The recent news surrounding E-Mart stock (139480) has created a complex picture for investors. On one hand, the National Pension Service (NPS) of Korea significantly reduced its stake, raising alarms. On the other, the company’s H1 2025 results reveal burgeoning growth in new sectors. This divergence leaves many asking: Is this a sign of impending trouble, or a buying opportunity in disguise? This comprehensive E-Mart stock analysis will dissect the fundamentals, decode the NPS’s move, and provide a clear investment strategy for Q3 2025 and beyond.

The NPS Bombshell: Understanding the Stake Reduction

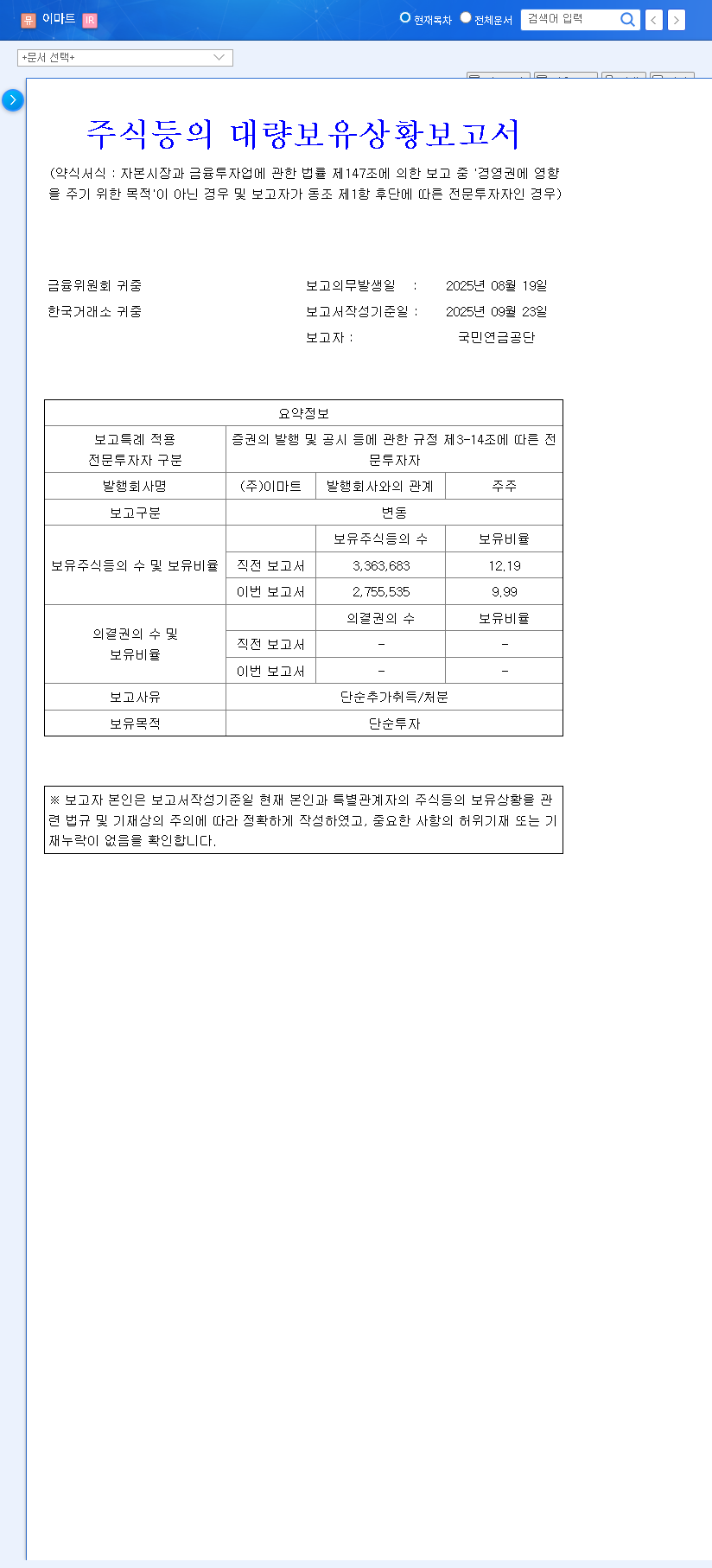

The most significant recent event impacting E-Mart stock was the disclosure that the National Pension Service, a colossal institutional investor, reduced its shareholding from 12.19% to 9.99%. A move of this magnitude by a major stakeholder naturally triggers market anxiety. However, the context is crucial.

