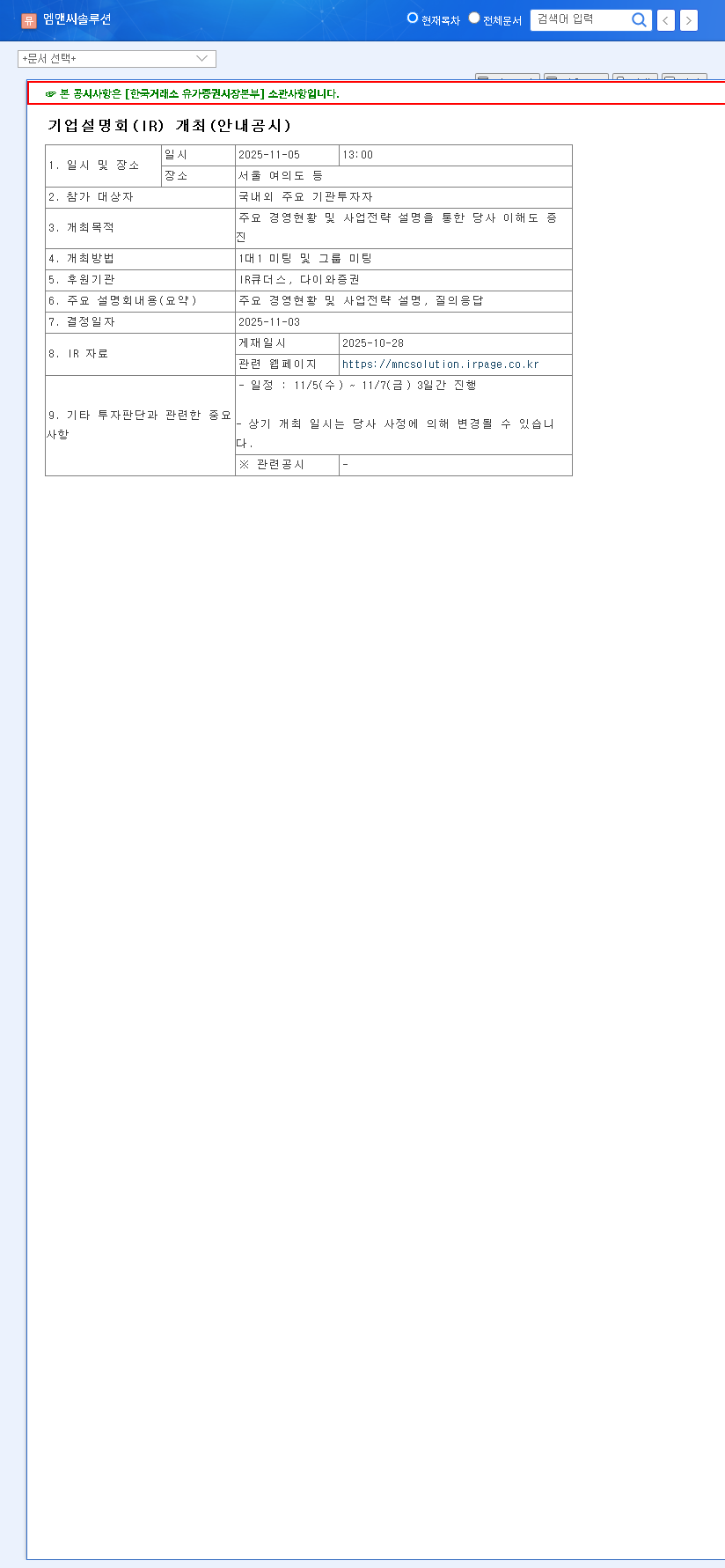

This comprehensive MECARO financial analysis delves into the company’s staggering Q3 2025 performance, where the leading semiconductor parts manufacturer announced results that have commanded the market’s attention. With an eye-watering 2,106% surge in operating profit, investors are keenly focused on the upcoming Investor Relations (IR) event scheduled for November 14th. We will unpack the core drivers of this explosive growth, examine the company’s robust financial health, and provide a detailed MECARO investment outlook to help you make informed decisions.

