Welcome to our comprehensive Samsung Electronics investment analysis for the first half of 2025. In an era defined by artificial intelligence and macroeconomic shifts, understanding the core fundamentals of a tech giant like Samsung is crucial. This detailed review of the Samsung H1 2025 report unpacks the performance of each business division, from semiconductors to mobile, providing investors with the critical insights needed to evaluate the company’s future trajectory and potential stock performance.

We will connect current achievements with historical patterns to offer a clear perspective on Samsung’s present state and highlight key considerations for your investment strategy. Let’s explore the present and future of Samsung Electronics together.

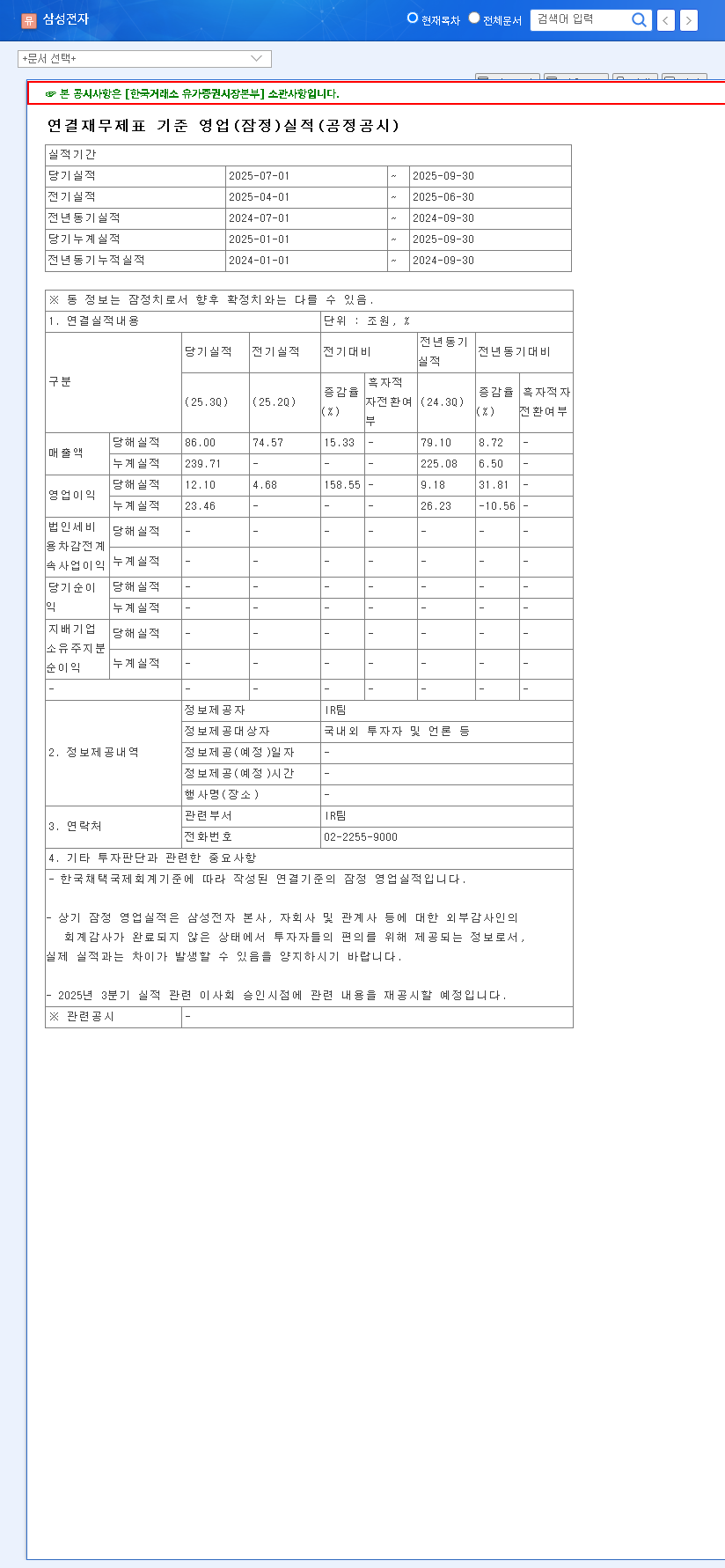

Samsung’s H1 2025 performance signals a strong recovery in its semiconductor division, fueled by AI demand, which is a pivotal factor for any forward-looking Samsung stock forecast.

