In the dynamic world of biotechnology, investors are closely watching Psomagen Inc. (KRX: 202680), a key player in the genomic analysis market. A recent development involving its majority shareholder, Macrogen Inc., has sparked discussions about the company’s future trajectory and corporate value. This comprehensive Psomagen stock analysis aims to dissect this event, evaluate the company’s fundamental health, and provide a clear investment outlook for current and potential shareholders.

We will explore the implications of the Macrogen stake change, delve into Psomagen’s financial performance, competitive positioning, and future growth drivers to equip you with the insights needed for an informed Psomagen investment decision.

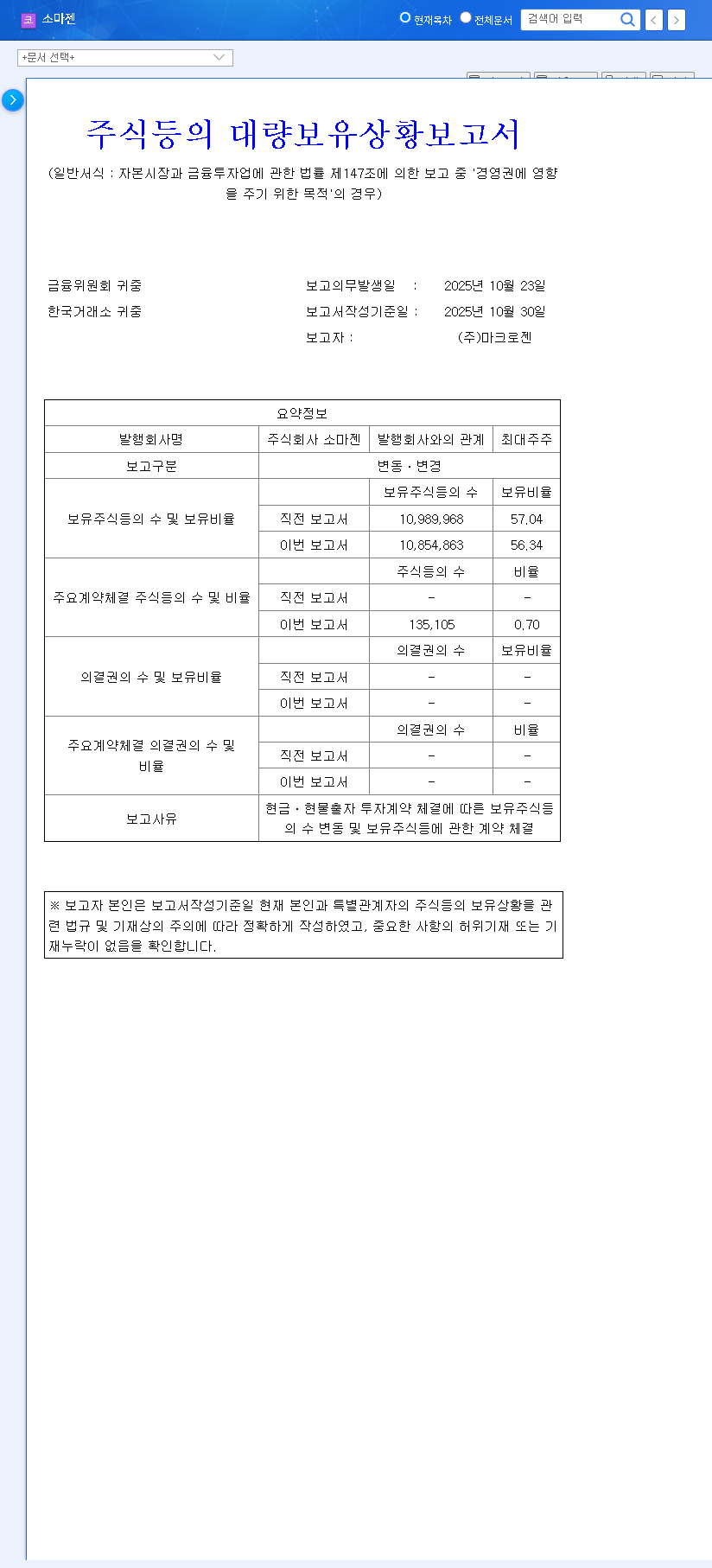

Unpacking the Macrogen Stake Change in Psomagen Inc.

