On October 2, 2025, Hankook Furniture Co. Ltd. (KRX: 004590) announced its quarterly dividend, a decision that warrants a closer look beyond the headline number. The Hankook Furniture dividend of KRW 35 per share, representing a modest 0.6% yield, raises a critical question for investors: Is this a signal of stable shareholder returns from a reliable company, or a minor consolation prize from a business facing significant internal and external pressures? This comprehensive Hankook Furniture stock analysis will dissect the company’s dual-natured business, evaluate its financial health, and provide a clear action plan for potential investors.

We’ll explore the stark contrast between its struggling furniture division and the stellar Jewon International performance, uncovering the true story behind the numbers.

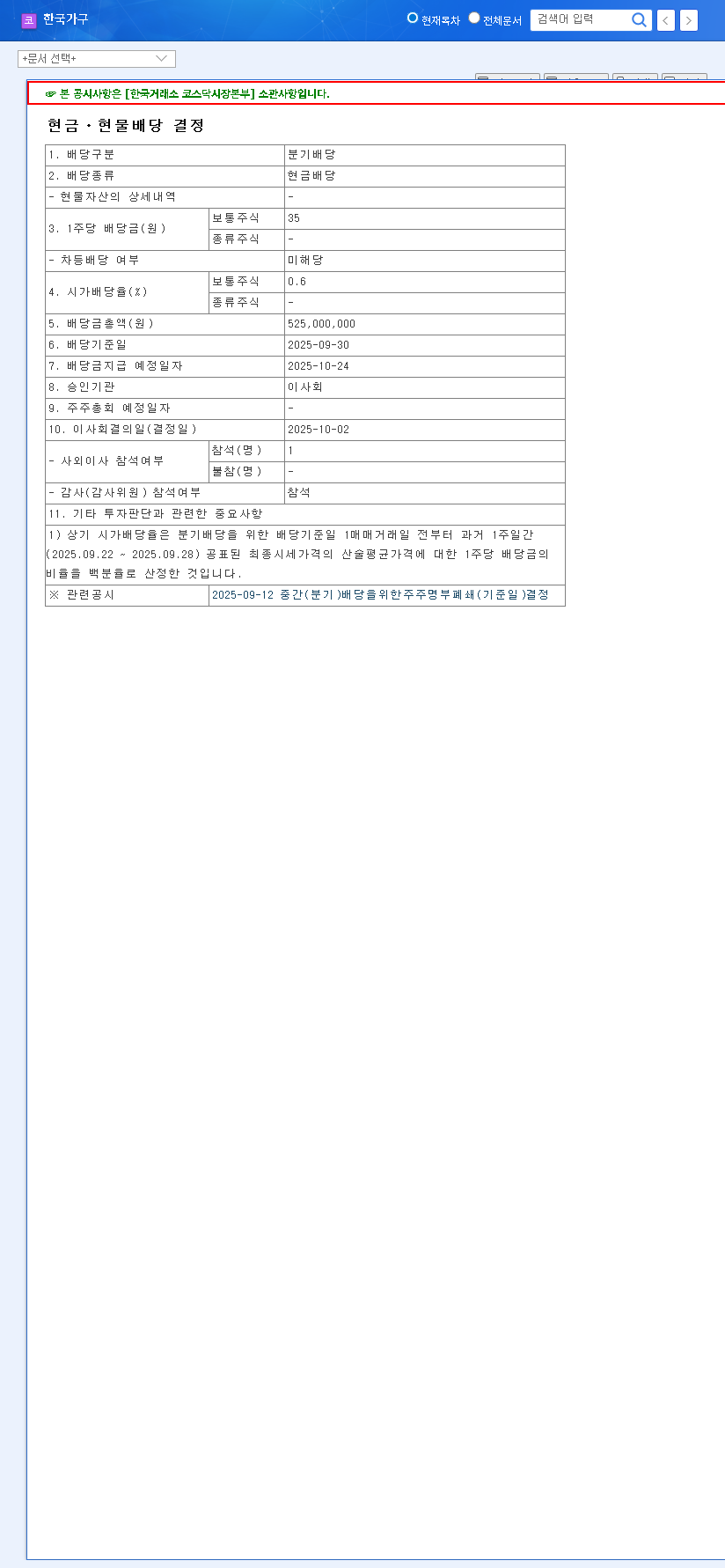

The Dividend Announcement: Key Details

The company formalized its commitment to shareholder returns with the latest quarterly cash dividend. The essential details from the Official Disclosure (DART) are as follows:

- •Dividend Amount: KRW 35 per common share.

