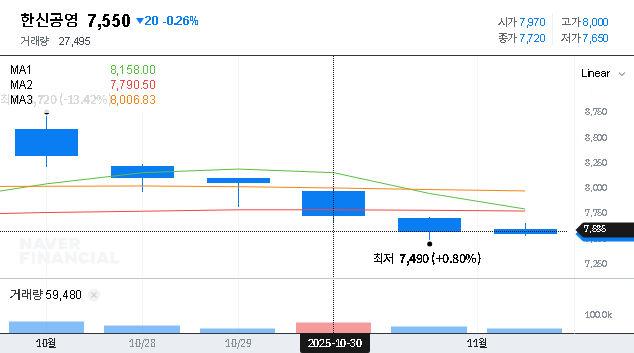

In a significant development for the South Korean construction sector, HANSHIN CONSTRUCTION CO.,LTD (004960) has secured a major contract that is turning heads among investors. The company was officially named the contractor for the ‘Siheung 1-dong 864-1 Area Housing Redevelopment Project,’ a massive undertaking valued at approximately KRW 149.6 billion. For those analyzing HANSHIN CONSTRUCTION stock, this news represents a pivotal moment, accounting for nearly 10% of the company’s recent annual revenue. This article provides a comprehensive analysis of this new project, its impact on HANSHIN’s fundamentals, and the strategic outlook for potential investors.

