Global cosmetic ODM leader COSMAX, INC. is at a pivotal moment, capturing investor attention with two major developments: robust H1 2025 performance and a strategic new patent acquisition. While top-line growth signals strong market demand, a closer look reveals financial complexities that warrant careful consideration. This analysis dives deep into what these events mean for the company’s competitive edge, its stock value, and its long-term trajectory in the dynamic beauty industry.

We will dissect the latest half-year report, unpack the significance of the ‘Antimicrobial Composition’ patent, and provide a balanced view of the opportunities and risks for investors considering COSMAX, INC. as part of their portfolio.

Unpacking the H1 2025 Financial Performance

COSMAX, INC.’s first-half results for 2025 paint a picture of impressive growth but also highlight underlying financial pressures. Understanding both sides is crucial for a complete assessment.

The Good: Strong Revenue and Operating Profit

The company showcased remarkable strength in its core business operations:

- •Revenue Growth: Consolidated revenue surged to KRW 1,212.1 billion, marking a 12.6% increase year-over-year. This indicates robust global demand for its cosmetic ODM services, particularly in key markets like China and the USA.

- •Operating Profit Increase: Operating profit climbed an impressive 21.7% to KRW 112.1 billion, signaling efficient management and strong operational leverage.

Areas for Concern: Net Income and Financial Health

Despite the positive top-line numbers, the bottom line tells a different story:

- •Net Income Decrease: Net income fell by 41% to KRW 32.4 billion. This was primarily attributed to non-operating financial costs, such as valuation losses on convertible bond put options.

- •High Debt Ratio: The debt-to-equity ratio remains elevated at 266.18%, a point of caution for risk-averse investors.

- •Negative Cash Flow: Negative operating cash flow suggests a potential increase in working capital burden and financial volatility, requiring close monitoring.

