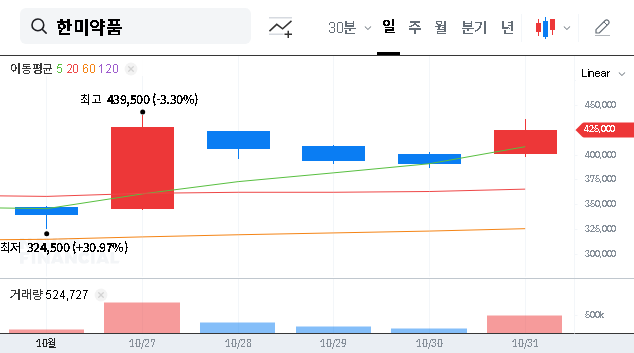

On November 4, 2025, the investment community will turn its attention to a pivotal event: the Hanmi Pharm. IR (Investor Relations) session. Hosted as part of the SK Securities Non-Deal Roadshow (NDR), this is far more than a routine update. For prospective and current stakeholders, this session is a critical window into the company’s Q3 2025 performance, its resilience in a volatile global market, and its strategic roadmap for future growth. This analysis will provide a comprehensive breakdown of what to expect, from financial transparency to R&D pipeline developments, offering a detailed guide for any Hanmi Pharm. investment decisions.

Understanding the nuances of the upcoming disclosures and the macroeconomic context is essential. We will delve into recent corporate actions, analyze potential market impacts, and highlight the key questions that investors should be asking to truly gauge the long-term potential of Hanmi Pharm. stock.