On October 30, 2025, a mandatory disclosure revealed a shift in the ownership structure of Psomagen Inc. Macrogen Inc., the largest shareholder, announced a reduction in its equity stake. According to the Official Disclosure (Source), Macrogen sold 135,105 shares of Psomagen to GenomeforMe Co., Ltd. in an off-market transaction. This resulted in Macrogen’s ownership decreasing from 57.04% to 56.34%—a modest but notable 0.7 percentage point reduction. While this change doesn’t threaten management control, it introduces a new variable for investors: the role and intentions of GenomeforMe Co., Ltd.

The core question for investors is whether this minor stake reduction by Macrogen is a routine portfolio adjustment or a signal of a deeper strategic shift for Psomagen Inc.

A Deep Dive into Psomagen’s Corporate Fundamentals

To properly assess any Psomagen investment, we must look beyond a single headline and analyze the company’s intrinsic value and operational health.

Financial Performance (H1 2025)

Psomagen’s recent financial story is one of aggressive growth paired with profitability struggles. While revenue saw impressive expansion, high R&D and SG&A expenses continue to weigh on the bottom line.

- •Revenue Growth: Top-line revenue increased by a robust 41.8% year-over-year to $18.93 billion.

- •Profitability Challenge: The company recorded an operating loss of $1.39 billion, highlighting the urgent need for cost management.

- •Segment Performance: Next-Generation Sequencing (NGS) remains the primary revenue driver, accounting for ~70% of total sales. However, the DTC/Microbiome segment shows mixed results, with strong growth in Japan (up 38.0%) but a decline in the US (down 26.3%).

- •Cash Flow: A positive sign is the improving trend in operating cash flow, indicating better management of working capital.

Market Environment & Competitive Edge

Psomagen operates in a high-growth but fiercely competitive market. The global genomics market is expanding rapidly, a trend confirmed by industry reports from sources like leading market research firms. Competition from major players like Novogene and BGI is intense. Psomagen’s key competitive advantage, particularly in the lucrative US clinical market, is its attainment of CLIA/CAP certifications, which serve as a significant barrier to entry and a marker of quality and reliability.

Future Outlook & Growth Strategy

The company’s strategy focuses on diversifying its portfolio into high-potential areas like single-cell analysis, proteomics, and long-read sequencing technology. Expansion in the Japanese DTC market is a key growth lever. However, the path forward hinges on profitability. Achieving operational efficiency is not just a goal but a necessity. For a broader perspective on this sector, you might find it useful to read our guide on how to evaluate biotech stocks. The synergy with Macrogen is expected to continue, bolstering R&D and sales capabilities.

Stock Price Impact: Short-Term Jitters vs. Long-Term Value

A complete Psomagen stock analysis must consider market reaction. The 0.7% stake reduction is unlikely to cause major short-term panic among general investors. However, the lack of clarity surrounding GenomeforMe creates uncertainty. The mid-to-long-term impact will depend entirely on whether this new partnership becomes a strategic asset or a complication. The stock, recently trading around KRW 4,265, will ultimately be driven by fundamental performance and the company’s ability to turn its revenue growth into profit.

Final Verdict: A ‘Neutral’ Stance on Psomagen Investment

After a thorough review, our investment opinion on Psomagen Inc. (KRX: 202680) is ‘Neutral’. The company presents a classic growth-versus-profitability dilemma.

- •Positives: Strong revenue growth, expansion into future-proof sectors, a growing market, and continued support from its major shareholder.

- •Negatives: Persistent and significant losses, intense competition, and a lack of clear market catalysts to drive investor sentiment.

An upgrade to our rating would require tangible evidence of a turnaround in profitability and more clarity on the strategic implications of the GenomeforMe partnership. Investors should monitor quarterly earnings reports closely for signs of improved margins and operational efficiency.

Frequently Asked Questions (FAQ)

Q1: Is the Macrogen stake change a major concern for investors?

The 0.7 percentage point reduction is not large enough to impact management control. The primary concern is the uncertainty around the new shareholder, GenomeforMe. The long-term impact depends on the nature of this new relationship, which requires monitoring.

Q2: What is Psomagen’s current financial health?

Psomagen is experiencing strong revenue growth (up 41.8% in H1 2025) but is not yet profitable due to high operating costs. Its financial health is relatively sound with improving cash flow, and projections suggest a potential turnaround to profitability in late 2025.

Q3: What are Psomagen’s key future growth drivers?

Future growth is expected from diversification into new technologies like long-read sequencing and proteomics, as well as strategic expansion in high-growth markets like the Japanese direct-to-consumer (DTC) genetic testing space.

Q4: Is now a good time to invest in Psomagen stock?

We currently hold a ‘Neutral’ opinion. While the growth story is compelling, the persistent losses make it a speculative investment. It is advisable to wait for clear signs of profitability improvement before considering a significant position in Psomagen Inc.