For investors evaluating opportunities in the Korean financial sector, a deep dive into Samsung Life Insurance (032830) is essential. As a titan of the industry, its performance is a bellwether for the market, but its complex structure and sensitivity to macroeconomic shifts demand careful analysis. This comprehensive report dissects the H1 2025 performance of Samsung Life Insurance stock, examines the pivotal disclosure regarding Samsung C&T’s shareholding change, and provides a forward-looking investment thesis. Our goal is to equip you with the critical insights needed to make informed decisions about this cornerstone of the KOSPI.

H1 2025 Financial Performance: A Mixed Picture

The first half of 2025 revealed a company navigating a complex environment with both commendable stability and clear challenges. The numbers tell a story of solid foundational health grappling with headwinds in profitability.

Robust Growth and Financial Soundness

On the positive side, Samsung Life Insurance demonstrated its resilience and market leadership through several key metrics:

- •Stable Profit Generation: Net profit saw a modest but stable increase of 1.30% year-on-year, reaching KRW 1.4711 trillion. This stability is crucial in an often-volatile financial market.

- •Top-Tier Financial Health: The company maintained an industry-leading K-ICS (Korean Insurance Capital Standard) ratio of 186.7%. This high ratio signifies robust capital adequacy, providing a significant buffer against market shocks and regulatory changes.

- •Commitment to Shareholder Value: A treasury stock holding of 10.21% signals a strong commitment to stabilizing the stock price and enhancing long-term shareholder returns.

Pressing Challenges for Profitability

Despite its solid foundation, the company faces significant hurdles in enhancing its profitability, primarily centered around its investment activities:

- •Low Asset Management Yield: The asset management yield stands at a modest 3.33%. In the current global economic climate, as detailed by sources like Bloomberg, improving this figure is a critical challenge. The company must urgently seek higher-yield assets while managing risk.

- •Decrease in Investment Income: A notable 11.84% year-on-year decrease in investment income highlights the vulnerability to market volatility. This underscores the need for more sophisticated risk management protocols within its vast securities portfolio.

