Investors examining SEOJIN SYSTEM (124075900928) are currently facing a complex picture. The company has recently been navigating significant headwinds, including a notable decline in its H1 2025 performance and concurrent shifts in its major shareholder structure. These events raise critical questions for any current or potential investor: Are these temporary setbacks in a volatile market, or do they signal a fundamental turning point for the company’s long-term value? This comprehensive SEOJIN SYSTEM analysis will dissect the company’s recent performance, explore the underlying causes, and provide a clear, forward-looking investment thesis to guide your decision-making process.

The Dual Challenge: Performance and Ownership

At the heart of the recent market concern are two primary developments that have created uncertainty around the SEOJIN SYSTEM stock. First, the company’s financial results for the first half of 2025 showed a significant downturn. Second, changes were reported in the holdings of its controlling shareholder, creating speculation about stability and future direction.

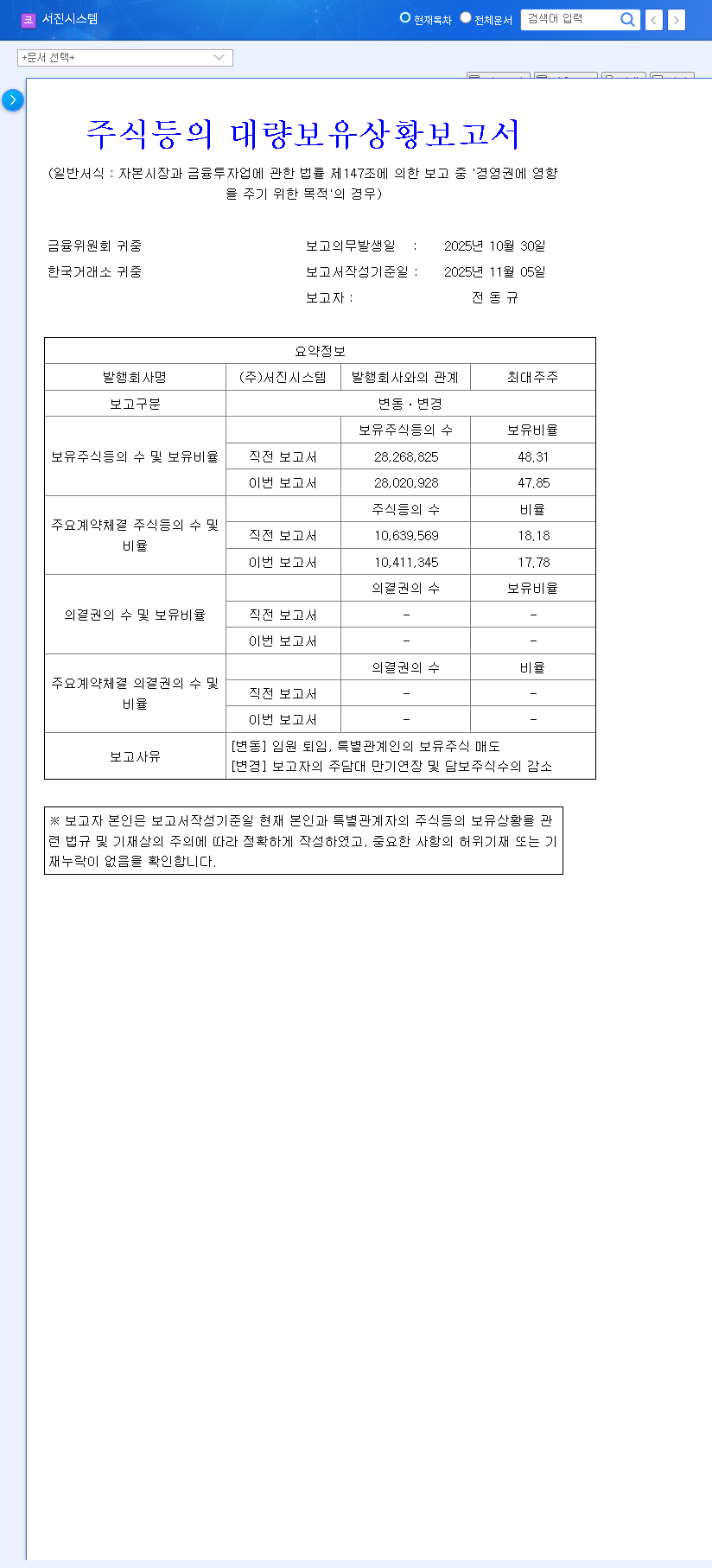

Major Shareholder Fluctuations

On November 6, 2025, a mandatory disclosure revealed shifts in the shares held by controlling shareholder Dong-kyu Jeon and related parties. According to the Official Disclosure (DART), the collective stake decreased by 0.46 percentage points, from 48.31% to 47.85%. This was attributed to an executive’s retirement, a sale of shares by an affiliate, and personal financial adjustments by the shareholder. While not a massive reduction, any change in a controlling stake can impact investor sentiment.

H1 2025 Performance Downturn

The financial report for the first half of 2025 painted a challenging picture. Consolidated revenue and operating profit saw substantial year-over-year reductions, and net income flipped to a deficit. This slump was not isolated to one area but was observed across all of the company’s key business segments, including Energy Storage Systems (ESS), electric vehicles (EV), semiconductors, and communications equipment.