Unpacking the MECARO.CO.,LTD. Q3 2025 Earnings Report

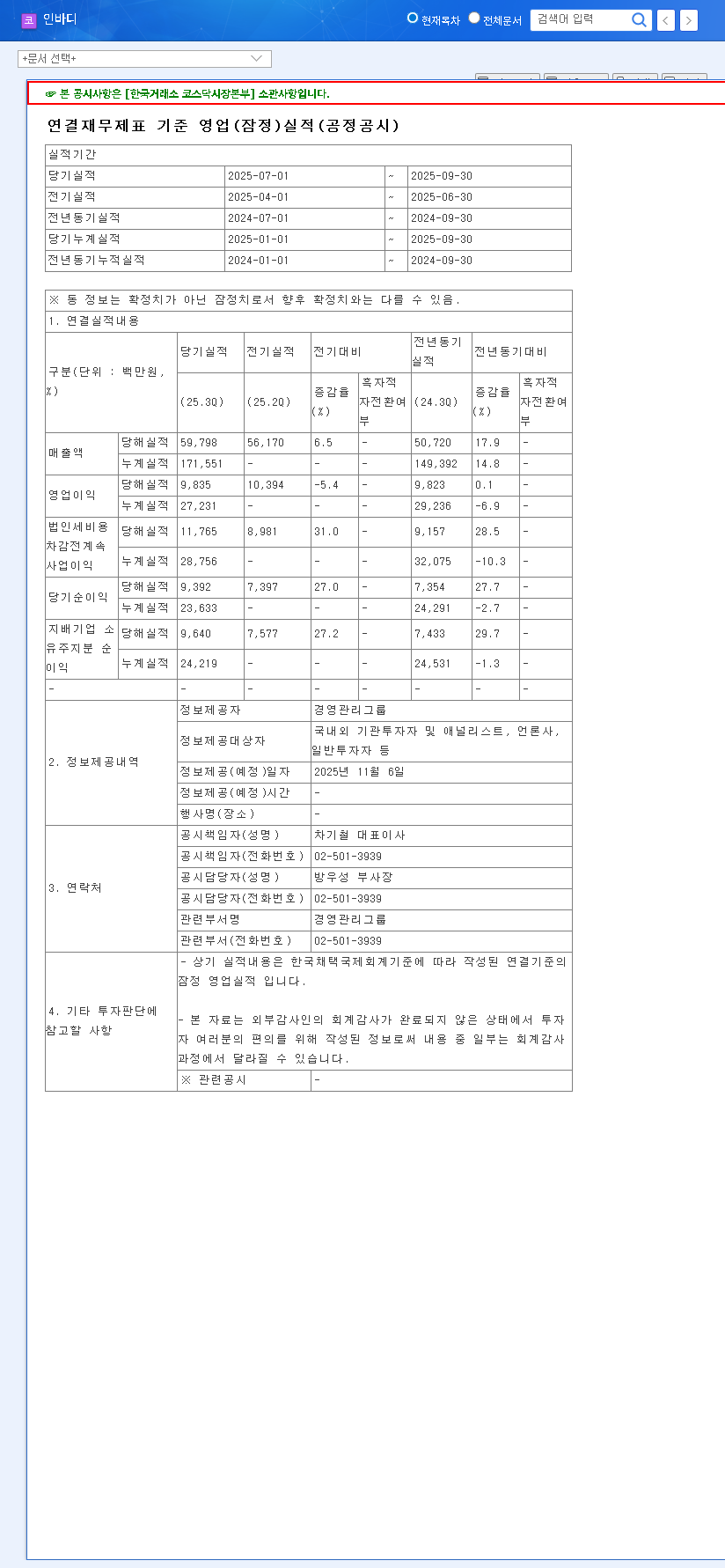

The financial data for the first nine months of 2025 paints a picture of exceptional success. MECARO.CO.,LTD. reported a consolidated revenue of KRW 70.161 billion, an impressive 68% increase year-over-year. The truly remarkable figure, however, is the operating profit, which rocketed by 2,106% to reach KRW 11.413 billion. Net profit also saw a significant 577% leap to KRW 11.794 billion, signaling a dramatic improvement in profitability and operational efficiency. These results provide a powerful backdrop for the company’s IR event, where management will address these figures and outline future strategies. For a complete breakdown, investors can review the Official Disclosure (DART report).