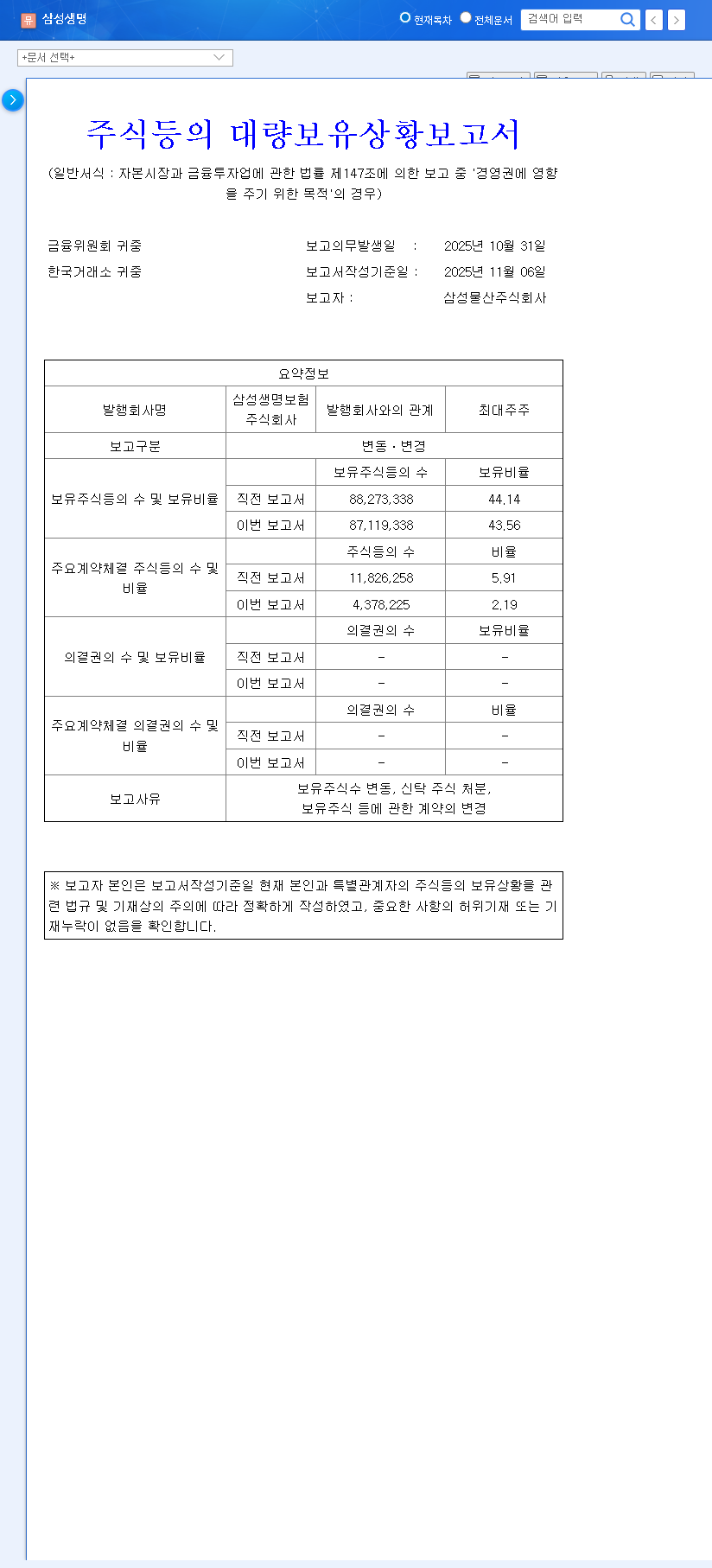

Analysis of the Samsung C&T Shareholding Change

One of the most significant recent events was the change in Samsung C&T’s shareholding in Samsung Life Insurance. This move, though seemingly small, has implications for corporate governance and investor perception.

According to the Official Disclosure, Samsung C&T reduced its stake by 0.58% (from 44.14% to 43.56%) following an off-market block trade by Ms. Lee Seo-hyun.

Interpreting the Impact

While the immediate risk to management stability is low—as Samsung C&T’s stake remains near a majority—this action warrants close attention. A large share disposal can create short-term downward pressure on the stock. However, given this was a minor reduction by an individual within the ownership family, the immediate market impact is likely contained. The key takeaway for investors is that it signals potential long-term shifts in the intricate ownership web of the Samsung Group. Any further changes must be monitored as they could affect governance and strategic direction.

Investment Thesis: Strengths vs. Headwinds

Core Strengths (The Bull Case)

The investment appeal of Samsung Life Insurance is built on a foundation of market dominance and forward-thinking strategy.

- •Dominant Market Position: As Korea’s #1 life insurer, its brand power and scale create a durable competitive moat.

- •Leading Digital Innovation: Aggressive investments in AI, big data, and digital platforms like Monimo are crucial for capturing the next generation of customers and improving operational efficiency.

- •Diversified Revenue: The strong performance of subsidiaries like Samsung Asset Management provides diversified revenue streams, reducing reliance on the traditional insurance business.

Key Headwinds (The Bear Case)

However, investors must weigh these strengths against significant challenges. The broader context of investing in the Korean financial market shows that even giants face structural issues.

- •Yield Improvement Urgency: The low asset management yield remains the primary obstacle to profit growth and must be addressed.

- •Demographic Shifts: An aging population and low birth rate in Korea are shrinking the traditional market for death insurance products, forcing a strategic pivot.

- •Ownership Uncertainty: While minor, the recent shareholding change introduces an element of uncertainty that requires continuous monitoring.

Conclusion: A Neutral Stance with Vigilant Monitoring

In conclusion, our Samsung Life Insurance analysis leads to a Neutral investment opinion. The company’s solid financials and market leadership provide a strong floor for the stock. However, the clear headwinds related to profitability and long-term market structure prevent a more bullish outlook at this time. Cautious optimism is warranted, but investors should closely monitor progress in asset yield improvement and any further changes in the major shareholder structure before committing significant new capital. The company is a stable giant, but one that must prove it can adapt to a rapidly changing world.