Why the Downturn? A Deeper Look at the Fundamentals

Understanding the reasons behind the performance drop is crucial. The issues stem from both sector-specific challenges and a weakening overall financial structure, which is a key part of this SEOJIN SYSTEM investor report.

Underperformance Across Key Business Segments

- •ESS Equipment: Despite the global ESS market’s strong growth trajectory, H1 sales for SEOJIN SYSTEM decreased significantly, suggesting potential market share loss or project delays.

- •Electric Vehicle & Battery Components: Similarly, sales in the booming EV sector declined. Compounding this, substantial facility investments are increasing the company’s financial burden without yet delivering commensurate returns.

- •Semiconductor Equipment: While market analysts like Gartner project long-term growth, H1 sales fell, highlighting the company’s vulnerability to industry volatility and intense competition.

- •Communication Equipment: A sharp decline in sales, despite global investment in 5G, shows a high sensitivity to the capital expenditure cycles of major telecom operators.

Worsening Financial Health

The company’s balance sheet reflects this operational strain. The debt-to-equity ratio rose from 1.40x to 1.83x, a worrying trend that signals increasing leverage. A decrease in total equity alongside this rising debt raises concerns about overall financial soundness. For a deeper dive into these metrics, investors can review our guide on Understanding Financial Ratios for Tech Stocks.

Investment Outlook: Navigating the Uncertainty

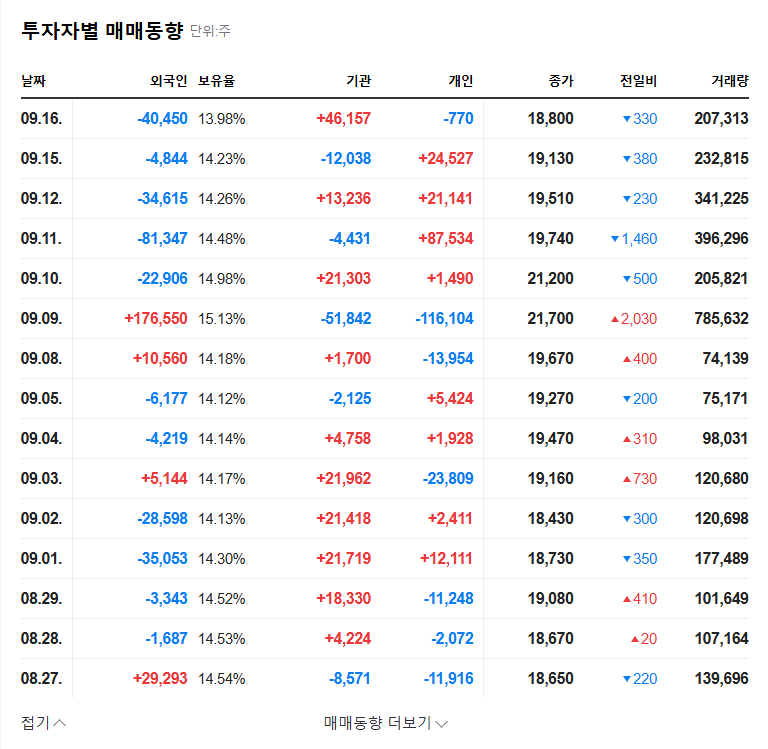

Given the dual headwinds of poor performance and ownership changes, the short-to-medium-term outlook for SEOJIN SYSTEM stock is clouded. The market is likely to react with caution, putting downward pressure on the stock price. The declining trend in foreign ownership, which fell from 10.44% in 2020 to 7.84% in August 2024, could accelerate if these negative trends persist.

Given the confluence of fundamental deterioration and market uncertainty, our current investment opinion for SEOJIN SYSTEM is a ‘Hold.’ It is essential for investors to monitor for clear recovery signals before considering new or additional positions.

Key Risk Factors to Monitor

- •Delayed Recovery: If the key business segments fail to rebound in the coming quarters, the stock could face further downward pressure.

- •Shareholder Overhang: The potential for additional share sales from affiliates could continue to weigh on market sentiment.

- •Financial Burden: The high debt ratio becomes a significant risk in a sustained high-interest-rate environment, potentially limiting future investment.

- •Macroeconomic Volatility: As an exporter, SEOJIN SYSTEM is highly exposed to exchange rate fluctuations (KRW/USD, KRW/EUR), which can directly impact profitability.

Potential Positive Catalysts

Despite the current challenges, it’s important to recognize the company’s underlying strengths. A comprehensive SEOJIN SYSTEM analysis isn’t complete without acknowledging its long-term potential.

- •High-Growth Portfolio: The company operates in industries—ESS, electric vehicles, and semiconductors—that are poised for significant long-term growth.

- •Operational Strengths: Its competitive Vietnam production base and proprietary technology provide a durable competitive advantage that can help it weather market downturns.

Investors should closely watch upcoming earnings releases for signs of a turnaround, monitor any further shareholder changes, and look for proactive efforts from management to improve the company’s financial structure.