Hanmi Pharm. IR Event Overview

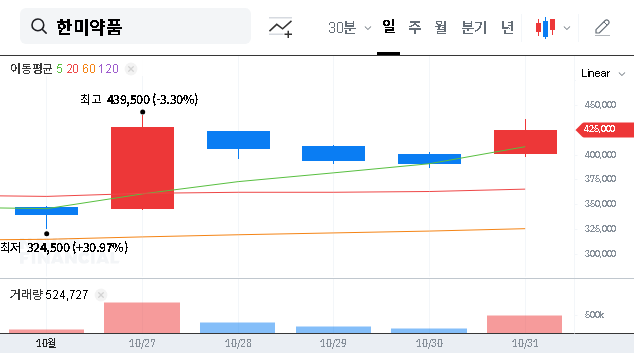

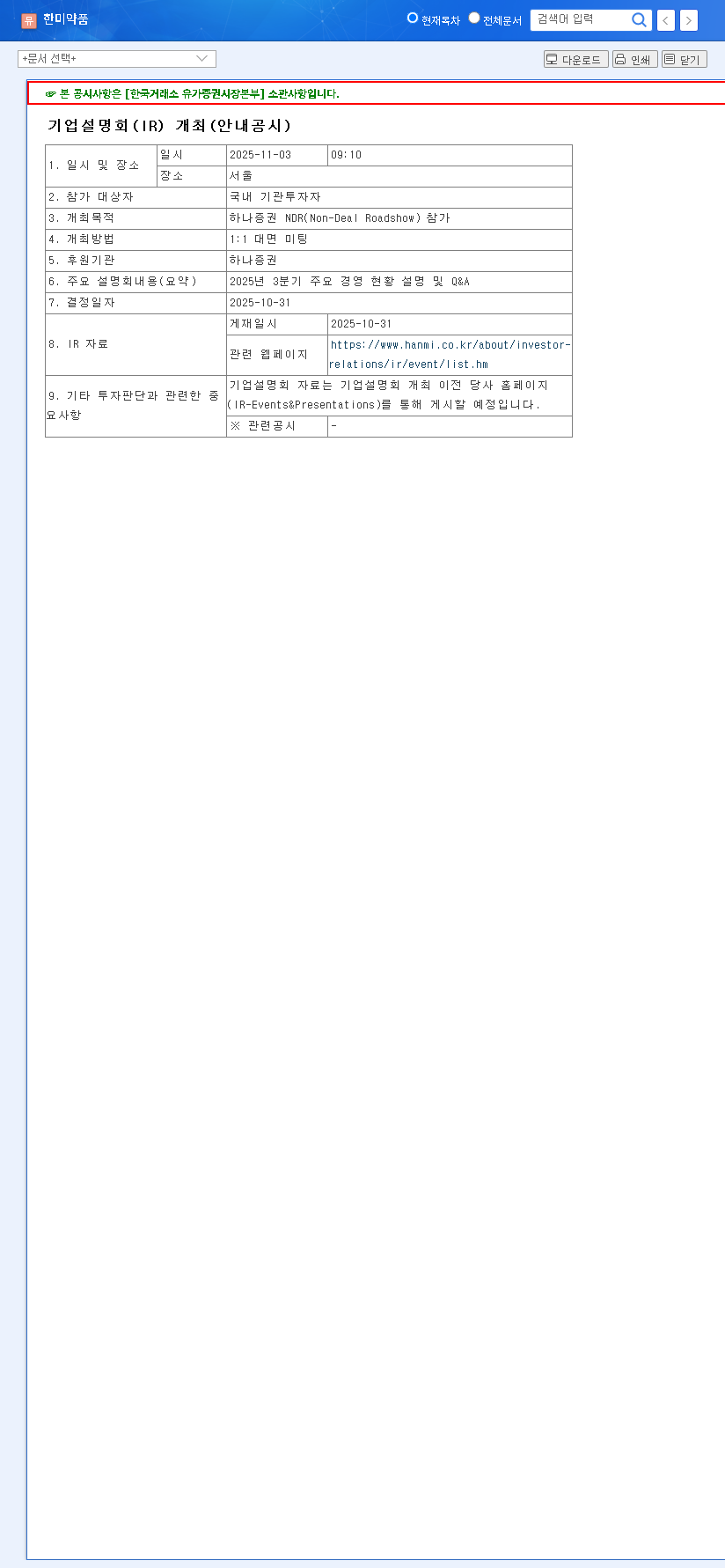

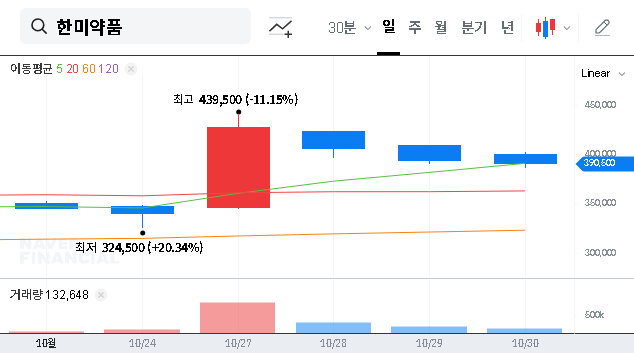

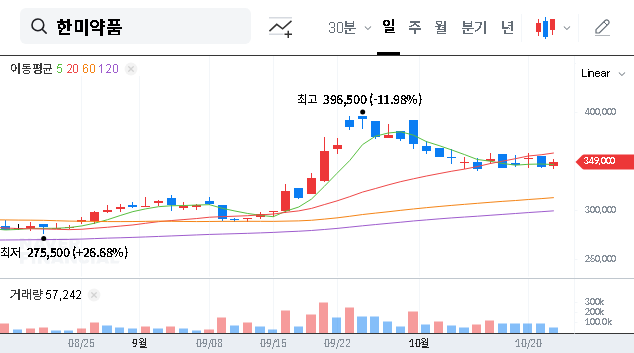

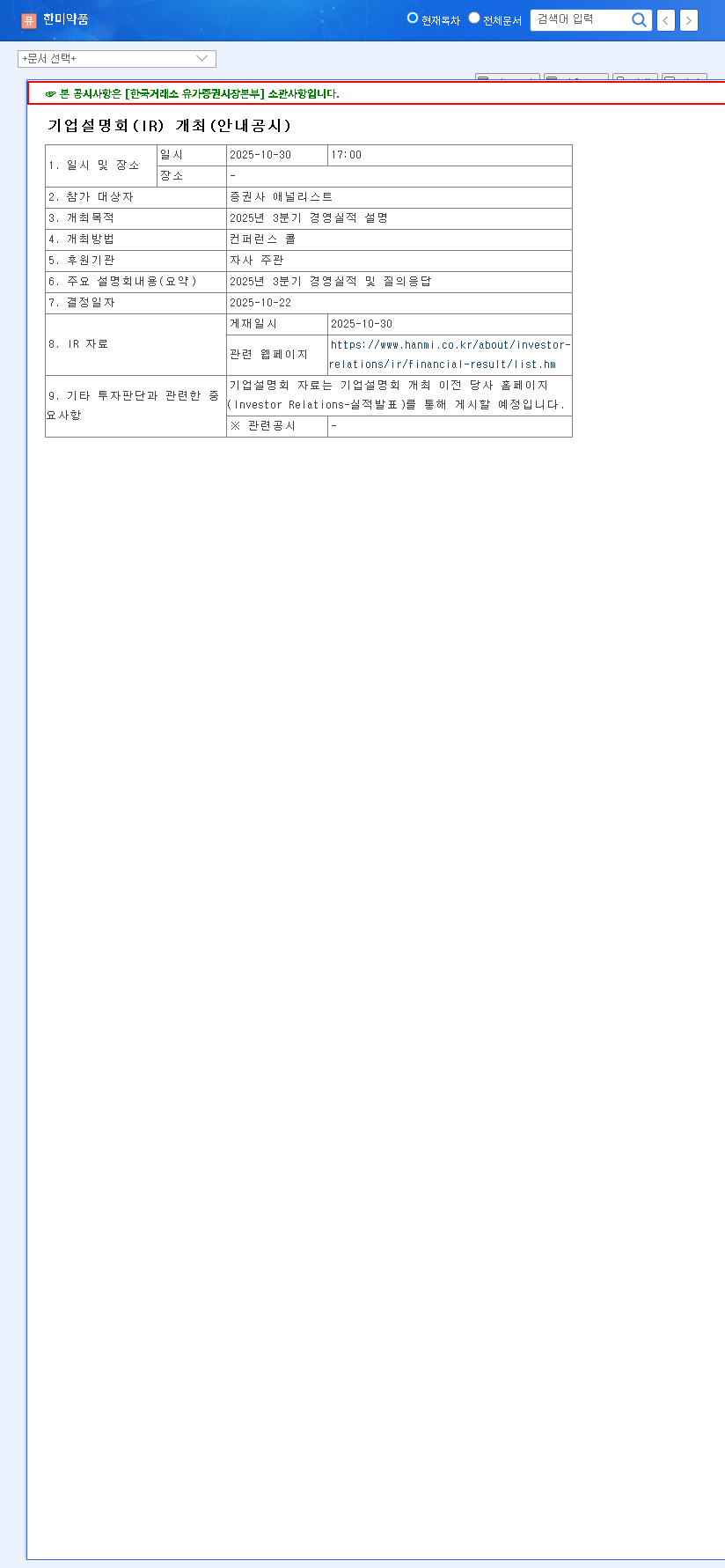

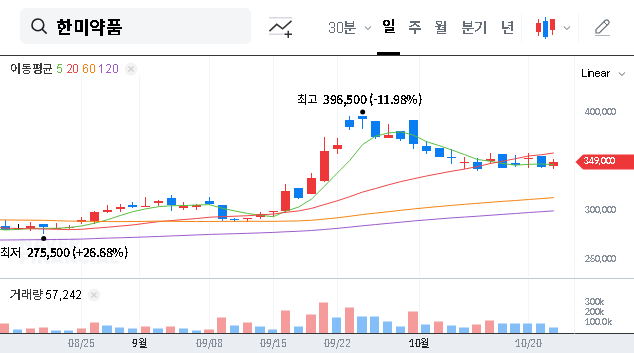