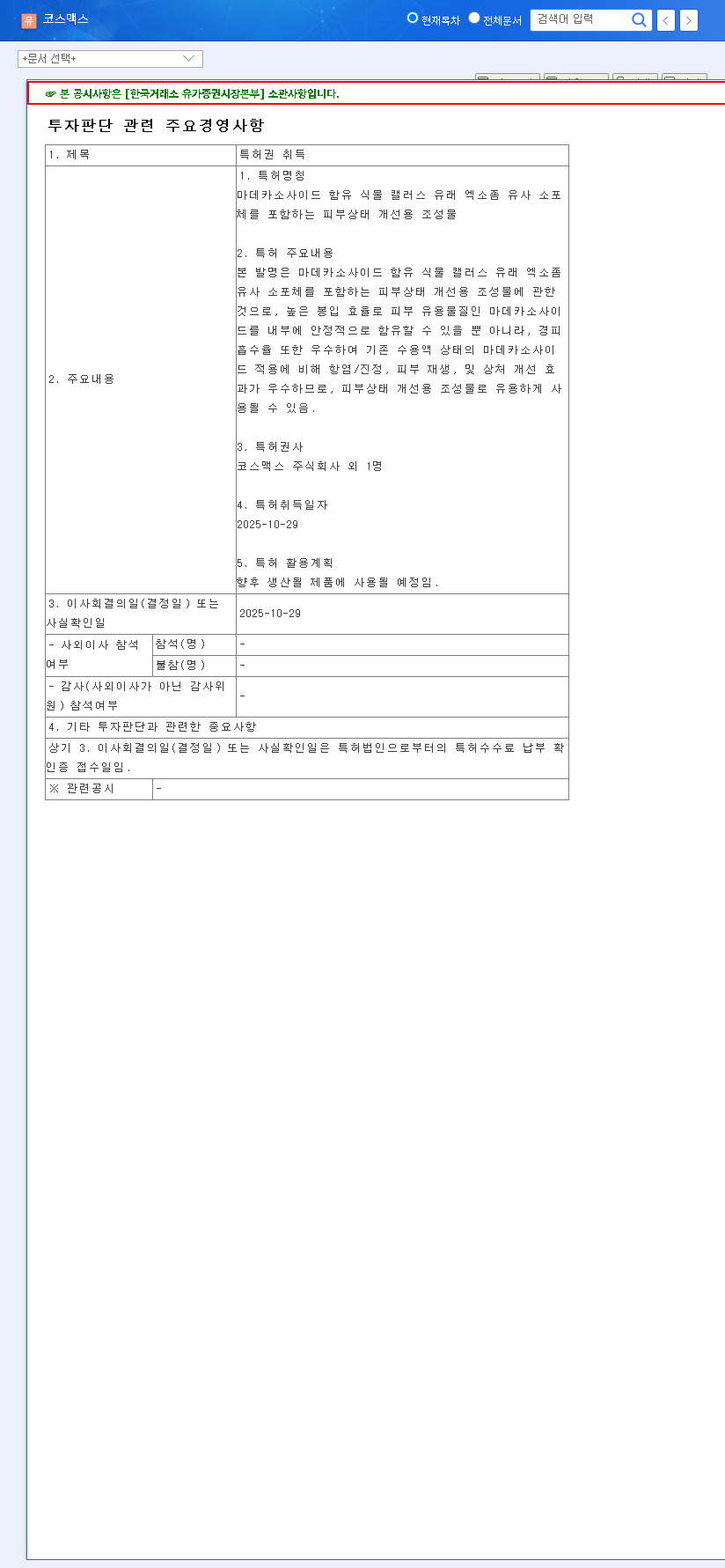

The Strategic Advantage: A Groundbreaking Patent Acquisition

Beyond the financials, COSMAX, INC. has fortified its technological moat with the acquisition of a key patent. This move is not just an R&D update; it’s a strategic play in the future of skincare.

The new patent for an ‘Antimicrobial composition’ is a game-changer, enabling COSMAX to develop products that selectively inhibit harmful bacteria while protecting the skin’s beneficial microbiome.

This technology, detailed in the Official Disclosure, directly taps into the growing consumer demand for clean and science-backed beauty. By focusing on microbiome health, COSMAX can differentiate its offerings, attract premium brands as clients, and command higher margins. This innovation underscores the company’s commitment to its R&D expenditure, which stands at a healthy 5.41% of sales.

Impact Analysis: Opportunities vs. Risks

Positive Catalysts for COSMAX Stock

- •Technological Leadership: The antimicrobial patent enhances product safety and efficacy, expanding the portfolio into high-performance lines and securing a long-term competitive advantage.

- •Revenue & Profit Growth: New products leveraging this patented technology are likely to see strong market adoption, driving both sales and profitability.

- •Sustainable Growth Engine: As a key intangible asset, this patent strengthens COSMAX’s foundation for sustainable growth in the ever-evolving global cosmetic ODM market.

Potential Risks and Headwinds

- •Financial Leverage: The high debt-to-equity ratio could lead to increased financial costs and volatility, especially in a rising interest rate environment.

- •Macroeconomic Factors: Profitability could be impacted by external pressures like exchange rate fluctuations, raw material costs, and global shipping challenges.

- •Commercialization Uncertainty: The success of the patent depends on market adoption, effective R&D execution, and the competitive landscape. There is always a risk of competitors developing similar technologies.

Investor Outlook & Action Plan

COSMAX, INC. presents a compelling, albeit complex, investment case. The company’s strong fundamentals and technological innovation create significant growth potential. However, the financial risks cannot be ignored. At present, a ‘Neutral’ investment opinion is warranted.

Investors should adopt a cautious approach and closely monitor these key areas:

- •New Product Pipeline: Watch for the launch of products using the new patent and gauge market response and their contribution to revenue.

- •Financial Deleveraging: Monitor the company’s progress in reducing its debt load and improving operating cash flow.

- •Market & Competitor Dynamics: Keep an eye on evolving consumer trends and the competitive actions within the cosmetic ODM/OEM space.

Disclaimer: This analysis is for informational purposes only and does not constitute investment advice. All investment decisions should be made based on your own research and judgment.