Project Deep Dive: The KRW 149.6 Billion Siheung Contract

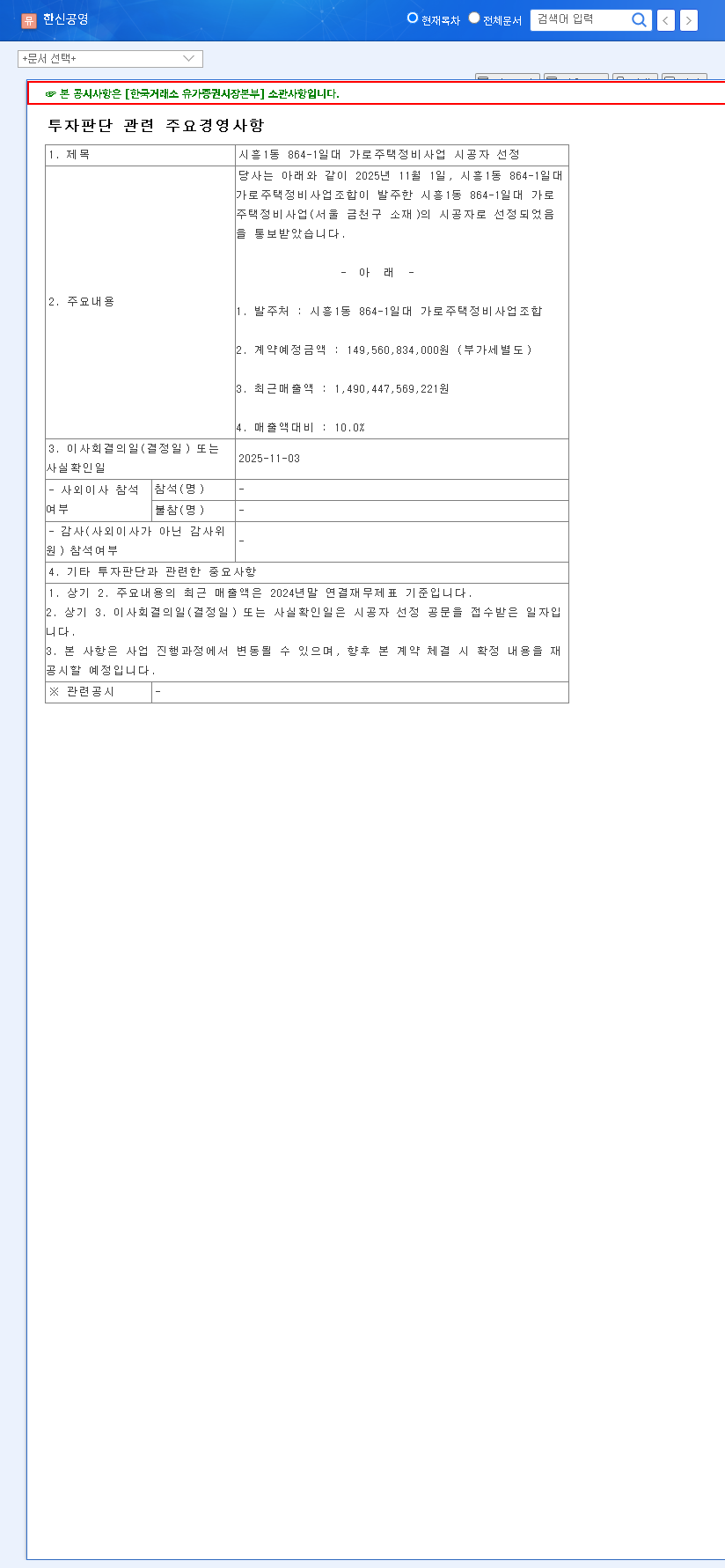

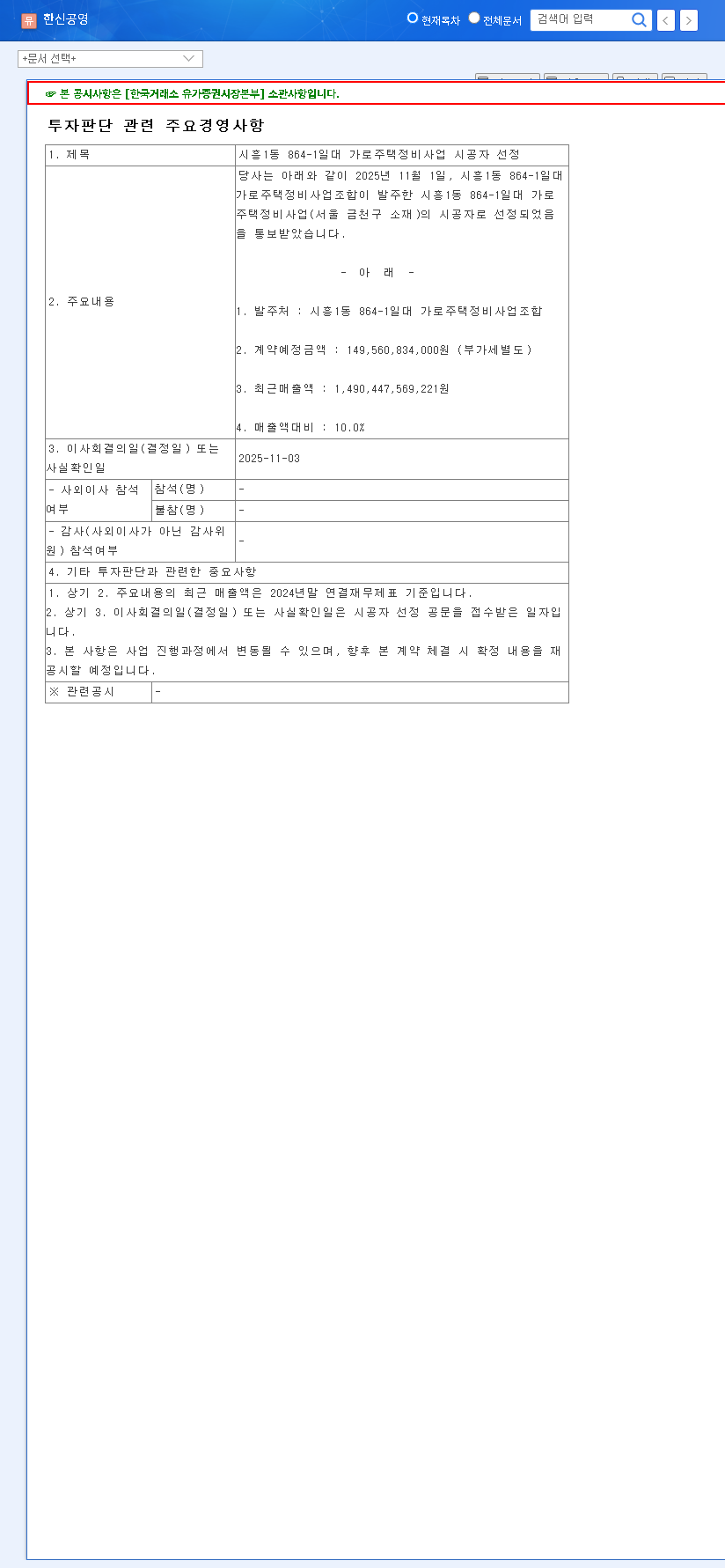

On November 1, 2025, HANSHIN CONSTRUCTION received official notification of its successful bid for the Siheung Redevelopment Project. The contract, commissioned by the local housing redevelopment association, carries an estimated value of KRW 149,560,834,000 (excluding VAT). This isn’t just another project; its scale is substantial enough to significantly influence the company’s revenue pipeline and future growth trajectory. The official details of this contract can be verified in the company’s public filing, as seen in this Official Disclosure. Securing such a large-scale urban regeneration project reinforces HANSHIN’s competitive position in the domestic market and is expected to have a material, positive impact on its order backlog.

In-Depth Fundamental Analysis of HANSHIN CONSTRUCTION

Beyond this single contract win, a thorough HANSHIN CONSTRUCTION analysis reveals a company on an improving financial path. While past projects have sometimes faced delays moving from pre-construction to revenue generation, the company’s commitment to transparent reporting has helped maintain investor confidence. Let’s examine the core financials.

Financial Performance & Growth Trajectory (Consolidated)

- •Revenue Growth: In 2024, consolidated revenue climbed to KRW 1.49 trillion, marking a solid 14% year-over-year increase, driven by the completion of proprietary projects.

- •Surging Profitability: Operating profit experienced a remarkable 153% surge to KRW 37.3 billion, largely due to improved cost management and the settlement of development profits.

- •Improving Debt Profile: The debt-to-equity ratio, while still at 197%, is trending in the right direction, falling by 14% from the previous year.

- •Stable Liquidity: With KRW 266.4 billion in cash and cash equivalents, the company maintains a robust liquidity position to navigate operational needs.

The combination of strong revenue growth, a significant jump in operating profit, and a steadily improving balance sheet paints a picture of a company regaining its footing in a competitive market. This new contract win acts as a powerful catalyst on an already positive trajectory.