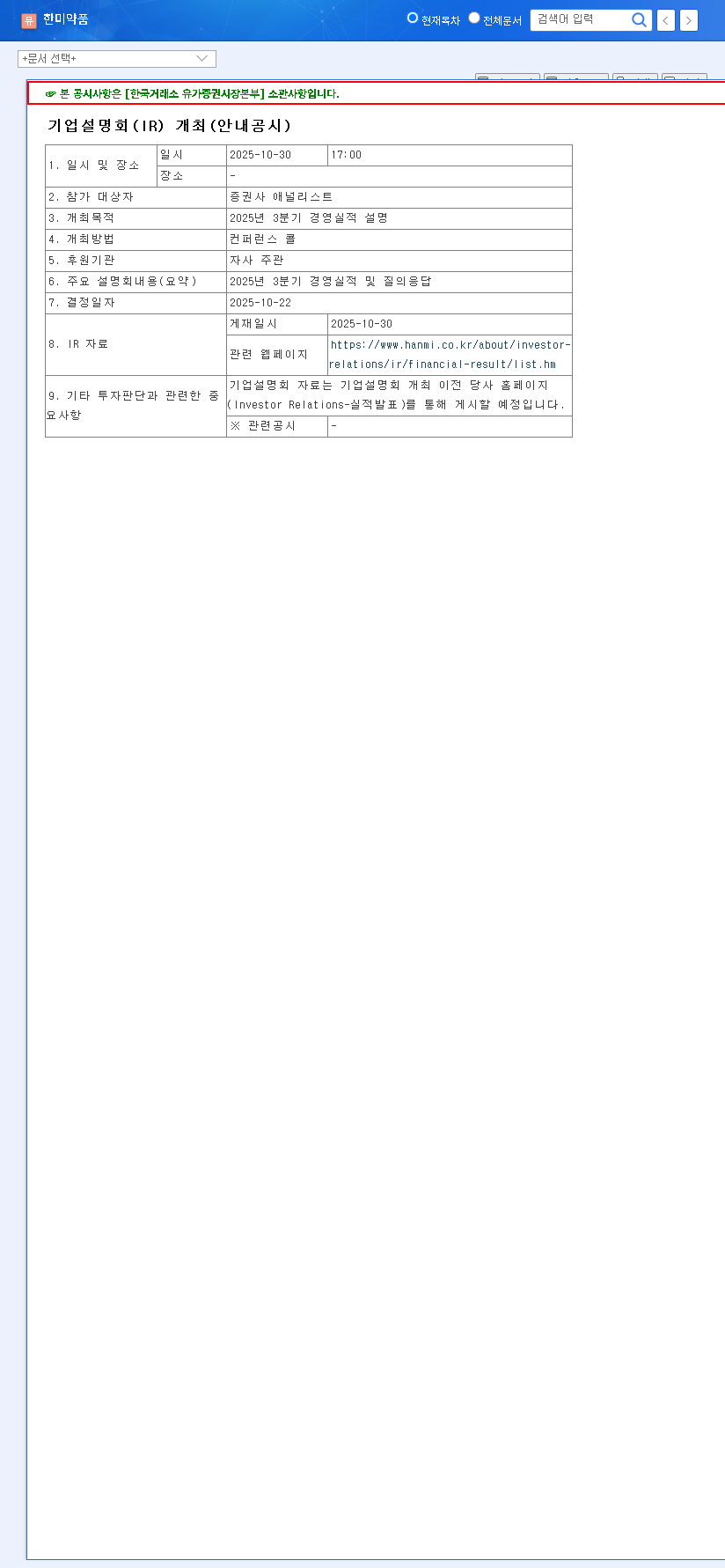

Mark your calendars for 09:10 AM on November 4, 2025. This is when Hanmi Pharm. Co., Ltd. is scheduled to present. The primary agenda is to clarify the company’s Q3 2025 management status and engage in a direct Q&A with the investment community. For a company with a market capitalization hovering around 5.44 trillion KRW, the insights shared during this IR will undoubtedly cause ripples in the market, influencing investor sentiment and the Hanmi Pharm. stock trajectory.