Deep Dive: The Engines Behind MECARO’s Explosive Growth

Such phenomenal growth isn’t accidental. It’s the result of a multi-faceted strategy and strong market positioning. A detailed MECARO financial analysis reveals several key contributors:

Dominance of Core ‘Heater Block’ Product

The cornerstone of MECARO’s success is its ‘Heater Block’ product line, which accounted for a massive 93.08% of total revenue. As a critical component in the semiconductor manufacturing process, the heater block ensures precise temperature control during wafer processing. MECARO’s market leadership and technological prowess in this niche have made it an indispensable partner for major global chipmakers. An export ratio of 44.74% for this product underscores its international competitiveness and high demand.

Strategic Global Expansion & Favorable Forex

Increased overseas sales were a significant catalyst. The company’s expansion into international markets, coupled with a favorable exchange rate environment (KRW/EUR at 1,696.57 and KRW/USD at 1,458.10 as of Nov 14, 2025), provided a dual boost to the top line. This global footprint not only diversifies revenue streams but also solidifies MECARO’s status as a key player in the global semiconductor supply chain. For more on industry trends, you can read about the global semiconductor market forecast.

MECARO’s performance is a textbook example of how product specialization, combined with effective cost management and global reach, can create exponential growth, even in a complex macroeconomic environment.

A Fortress Balance Sheet: MECARO’s Financial Stability

Beyond the headline-grabbing profit numbers, MECARO’s financial health is exceptionally strong, offering a significant layer of security for investors. A low debt profile and high liquidity demonstrate resilience and a capacity to weather economic shifts or fund future growth without taking on excessive risk. These are critical metrics for any long-term MECARO investment outlook.

- •Extremely Low Debt-to-Equity Ratio: At just 8.05%, the company has minimal reliance on debt financing, indicating a highly stable and self-sufficient financial structure.

- •Exceptional Liquidity: A consolidated current ratio of 710.40% and a quick ratio of 594.76% signify an outstanding ability to cover short-term liabilities with readily available assets.

Investor Action Plan: Opportunities & Risks for MECARO Stock

With the IR event on the horizon, investors should weigh the potential catalysts against the inherent risks. The strong MECARO.CO.,LTD. Q3 2025 earnings create a bullish foundation, but external factors must be considered.

Potential Positives (The Bull Case)

- •Strong Earnings Momentum: The outstanding results will attract significant investor interest, and a confident growth vision presented at the IR could fuel positive momentum for the MECARO stock.

- •Sustained Market Leadership: The dominance of its core products provides a reliable foundation for continued revenue and profit growth.

- •Macroeconomic Tailwinds: A trend of interest rate cuts in key markets like the U.S. and Europe could improve investor sentiment and lower future borrowing costs, as noted by sources like Reuters.

Potential Risks (The Bear Case)

- •Exchange Rate Volatility: The high proportion of overseas sales makes profitability sensitive to currency fluctuations. Investors should listen for the company’s hedging strategies at the IR.

- •High Expectations: The stellar results have set a high bar. If the IR presentation or future guidance fails to meet lofty market expectations, a short-term stock price correction is possible.

Conclusion: A Promising Outlook

Based on its robust fundamentals and stellar financial performance, MECARO.CO.,LTD. is poised to send a strongly positive signal to the market. Its leadership as a semiconductor parts manufacturer, combined with a pristine balance sheet, suggests that the current growth trajectory is sustainable. Short-term traders should watch the IR event closely for catalysts, while long-term investors should focus on the company’s ability to maintain its technological edge and expand into new markets. The MECARO stock remains a compelling story of growth and stability in a vital global industry.

Disclaimer: This article is for informational purposes only and does not constitute investment advice. Investors are solely responsible for their own investment decisions.