The NPS classified this change as being for “simple investment” purposes. This typically means the decision is driven by portfolio management strategies—such as rebalancing, profit-taking, or managing risk exposure—rather than a negative verdict on E-Mart’s long-term corporate health. While this divestment could create short-term selling pressure and stock price volatility, its long-term impact is less certain. The official filing provides direct confirmation of this event, which you can review in the Official Disclosure (DART). Ultimately, the future of the 139480 stock will hinge on the company’s fundamental performance, not just the trading patterns of one institution.

A Tale of Two Companies: E-Mart’s Financial Health Check

E-Mart’s current financial situation is a study in contrasts. While its legacy business faces headwinds, new ventures are showing impressive vitality, leading to a consolidated operating profit surplus of KRW 180.9 billion year-over-year.

The Bright Spots: Growth Engines Firing Up

E-Mart’s strategy of diversification is bearing fruit, creating new pillars of growth that are offsetting weaknesses elsewhere. These are the key drivers:

- •Hotel & Leisure: This division’s sales surged by KRW 71.9 billion, capitalizing on the rebound in travel and leisure activities.

- •IT Services: With a sales increase of KRW 46.9 billion, this segment is proving to be a stable and profitable venture.

- •Overseas Business: The most significant contributor, with sales climbing by KRW 115.4 billion to KRW 1.18 trillion. Success in the U.S. market is demonstrating E-Mart’s potential for global expansion.

Furthermore, the company’s financial structure remains stable, with a debt-to-equity ratio of 154.74%, providing a cushion against macroeconomic shocks.

The Red Flags: Core Business Challenges Persist

Despite the success of its new ventures, E-Mart’s traditional core businesses are struggling. The primary concerns are:

- •Retail Sales Decline: The hyper-competitive South Korean retail market, coupled with a low-growth economic trend, led to a KRW 130.6 billion decrease in retail sales. The rise of agile e-commerce players continues to chip away at the dominance of traditional hypermarkets.

- •Construction Division Sluggishness: Increased market uncertainty and a more selective order strategy have caused both sales and operating profit to fall in the construction division, weighing on the group’s overall performance.

Macroeconomic Headwinds: The Bigger Picture for E-Mart Stock

No company operates in a vacuum. Broader economic forces are exerting significant pressure on E-Mart. As noted by global financial analysts at sources like Reuters, a persistent environment of high inflation and high interest rates erodes consumer purchasing power, directly impacting retail sales. Rising government bond yields in both the U.S. and Korea also signal potentially higher borrowing costs for the company in the future. These factors create a challenging backdrop for E-Mart’s core domestic business.

2025 E-Mart Investment Strategy: A “HOLD” Recommendation

After a comprehensive analysis of the competing factors, our recommended E-Mart investment strategy is a ‘HOLD’. This position acknowledges both the inherent risks and the tangible progress the company is making.

The ‘HOLD’ recommendation reflects a cautious optimism. While the core retail business requires a significant turnaround, the impressive performance of E-Mart’s diversified growth engines provides a compelling reason to wait and see how the company’s long-term strategy unfolds.

Key risk factors to monitor include intensifying retail competition, continued sluggishness in construction, and sustained macroeconomic pressure. Investors should also be prepared for short-term price swings following the NPS E-Mart stake reduction. To learn more about assessing such risks, you can explore our guide on evaluating retail sector stocks.

Frequently Asked Questions (FAQ)

Q1: Why did the NPS sell its E-Mart stock?

A1: The NPS reported the stake reduction was for “simple investment” purposes, suggesting it was part of a broader portfolio rebalancing strategy rather than a negative judgment on E-Mart’s future. While it can cause short-term price drops, the long-term direction of E-Mart stock will depend on business fundamentals.

Q2: Can E-Mart’s core retail business recover?

A2: The retail segment faces significant challenges from competition and a slow economy. However, E-Mart is actively working to strengthen its competitiveness through strategies like enhancing customer experience, developing popular private label products, and accelerating its digital transformation.

Q3: What are E-Mart’s most promising growth areas?

A3: E-Mart’s new growth drivers are its Hotel & Leisure, IT Services, and Overseas Business divisions. The overseas segment, especially, has shown massive growth, driven by its success in the U.S. market. This business diversification is critical to E-Mart’s long-term success.

Disclaimer: This article is for informational purposes only and is based on publicly available data. It does not constitute financial advice or a guarantee for investment decisions. All investment decisions should be made based on your own judgment and, if necessary, consultation with a financial professional.