The Importance of Financial Transparency

Recently, Hanmi Pharm. took a proactive step to bolster investor confidence by filing a correction disclosure. This addressed a previous omission in its semi-annual report concerning investment details in the ‘Shiwha Industrial Complex Pharmaceutical Business Cooperative’. While the financial impact of this cooperative is negligible to Hanmi’s bottom line—with a book value of approximately 2.1 billion KRW and a minor net loss—the act of correction is profoundly significant. It signals a commitment to complete transparency, a cornerstone of good corporate governance. You can review the Official Disclosure on the DART system. This move reassures investors that financial reporting is meticulous and trustworthy, which is crucial for long-term Hanmi Pharm. investment stability.

The key takeaway from the disclosure correction is not the financial data itself, but the company’s reinforced commitment to transparency. This builds a foundation of trust that is invaluable in the pharmaceutical sector.

Navigating the Macroeconomic Headwinds

No company operates in a vacuum, and Hanmi Pharmaceutical performance is subject to the pressures of the global economy. Investors should closely monitor several key macroeconomic variables that could impact profitability and growth.

- •Currency Fluctuations: The won/dollar exchange rate is a critical factor. Projections indicate that a 10% appreciation in the USD could boost Hanmi’s profit before tax by over 9.5 billion KRW. This highlights the company’s sensitivity to global currency markets, a double-edged sword that can either buffer or erode earnings.

- •Interest Rate Environment: While there are broad expectations for rate cuts globally, the risk of a hike remains. An estimated 1% increase in interest rates could decrease Hanmi’s net income by 1.6 billion KRW. This is particularly relevant for a research-intensive company where capital for R&D is paramount. For more context on global rate policies, see analysis from sources like Reuters Financial.

- •Supply Chain Costs: Volatility in oil prices and ocean freight rates directly impacts the cost of raw materials and logistics. A recent downturn in the China Container Freight Index is a positive sign, potentially stabilizing expenses, but this area requires continuous monitoring.

Strategic Investment Outlook: What to Watch in the Hanmi Pharm. IR

The upcoming Hanmi Pharm. IR provides an opportunity to look beyond the surface. Investors should focus on the substance of the presentation to build a robust investment thesis. Here’s what to prioritize:

1. Deep Dive into R&D Pipeline Progress

The true engine of a pharmaceutical company’s long-term growth is its R&D pipeline. Pay close attention to updates on key clinical trials, new drug development timelines, and commercialization strategies. Progress in high-value areas like oncology, metabolic diseases, or rare disorders will be a significant catalyst for the stock. For a deeper understanding, you can review our complete guide to Hanmi’s R&D.