Decoding the Samsung H1 2025 Report: A Divisional Deep Dive

Samsung Electronics showcased robust operations in H1 2025, navigating global uncertainties with strategic finesse. The pronounced growth in the Device Experience (DX) Division and a significant recovery in the Device Solutions (DS) Division are key highlights, signaling positive momentum.

Device Experience (DX) Division: AI-Powered Premium Strategy

The DX Division continues to fortify its market leadership through a dual focus on premium products and AI innovation. In the TV and home appliance sector, Samsung extended its remarkable 19-year streak as the top global TV seller. The expansion of ultra-large TV lineups and the integration of new AI technologies underscore its commitment to innovation. On the mobile front, the sustained growth of foldable phones and the rollout of ‘Galaxy AI’ demonstrate a clear Samsung AI strategy aimed at enhancing service competitiveness in a mature market. While these efforts are promising, a projected slowdown in 2025 TV market demand and geopolitical risks in the smartphone market present potential challenges.

Device Solutions (DS) Division: The Engine of Recovery

The DS Division is at the heart of Samsung’s resurgence, led by a rebound in the memory market. This recovery is driven by voracious AI market demand and renewed data center investments. Key points include:

- •Memory Leadership: Surging demand for HBM3E and high-capacity DDR5 products is boosting memory prices and improving profitability, a critical factor for any Samsung stock forecast.

- •System LSI & Foundry: Strategic expansion into the automotive semiconductor market and advancements in 2nm and 3nm GAA processes position Samsung for long-term growth. This is crucial for competing with industry leaders, as detailed in reports from sources like Reuters on the global chip war.

Macro Environment & Samsung’s Fundamentals

The global economic landscape significantly influences Samsung’s performance. The weaker Korean Won (USD/KRW 1,431.30) positively impacts export price competitiveness. Moreover, Samsung’s remarkably stable financial structure, a key aspect of its Samsung fundamentals, provides a strong defense against rising interest rates.

Analyzing Samsung’s Financial Health

As of H1 2025, Samsung’s financial health remains impeccable. With total assets of KRW 504.9 trillion against liabilities of KRW 105.3 trillion, the resulting debt-to-equity ratio is a low 49.38%. This financial stability is a cornerstone of the company’s resilience. Additionally, a substantial R&D investment of KRW 18.1 trillion (11.8% of sales) underscores a commitment to future growth, aligning with its past patterns of heavy investment in innovation. For verifiable figures, investors can review the Official Disclosure (DART report).

Actionable Investor Takeaways & Considerations

This Samsung Electronics investment analysis reveals a company at a pivotal moment. The recovery in semiconductors, driven by AI, is a powerful tailwind. However, investors must remain vigilant.

- •Monitor Macro Trends: Keep a close eye on global inflation, interest rates, and geopolitical tensions, which can impact consumer demand and supply chains.

- •Track the AI Arms Race: Samsung’s success hinges on its ability to compete in the high-stakes AI and semiconductor markets. For more on this, see our deep dive into the global semiconductor market.

- •Value Shareholder Policies: Samsung’s consistent dividend payouts and share buybacks are positive indicators of its commitment to shareholder value.

Disclaimer: This analysis is based on the provided information, and investment decisions should be made at the investor’s own discretion and responsibility.

Frequently Asked Questions

Q1: Which division had the best performance in Samsung’s H1 2025 report?

The DS (Semiconductor) Division showed the most positive performance, driven by the memory market’s recovery due to strong AI demand and data center investments, which significantly improved profitability.

Q2: What is the state of Samsung Electronics’ financial health?

Samsung maintains an exceptionally stable financial structure. As of H1 2025, its debt-to-equity ratio is a low 49.38%, a consistent strength that provides resilience.

Q3: What are Samsung’s key areas for future growth?

Samsung is heavily focused on its Samsung AI strategy (e.g., Galaxy AI), expanding into the automotive semiconductor market, and capturing the growing IT and automotive OLED display markets.