- •Dividend Yield: Approximately 0.6% (based on the price of KRW 5,060 at the time).

- •Record Date: September 30, 2025.

- •Payment Date: October 24, 2025.

While consistent, this dividend doesn’t tell the whole story. To understand its real significance, we must look under the hood at the company’s two very different operating segments.

A Tale of Two Companies: Dissecting Hankook’s Performance

Hankook Furniture Co. Ltd. is a story of contrasts. One division is facing significant headwinds in a competitive market, while the other is thriving and driving the company’s overall growth. This internal dynamic is the single most important factor in any Hankook Furniture stock analysis.

1. The Lagging Furniture Division

The legacy Hankook Furniture segment, focused on furniture distribution and sales, is struggling. The latest report shows an 8.84% year-on-year revenue decrease and continued operating losses. This downturn is caused by a perfect storm of factors: a cyclical household furniture market, intense competition from both online and offline retailers, and a high dependency on overseas imports, which exposes the company to exchange rate volatility and rising logistics costs.

2. Jewon International: The Hidden Growth Engine

In stark contrast, the Jewon International division, which distributes confectionery ingredients, is booming. This segment saw revenue surge by an impressive 26.68% year-on-year, with operating profit skyrocketing by 65.24%. The strong demand for cocoa, chocolate products, and frozen bakery items is fueling this growth. The Jewon International performance is currently the primary driver of the company’s consolidated profits and the main reason it can sustain dividend payments.

Essentially, investors are not just buying a furniture company. They are investing in a holding company where a high-growth food ingredient business is subsidizing a struggling legacy operation.

Financial Health & Macroeconomic Risks

The dividend decision was made against a complex financial and macroeconomic backdrop. One notable red flag is the 14.35% increase in consolidated inventory assets. This suggests the furniture division is having trouble moving its products, which could lead to future write-downs and pressure on profitability.

Furthermore, the company is highly exposed to external forces. Fluctuations in the KRW/Euro exchange rate, volatile international raw material prices (like cocoa and oil), and rising global shipping costs are significant risks. As noted in reports from sources like Bloomberg, global supply chains remain a point of concern. While the company uses derivatives to hedge, recent losses on these transactions call the effectiveness of their strategy into question.

What the 0.6% Hankook Furniture Dividend Really Means

The Bull Case (Positive Signals)

- •Shareholder Commitment: The dividend demonstrates management’s dedication to returning value to shareholders, even amidst challenges.

- •Underlying Cash Flow: It proves that the highly profitable Jewon International segment generates enough cash to cover the dividend and support the wider company.

- •Price Support: For income-focused investors, a regular dividend can provide a floor for the stock price and attract stable, long-term capital.

The Bear Case (Potential Risks)

- •Low Yield: At 0.6%, the yield is not compelling enough on its own to attract serious dividend investors. The potential for capital appreciation is far more important.

- •Fundamental Weakness: The dividend could mask the severe underperformance of the furniture business. The core problem of a money-losing division remains unsolved.

- •Limited Impact: The market will likely focus on the company’s strategic direction and earnings reports rather than this small dividend payment.

Investor Action Plan & Key Checkpoints

Making an informed decision on Hankook Furniture requires looking beyond the dividend. For those considering an investment, focusing on long-term value investing principles is key. Monitor these critical points:

- •Furniture Turnaround Strategy: Watch for any concrete plans to improve profitability in the furniture division. This includes inventory management and competitive positioning.

- •Sustained Jewon Growth: Can Jewon International maintain its incredible growth trajectory? Look for signs of market share gains and effective risk management against commodity price swings.

- •Corporate Structure Changes: Is there any talk of spinning off Jewon International or selling the furniture division? Such a move could unlock significant value for shareholders.

Ultimately, the Hankook Furniture dividend is a minor plot point in a much larger story. The company’s future stock performance will be written by its ability to either fix its struggling furniture arm or fully unleash the power of its thriving food ingredient business.