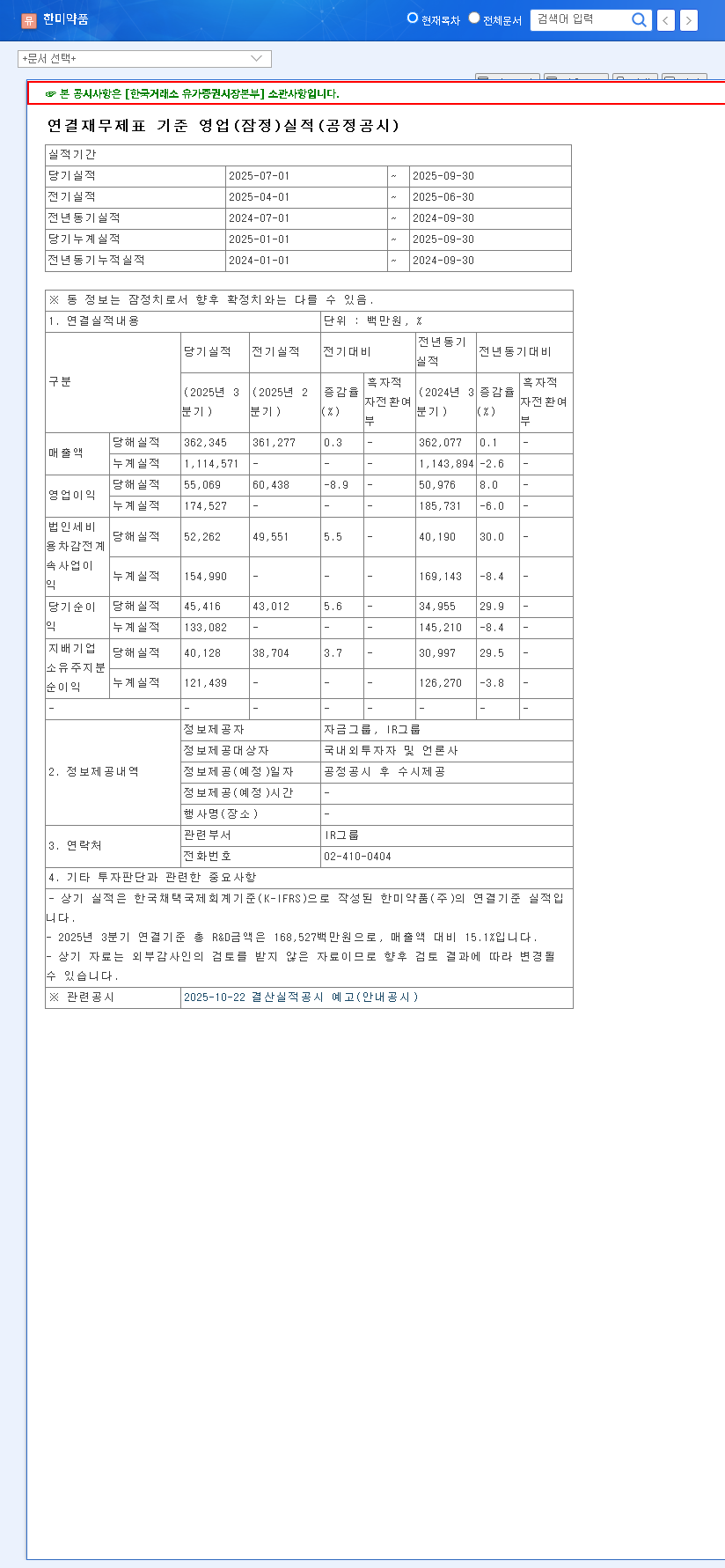

2. Q3 2025 Performance Metrics

Beyond the headline revenue and profit numbers, look for details on sales growth for key products, market share trends, and margin analysis. How is the company performing against its own forecasts and competitor benchmarks? The quality of earnings and the drivers behind the results are more important than the raw figures.

3. Management’s Forward-Looking Guidance

The management’s outlook for Q4 and early 2026 will be a crucial indicator of their confidence. Listen for specific targets related to revenue, investment plans, and anticipated milestones. Their tone and the clarity of their strategy during the Q&A session can often be as revealing as the prepared presentation.

In conclusion, this Hanmi Pharm. IR is a must-watch event. By focusing on the core fundamentals—R&D progress, transparent financial health, and a clear strategic vision—investors can cut through the noise. A prudent approach involves using the information from the IR to make a well-rounded decision, balancing the company’s internal strengths against the external macroeconomic environment. This disciplined analysis will be the key to a successful Hanmi Pharm. investment strategy.