Strategic Outlook: What This Means for Investors

The Siheung Redevelopment Project will directly impact the HANSHIN CONSTRUCTION stock valuation, but investors must weigh both the opportunities and the inherent risks associated with the construction industry.

Opportunities & Upside Potential

The most direct benefit is a significant and predictable revenue stream that will be recognized over the next few years. This enhances earnings visibility, which is highly valued by the market. Furthermore, successfully executing a project of this scale diversifies HANSHIN’s portfolio and strengthens its reputation in the lucrative urban regeneration sector. This can create a flywheel effect, making it easier to win similar large-scale bids in the future. For a deeper understanding of how project backlogs affect valuations, you can review our guide on analyzing South Korean construction stocks.

Potential Risks & Macroeconomic Headwinds

Investors must remain pragmatic. The construction industry is sensitive to macroeconomic shifts. Persistently high interest rates can dampen real estate sentiment and increase financing costs. Volatility in currency exchange rates and global commodity prices (e.g., steel, oil) can impact material costs and erode profit margins. As noted by industry reports from sources like Reuters, supply chain stability remains a key concern. Finally, there are always execution risks, such as potential project delays or cost overruns, which require diligent management from the company.

Final Verdict: An Investment Strategy for HANSHIN CONSTRUCTION Stock

The Siheung project win is an unequivocally positive catalyst for HANSHIN CONSTRUCTION. It validates the company’s operational capabilities and adds substantial weight to its future earnings potential. For investors, this event strengthens the bullish case for the stock. However, a prudent strategy involves a long-term perspective. It is crucial to monitor the project’s execution progress, keep a close watch on macroeconomic indicators, and consider the HANSHIN CONSTRUCTION stock price in the context of the broader market. This development solidifies HANSHIN’s position as a noteworthy player among South Korean construction stocks, warranting careful consideration for inclusion in a diversified portfolio.