management Actions: Look for decisive cost-cutting measures, improved pricing strategies, and enhanced transparency from leadership.

- •New Business Growth: Assess the revenue growth and path to profitability for the eco-friendly packaging and new materials segments.

- •Industry Trends: Monitor paper demand and pricing dynamics. For a deeper understanding of market analysis, resources like Investopedia offer excellent guides on fundamental analysis.

In conclusion, this detailed 213500 earnings report analysis suggests that a ‘wait-and-see’ approach is the most logical strategy. The risks currently outweigh the potential rewards until there is clear evidence of a fundamental turnaround.